October lived up to its reputation as being a torrid month. The following extraordinary performances tell the story:

- MSCI Word Index: -19.1% (largest monthly decline since the Index started in 1969, beating October 1987's -17.1%)

- MSCI Emerging Markets Index: -27.1% (worst monthly loss since Russia's debt default in August 1998)

- Dow Jones Industrial Index: -14.1% (15th worst monthly decline since 1900 and the biggest drop since October 1987)

- S&P 500 Index: -16.9% (8th worst one-month decline since 1930)

- US Dollar Index: +7.8% (4th best one-month improvement since 1967)

- Reuters/Jeffries CRB Index: -22.3% (worst monthly decline since the Index started in 1956)

- Crude-oil futures: -32.6% (worst one-month drop since oil futures started trading on the New York Mercantile Exchange in 1983)

- Reuters/Jeffries CRB Industrials Index: -26.5% (sharpest monthly decline since the series started in 1971)

- Gold futures: -18.5% (biggest monthly loss since 1983)

But the last week of the month witnessed a strong rebound in global stock markets as investors brushed aside discouraging economic reports and took heart from central banks cutting key lending rates and positive developments in the credit markets. This resulted in investors scooping up beaten-down stocks around the globe, and particularly emerging-market stocks, government bonds and currencies, mending some of the damage done earlier in October.

Further evidence of just how tough October has been was provided by Thursday and Friday's stock market improvement producing the first back-to-back days of gains for the S&P 500 Index and the Dow Jones Industrial Index since September 25 and 26.

In the spirit of Halloween, one can rightfully ask: trick or treat? (By the way, the masks below, according to FT Alphaville, are not accompanied by suitcases of money.)

The FOMC lowered the Fed funds target rate from 1.5% to 1.0% on Wednesday. This action followed an emergency 50 basis point cut in the benchmark rate on October 8. The committee's statement said economic activity has "slowed markedly" and cited weakness in consumer spending, business investment and exports. It also noted tight credit. The statement furthermore said that "downside risks to growth remain", an indication that more rate cuts could follow. The target rate was last at 1.0% in 2004 and has not been below this level since 1958.

The Fed followed up its rate-cutting action with an announcement that it was setting up dollar swap lines with Brazil, Mexico, South Korea and Singapore, contributing to the sharp turnaround in emerging-market assets.

Next, a tag cloud of the text of the large number of articles I have devoured during the past week. This is a way of visualizing word frequencies at a glance. Unsurprisingly, the key words included the following: "market", "bank", financial", "fund" and "credit".

Where do we go from here? One bit of cheer is that the stock market is now entering what has historically been the strongest half of the year. "... investing in the S&P 500 Index from the last trading day in October (therefore referred to as the Halloween indicator) through the end of April accounted for the vast majority of S&P 500's gains since 1950. While there are some noteworthy periods in which the Halloween indicator didn't produce (i.e. 1973-74 and 2000-01), the overall outperformance is compelling," reported Chart of the Day.

To which Jeffrey Hirsch (Stock Trader's Almanac) added: "... November is much better in election years when the incumbent party is ousted - usually because of dissatisfaction with the status quo. Traders and investors often celebrate a change of the guard when the economy and stock market are on the ropes as they are now."

Here is Richard Russell's (Dow Theory Letters) take on matters: "Things are looking better. After a series of 90% down-days, we had a 90% up-day on Tuesday, October 28. Since then, the market action has been fairly good. With bonds appearing to have topped out, I'm beginning to think that there's a fairly good chance the market has bottomed. On Thursday's statistics, Lowry's Selling Pressure Index (supply) finally dropped substantially, giving evidence of an important drop in supply. At the same time their Buying Power Index surged, finally showing an increased willingness to buy. So far, so good."

I summarized my viewpoint in a post on Friday: "I give the current rally the benefit of the doubt provided the recent lows (8,176 on the Dow Jones Industrial Index and 849 on the S&P 500 Index) do not get taken out. However, it remains difficult to say whether a secular low has been reached in an environment of economic and profit recession. At least, the extent to which central banks, governments and the IMF are becoming involved to fend off a total economic meltdown is a sign that we could be in a bottoming-out phase of the bear market."

The last word goes to Laszlo Birinyi (Birinyi Associates) who cautioned as follows: "We believe the markets are in uncharted territory with developments and characteristics that are unique in our experience and we can only guess at what might transpire over the next several months. Frankly we don't know, history provides no clues and anyone who claims to have some insight or strategy cannot do so on the basis of fact and historical evidence."

Before highlighting some thought-provoking news items and quotes from market commentators, let's briefly review the financial markets' movements on the basis of economic statistics and a performance round-up.

Economic reports

"Sentiment is extraordinarily negative in North America and Europe and measurably weaker in Asia and South America," according to the Survey of Business Confidence of the World conducted by Moody's Economy.com. The financial panic that began in early September has been a body blow to global business confidence and thus the global economy which, according to the survey, is now in recession.

Economic reports released in the US during the past week were mostly negative. The most important of these was the announcement that real GDP fell by 0.3% in the third quarter. Weakness was driven by consumer spending, down 3.1% (i.e. subtracting 2.2 percentage points from the GDP calculation), as higher gas prices, housing weakness and job losses created huge headwinds for the consumer. Business equipment spending declined while strength was added by exports and government spending.

Summarizing the US economic situation, Asha Bangalore (Northern Trust) said: "The National Bureau of Economic Research (NBER) will eventually announce the onset of a recession. Based on the NBER's methodology, the recession appears to have commenced in the fourth quarter of 2007/first quarter of 2008.

"The question now is about the depth and duration of the recession. In the post-war period, the median duration of a recession has been 10 months and median drop in real GDP from the peak to trough is a 1.9% annualized decline.

"How will the current recession compare with prior history? In our estimation, the depth and duration will err on the side of being slightly higher than the historical median given the nature of the credit crisis that is under way. Congress is supposedly working on a second stimulus package that could moderate the weakness in economic activity."

Elsewhere in the world, the Bank of Japan cut interest rates on Friday for the first time in seven years, reducing the target overnight call rate by 20 basis points to 0.30%. Earlier last week, South Korea, Hong Kong, China, Taiwan and Norway also cut benchmark rates (in the case of China, the third cut in six weeks). It is expected that the European Central Bank, the Bank of England and the Reserve Bank of Australia will ease monetary policy during the coming week.

Week's economic reports

Click here for the week's economy in pictures, courtesy of Jake of EconomPic Data.

| Date | Time (ET) | Statistic | For | Actual | Briefing Forecast | Market Expects | Prior |

| Oct 27 | 10:00 AM | New Home Sales | Sep | - | 445K | 450K | 460K |

| Oct 28 | 10:00 AM | Consumer Confidence | Oct | 38.0 | 52.0 | 52.0 | 59.8 |

| Oct 29 | 8:30 AM | Durable Orders | Sep | - | -1.0% | -1.0% | -4.5% |

| Oct 29 | 10:35 AM | Crude Inventories | 10/25 | - | NA | NA | NA |

| Oct 29 | 2:15 PM | FOMC Policy Statement | - | - | - | - | - |

| Oct 30 | 8:30 AM | Chain Deflator-Adv. | Q3 | 4.2% | 4.2% | 4.0% | 1.1% |

| Oct 30 | 8:30 AM | GDP-Adv. | Q3 | -0.3% | +0.3% | -0.5% | 2.8% |

| Oct 30 | 8:30 AM | Initial Claims | 10/25 | 479K | 470K | 473K | 479K |

| Oct 31 | 8:30 AM | Employment Cost Index | Q3 | 0.7% | 0.7% | 0.7% | 0.7% |

| Oct 31 | 8:30 AM | Personal Income | Sep | 0.2% | 0.1% | 0.1% | 0.5% |

| Oct 31 | 8:30 AM | Personal Spending | Sep | -0.3% | -0.3% | -0.2% | 0.0% |

| Oct 31 | 9:45 AM | Chicago PMI | Oct | 37.8 | 50.0 | 48.0 | 56.7 |

| Oct 31 | 10:00 AM | Mich Sentiment-Rev. | Oct | 57.6 | 52.0 | 57.5 | 57.5 |

In addition to interest rate announcements by the Bank of England and the European Central Bank on Thursday, November 6, next week's US economic highlights, courtesy of Northern Trust, include the following:

1. ISM Manufacturing Survey (November 3): The consensus for the manufacturing ISM composite index is 41.5 versus 43.5 in September.

2. Employment Situation (November 7): Payroll employment in October is predicted to have dropped by 200,000 following a decline of 159,000 in the prior month. The jobless rate is predicted to have risen to 6.2% from 6.1% in September. Consensus: Payrolls: -200,000 versus -159,000 in September, unemployment rate: 6.3% versus 6.1% in September.

3. Other reports: Construction spending, auto sales (November 3), factory orders (November 4), ISM Non-manufacturing (November 5).

Click here for a summary of Wachovia's weekly economic and financial commentary.

A summary of the release dates of economic reports in the UK, Eurozone, Japan and China is provided here. It is important to keep an eye on growth trends in these economies for clues on, among others, the direction of the US dollar.

Markets

The performance chart obtained from the Wall Street Journal Online shows how different global markets performed during the past week.

Source: Wall Street Journal Online, October 31, 2008.

Equities

Stock markets throughout the world closed the week with excellent gains, spurred on by a combination of interest rate cuts, an improvement in short-term lending rates, short covering and bottom-picking buying. The MSCI World Index improved by 9.8%, but still leaving the Index 39.8% down for the year to date. Leading the pack among developed markets were Germany (+16.1%), the UK (+12.7%) and Japan (+12.1%).

A dramatic reversal of fortune hit emerging markets on the back of the Fed's dollar swap lines for a number of key developing economies, resulting in the MSCI Emerging Markets Index surging by 20.4% (YTD -54.2%). The week's largest increases were recorded by Russia (+40.8%), Mexico (+19.3%), Brazil (+17.4%), South Korea (+18.6%) and Turkey (+15.1%).

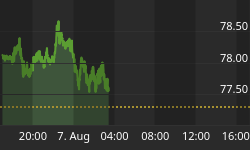

The performance of the Dow Jones World Index (green line) and the MSCI Emerging Markets Index (red line) during October is shown by the graph below.

The table below by Finviz summarizes the past week's performances (in US dollar terms, whereas all the gains/losses referred to elsewhere in this post are in local currency terms) for various stock markets.

The US stock markets all improved strongly over the week as shown by the major index movements: Dow Jones Industrial Index +11.3% (YTD -29.7%), S&P 500 Index +10.5% (YTD -34.0%), Nasdaq Composite Index +10.9% (YTD -35.1%) and Russell 2000 Index +14.1% (YTD 29.8%).

The Dow needs to rise to 9,810 - 5.2% higher than its current level of 9,325 - in order to be "officially" classified as being in a bull market again. The Index will be required to increase by 10.2% to reach its 50-day moving average and 25.4% to get to the key 200-day line.

A (delightfully green) market map, obtained from Finviz.com, providing a quick overview of the performance of the various segments of the S&P 500 Index over the week.

The bar chart below, also from Finviz, shows the US sector performance for last week, and specifically how defensive sectors such as utilities and healthcare underperformed on a relative basis.

Putting the stock market outlook in perspective, Eoin Treacy (Fullermoney) said: "... the current environment is extraordinary in terms of how overextended markets have become relative to their long-term averages. Statistically, a reversion to the mean (i.e. 200-day moving average) remains the most likely scenario in the short to medium term. Where markets consolidate subsequent to that move will be an important marker for the shape of any potential recovery."

Fixed-interest instruments

Yields on short-dated government bonds were mostly lower during the past week, whereas yields on long-term paper moved up. Long bonds appear to be topping out, either because investors are switching from bonds to stocks, or because the bond market is starting to discount better economic times in the months ahead.

US mortgage rates increased, with the 30-year fixed rate jumping by 44 basis points to 6.56% (in line with the 30-year US Treasury Note rising by 29 basis points) and the 5-year ARM by 9 basis points to 5.99%.

The cost of buying credit insurance for US and European companies eased as shown by the narrower spreads for both the CDX (North American, investment grade) Index (down from 227 to 200) and the Markit iTraxx Europe Crossover Index (down from 920 to 765).

Money-market rates declined as a result of rate cuts by a number of central banks and the ongoing provision of liquidity. The three-month dollar Libor rate declined by 49 basis points to 3.03% during the week, but remained 203 basis points above the Fed's target rate of 1.0%. The spread was 43 basis points at the start of the year.

Currencies

A statement by the G7 warning about the dangers of the excessive gains in the Japanese yen caused investors to fear currency intervention. This concern, together with a rate cut of 20 basis points to 0.30% by the Bank of Japan, helped to cool the yen against all major currencies.

Also on center stage was a strong turnaround in a number of emerging-market currencies as investors were comforted by (1) the Fed establishing dollar swap lines with Brazil, South Korea, Singapore and Mexico, and (2) aid programs from the IMF and other organizations reducing the risk of defaults.

Over the week the US dollar gained against the Japanese yen (+4.2%), but lost ground against the euro (-0.9%), the British pound (-0.9%), the Swiss franc (-0.9%), the Canadian dollar (-5.5%), the Australian dollar (-7.4%), the New Zealand dollar (-4.8%) and a host of emerging-market currencies.

Has the greenback made its high for the current cycle? Paul Kedrosky (Infectious Greed) argued in a recent guest post on my blog site that the US dollar's surge won't last. "Down is up, and up is down? How is it that a growing US economy was bad for the US dollar, but a potentially calamitous collapse in the same US economy has the US dollar up double-digit percentages?," asked Kedrosky.

BCA Research outlined its currency strategy as follows: "First, the euro and pound will be 'trading buys' against the dollar and yen, but no more than that. The European economies and financial systems will be soggy for some time, and their central banks are still behind the curve. Second, the trade-weighted dollar is close to a three-year high, which will not make economic sense even after the US economy and banking system turn the corner. Most likely, the dollar will lose ground against emerging and commodity currencies with good fundamentals, but will hold its own against the euro. Finally, the yen is a tougher call and we recommend standing aside."

Commodities

Fears that the deteriorating global economic situation was causing demand destruction resulted in strong selling pressure for all commodities during October, resulting in the Reuters/Jeffries CRB Index plunging by 22.3% for the month - its sharpest monthly decline since the Index started in 1956.

However, commodities reversed course during the past week as dollar weakness resulted in an improvement for most commodities (with the exception of gold), as shown by the following chart:

Now for a few news items and some words and charts from the investment wise that will hopefully assist in keeping our investment portfolios on a profitable course. Let's hope that after the volatile trading that characterized most of October, conditions will calm down - as always happens after a storm. And if this is part of the change to be brought about by a new US president after Tuesday's election, nobody will be complaining.

That's the way it looks from Cape Town.

The American consumer - R.I.P.

"The great American consumer - much like the Norwegian Blue parrot of Monty Python fame - is dead. A stiff. Bereft of life. He rests in peace."

Source: New York Post, October 26, 2008.

BBC News: Steve Forbes - Credit crisis: "The worst is over"

"Steve Forbes, the publisher of Forbes magazine, is one of the few people remaining optimistic despite gloomy predictions about the global economy. He talked to Matt Frei about how an economic recovery could be underway."

Source: BBC News, October 29, 2008.

CNBC: Recovery Could Take 20 Years - Hugh Hendry

"The ongoing financial turmoil and economic gloom will take 10 or 20 years to heal, Hugh Hendry, partner at hedge fund Eclectica, told CNBC."

Source: CNBC, October 22, 2008.

Sovereign Society: Felix Zulauf - world is entering a "soft depression"

"Zulauf believes we're entering a soft economic depression. If not for the government's backstops on October 13 to prevent further stock and credit market seizures, a depression would have followed. Zulauf is convinced the markets would have crashed.

"His prediction of a severe recession will take the S&P 500 Index down all the way to 550, possibly 500. Stocks have already plunged 40% from their October 2007 highs. Zulauf is adamant: 'US stocks are still not cheap. The S&P 500 Index trades at 1.7 times book-value and the Dow more than 3.5 times book. This is still expensive.'

"The Swiss advisor now predicts a very different world will emerge as a result of widespread government nationalization of banking. These efforts - started in the West - will send the wrong message to emerging markets, also likely to follow the same course of full or partial nationalization.

"This will also mark the end (at least temporarily) of the globalization theme, as markets will gradually be closed to foreign competition amid a marked increase in government regulation of financial markets. He also expects foreign currency controls as economic distress accelerates.

"According to Zulauf, a 'soft depression' lies ahead. And Europe might be the focal point because the banking system there is worse than in the United States.

"'There's a disaster unfolding in Eastern and Central Europe. These countries are now unwinding leverage, namely Hungary, Romania and Bulgaria. They've borrowed heavily in foreign currencies and now have to pay those funds back as bank liquidity dries.'

"Zulauf also believes Italy, Greece and Spain will eventually exit the single European currency, or the euro.

"He seriously doubts the euro - in its current form - will survive beyond 10 years as government deficit ceilings are breached amid a bulging credit crisis. The 15 members comprising the Eurozone must keep budget deficits at 3% of GDP or lower in accordance with the Maastricht Treaty.

"Despite his bearish tone, Zulauf believes global equities will offer one of the best buying opportunities in a generation sometime over the next 24 months. This includes real estate. He's expecting stocks to stage a powerful bear market rally off the October lows.

"But beyond a big move, he thinks the economic landscape is still deteriorating and earnings forecasts are too aggressive. Still, after the next big drop, he does believe stocks will be trading at incredibly low levels."

Source: Sovereign Society, October 27, 2008.

BBC News: Financial crisis - world round-up

"A look at the regions of the world most affected by the financial crisis, and what governments are doing to try to alleviate the financial turmoil."

Click here for the full article.

Source: BBC News, October 29, 2008.

Financial Times: IMF to speed lending to select countries

"The International Monetary Fund on Wednesday unveiled a new emergency lending programme that will get money to well-run countries quickly and with almost no conditions attached if they are hit by financial volatility.

"The new liquidity facility is the culmination of a decade of attempts at the IMF, after the Asian financial crisis of 1997-98, to come up with a way of protecting big emerging markets from financial contagion.

"The IMF's executive board on Wednesday agreed to allow countries with sustainable debt and a good policy track record to borrow up to five times their 'quota', or financial contribution to the IMF, with almost no conditions.

"'This fills a gap in the fund's toolkit of financial support,' said Dominique Strauss-Kahn, the IMF's managing director. 'It shows the fund can act quickly and decisively.'

"An IMF official said that a 'discrete and not particularly large group" of nations would likely qualify. With the exception of Argentina, which Mr Strauss-Kahn ruled out as a participant, the fund declined to name them. But fund officials said it should be fairly easy for market participants to identify eligible countries from the IMF's annual assessments of debt sustainability and fiscal and monetary policy.

"Independent economists said that the four emerging markets to which the US Federal Reserve offered currency swap lines on Wednesday - Brazil, South Korea, Mexico and Singapore - would certainly qualify, though they would probably choose Fed money first over IMF money. Other countries likely to meet the fund's criteria included the Czech Republic, Chile and possibly Poland, while economies with large current account deficits such as South Africa and Turkey would probably not, they said.

"Lending will be for three months at the fund's standard interest rates, renewable up to twice within a twelve-month period. IMF officials said that money could be available within 72 hours."

Source: Alan Beattie, Financial Times, October 29, 2008.

Financial Times: IMF firepower could soon run short

"With its $2 billion rescue loan to Iceland and $16.5 billion to Ukraine, the International Monetary Fund has started to dip into an arsenal that is full to the brim. Yet the IMF could soon run short of firepower.

"In spite of the period of relative peace in recent years among emerging markets, the private armies of global finance have grown much faster than the fund's store of ammunition.

"The IMF, headed by Dominique Strauss-Kahn, has about $200 billion in easily reachable money and another $50 billion or so it can access rapidly. But Simon Johnson, a former IMF chief economist now at the Massachusetts Institute of Technology, says that is relatively small. 'Maybe if the IMF had two trillion dollars it could be a serious global player,' he says. 'But $200 billion can go very quickly. There are a lot of countries in the same position as Ukraine, and you only need to add one or two of the really big countries to use it up.' Mr Johnson reckons that with other countries also in trouble, the IMF has probably already had to pencil in committing about a quarter of its $200 billion over the next few months."

Source: Alan Beattie, Financial Times, October 27, 2008.

Bloomberg: Ryan says treasury to need "unprecedented" financing

"The US Treasury faces historic financing demands from a weakening economy and the added costs of a $700 billion Wall Street rescue program, the department's top domestic finance official said today.

"'This year's financing needs will be unprecedented,' said Anthony Ryan, the Treasury's acting undersecretary for domestic finance, at a Securities Industry and Financial Markets Association conference in New York.

"Ryan's borrowing outlook comes after Treasury officials spent much of the past month publicly praising the rescue plan's virtues. The Treasury needs to sell debt to raise money for the new initiatives and also cope with a weaker economy, two factors analysts say may push the country's budget deficit to more than $1 trillion for the current fiscal year.

"As part of the rescue effort, the Treasury aims to boost the economy by pushing $250 billion in new capital to US banks. Half of that money has been set aside for large banks, which hold about half of all US deposits, in hopes of stimulating more lending to businesses and consumers. The rest will go to regional banks and smaller institutions.

"Analysts say the 2009 budget deficit could be more than double the White House projections. In fiscal year 2008, which ended September 30, the deficit was a record $455 billion."

Source: Rebecca Christie and Robert Schmidt, Bloomberg, October 28, 2008.

Bloomberg: Fed spurs record surge in longer-term commercial paper issuance

"Sales of longer-term commercial paper soared 10-fold after the Federal Reserve began buying the corporate IOUs, a sign that the central bank's efforts toward unlocking the market may be working.

"Companies yesterday sold 1,511 issues totaling a record $67.1 billion of the debt due in more than 80 days, compared with a daily average of 340 issues valued at $6.7 billion last week, according to Fed data. The central bank probably absorbed about $60 billion of the total, said Adolfo Laurenti, a senior economist at Mesirow Financial.

"'That's the very first really good news in quite some time,' said Laurenti. 'It's probably something the government can do and the normal investor would not otherwise do.'

"The Fed began buying commercial paper from companies yesterday to reduce rates, lure back investors and unlock the market, which seized up last month following the bankruptcy of Lehman Brothers."

Source: Bryan Keogh, Bloomberg, October 28, 2008.

The Wall Street Journal: US mulls widening bailout to insurers

"The Treasury Department is considering buying equity stakes in insurance companies, a sign of how the government's $700 billion rescue program could turn into a piggy bank for a range of beleaguered industries.

"The availability of US government cash in the middle of a global credit squeeze is drawing requests from insurance firms, auto makers, state governments and transit agencies. While Treasury intended for the program to apply broadly, the growing requests could put a strain on the $700 billion, a sum that only last month stunned lawmakers.

"Insurers are critical to market stability. Signs of eroding confidence at life insurers could further dent fragile business and consumer confidence. Insurers are among the biggest holders of the nation's corporate debt, with $1.3 trillion on their books."

Source: Deborah Solomon and Leslie Scism, The Wall Street Journal, October 25, 2008.

Associated Press: Treasury set to dish out financial rescue funds

"The US government will start doling out $125 billion to nine major banks this week to get credit flowing again, but Monday's announcement offered cold comfort to investors as rising anxiety about a worldwide recession drove stocks down sharply around the globe.

"Assistant Treasury Secretary David Nason said the deals with the nine banks were signed Sunday, and the government will make the stock purchases this week. The deals are designed to bolster the banks' balance sheets so they will begin more normal lending.

"The action will mark the first deployment of resources from the government's $700 billion financial rescue package passed by Congress on October 3.

"The bailout package has undergone a major change in emphasis since it was passed by Congress. Treasury Secretary Henry Paulson decided to use $250 billion of the $700 billion to make direct purchases of bank stock, partially nationalizing the country's banking system, as a way to get money into the financial system more quickly.

"The plan is also aimed at clearing banks' balance sheets of bad assets. That effort has yet to begin although the administration expects to use $100 billion to purchase bad assets in coming months.

"Treasury is also starting to give approval to major regional banks with the goal of getting another $125 billion in stock purchases made by the end of this year."

Source: Martin Crutsinger, Associated Press (via Breitbart), October 27, 2008.

CNNMoney.com: Bernanke discusses future of Fannie and Freddie

"Federal Reserve Chairman Ben Bernanke said Friday that the federal government will need to continue to play a role in the future of the mortgage financing market.

"In a speech broadcast to an economic symposium in Berkeley, Calif., Bernanke said there are many alternatives that need to be considered but that all will involve a role for the federal government and federal guarantees for securities backed by mortgage loans.

"'Government likely has a role to play in supporting mortgage securitization, at least during periods of high financial stress,' he said.

"The two government sponsored firms either owned or guaranteed about $5 trillion in mortgages between them and their problems could end up costing taxpayers hundreds of billions of dollars in future losses.

"But Bernanke said having them replaced by totally private firms could cause greater problems for the economy during a future financial crisis. Thus, he said that the federal government will likely have a role guaranteeing mortgages into the future.

"'From a public policy perspective, a greater concern with fully privatized [firms] is whether mortgage securitization would continue under highly stressed financial conditions,' he said. 'As I have noted, almost no mortgage securitization is occurring today in the absence of a government guarantee.'

"Bernanke did not endorse any specific alternative for Fannie and Freddie and he stopped short of advocating for the government to completely nationalize the two firms. Instead, he gave a rundown of numerous proposals that have already been raised by Fed and Treasury officials as well as other experts."

Source: Chris Isidore, CNNMoney.com, October 31, 2008.

Financial Times: Hungary gets $25.1 billion rescue package

"The International Monetary Fund, the European Union and World Bank on Tuesday agreed to a $25.1 billion economic rescue package for Hungary to bolster confidence in its economy hit by the global financial crisis.

"The IMF said it had reached an agreement with Hungary for a $15.7billion loan programme, while the European Union stood ready with an additional $8.1 billion in financing and the World Bank another $1.3 billion. The IMF loan will be disbursed over 17 months.

"It is the biggest international rescue package for an emerging market economy since the start of the current global crisis and is the first for an EU-member country. Last week the IMF approved a $2.1 billion deal for Iceland and a $16.5 billion programme for Ukraine.

"'The Hungarian authorities have developed a comprehensive policy package that will bolster the economy's near-term stability and improve its long-term growth potential,' Dominique Strauss-Kahn, IMF managing director, said.

"'At the same time it is designed to restore investor confidence and alleviate the stress experienced in recent weeks in the Hungarian financial markets,' he added."

Source: Financial Times, October 28, 2008.

Financial Times: Gulf Bank bailout

"Who would have thought it? Gulf states, or rather their petrodollar-flush sovereign wealth funds, had won a reputation for providing first aid to the ailing global financial system, taking stakes in once-revered names only to watch their value plummet. It was as if they could pour good money after bad almost indefinitely, even as the oil price fell towards $60 a barrel.

"The same aura of resilience extended to the Gulf's banks - until Kuwait's weekend rescue. Gulf Bank is the region's first casualty - not because of subprime losses or overexposure to the heady Dubai property market, but after derivative counterparties defaulted, costing it an estimated $800 million. Seven days is a long time in a global financial crisis: a week after the Central Bank of Kuwait said deposit guarantees were not needed, Gulf Bank's loss - which looks to be a one-off - forced it to guarantee all local bank deposits."

Source: Financial Times, October 27, 2008.

Bloomberg: Shipping news suggests world economy is toast

"In the third quarter of 2007, Volvo AB booked 41,970 European orders for new trucks. Guess how many prospective purchases Volvo, the world's second-biggest maker of heavy rigs, received in the third quarter of this year?

"Here's a clue. Picture a highway gridlocked by 41,815 abandoned trucks - because Volvo's order book got destroyed to the tune of 99.63%, with customers signing up for just 155 vehicles in the three-month period, the Gothenburg, Sweden-based company said last week.

"The pathogen that has fatally infected swathes of the banking industry is now contaminating non-financial companies. 'We're heading toward the sharpest downturn I've ever seen in Europe,' said Chief Executive Officer Leif Johansson.

"Volvo has company. Daimler AG, the world's biggest truckmaker, said earlier this month that its US deliveries slumped by a third in the first half of the year."

Source: Mark Gilbert, Bloomberg, October 30, 2008.

Bill Moyers Journal: Interview with James Galbraith

"Bill Moyers sits down to talk about the economic future with James K. Galbraith, Chair in Government/Business Relations at the LBJ School of Public Affairs of the University of Texas."

Source: Bill Moyers Journal, October 24, 2008.

Bespoke: Overnight Libor at lowest level in years

"As a sign that the credit crisis has eased significantly for the time being, overnight Libor has dropped to its lowest levels in years to 0.73125%. After spiking to 6.43% at a time when the Fed funds rate was at 2% on September 16, and then spiking to 5.09% again on October 9, O/N Libor is now below the 1% Fed Funds Rate. Let's hope it stays that way!"

Source: Bespoke, October 30, 2008.

Asha Bangalore (Northern Trust): Fed takes aggressive action

"The Fed took aggressive action once again and lowered the Fed funds rate 50 bps to 1.00%, putting the total amount of easing at 425 bps since September 18, 2007. It was a unanimous vote. The discount rate was also cut by 50 bps to 1.25%.

"On October 8, the FOMC statement indicated that economic activity has weakened, while particular sectors were not mentioned. By comparison, the October 29 statement describes slowing conditions but also notes explicitly that the major culprit is consumer expenditure."

Source: Asha Bangalore, Northern Trust - Daily Global Commentary, October 29, 2008.

BCA Research: Fed moving closer to monetization

"The Fed funds rate may well hit zero in the next six months given the profound weakening in the economic outlook. Eventually, the Fed might be forced to print money.

"As expected, the Fed eased policy again yesterday, returning the funds rate to 1%, the level reached in the wake of the burst technology bubble. The economy is in much worse shape today than it was back then, warning that policy may have to be eased even further.

"While the Fed's program to purchase commercial paper appears to be off to a good start, the key issue is whether there is a more broad-based thaw in the credit freeze. The signs are still not encouraging on this front with many key credit spreads at or close to their peaks.

"The Fed's balance sheet has exploded upwards, but the corresponding rise in bank reserves needs to spread out into the broader economy. In this respect, it will be important to monitor the ratio of M2 to the monetary base (the money multiplier). This has plunged recently, but that may simply be due to lags. If it fails to revive, the Fed will continue to expand its asset support programs but ultimately may have to resort to quantitative easing."

Source: BCA Research, October 30, 2008.

The Wall Street Journal: Ex Fed governor makes case for zero Fed funds rate

"With the US unemployment rate now expected to climb well above 7%, former Federal Reserve governor Laurence Meyer projects that Fed policymakers may have to lower the target federal-funds rate all the way to zero next year.

"The FOMC is widely expected to reduce the rate to 1% from 1.5% at the conclusion of its two-day meeting Wednesday. Meyer and former Fed economist Brian Sack, who are both with Macroeconomic Advisers, said they expect another half-percentage-point rate cut in December, to 0.5%. Their baseline assumption is that the easing cycle will stop there.

"'However, the expected rise in the unemployment rate, paired with the rising threat of deflation, presents a risk that the FOMC will have to ease even further, perhaps all the way to a zero federal funds rate,' Meyer and Sack wrote in a research note.

"Meyer and Sack said they think the jobless rate will rise to as high as 7.5% from 6.1% now. They also expect a significant gross domestic product contraction of 2.8%, at an annual rate, in the fourth quarter, after a projected 0.7% decline in the third. They also expect GDP to fall in the first quarter of next year."

"'Plugging our interim forecast into our backward-looking policy rule suggests that the federal funds rate should be cut to zero by the middle of next year,' Meyer and Sack wrote.

"'Our forward-looking policy rule ... gives similar results if we plug in our updated forecast, as it calls for a funds rate of about zero by early 2010,' they wrote."

Source: The Wall Street Journal, October 28, 2008.

Asha Bangalore (Northern Trust): Q3 GDP - details tell a grimmer story than headline

"Real gross domestic product fell 0.3% in the third quarter, after a boost from tax-rebate dollars lifted growth in the second quarter to an annual rate of 2.8%. The decline in real GDP as seen from the headline is sobering but less troublesome than the details.

"Government spending contributed 1.15% to the headline GDP, with the defense component accounting for the lion share (+0.9%) of the increase. Going forward, state and local government spending is likely to be weaker than the already tepid growth seen in the past few quarters.

"The contribution of net exports to growth of real GDP in the third quarter (1.13%) was close to that of government spending. However, economic growth in foreign economies has slowed and projections show weaker world economic growth (even excluding the US) in the quarters ahead compared with forecasts prior to the intensification of the financial turmoil.

"Among the other major components of GDP, consumer spending fell at annual rate of 3.1% in the third quarter, the first quarterly decline since the fourth quarter of 1991 when consumer spending dropped at an annual rate of 0.3%. The magnitude of the decline in consumer spending is the largest since the second quarter of 1980, when some households literally were cutting up their credit cards."

Source: Asha Bangalore, Northern Trust - Daily Global Commentary, October 30, 2008.

John Williams (Shadow Government Statistics): US economy is in a severe recession

"The reported 'advance' growth estimate usually is massaged so as to come in close to consensus, in this case a little bit better ...

"With real retail sales, housing, nonfarm payrolls, new orders for durable goods and industrial production all showing quarterly and annual growth patterns never seen outside of a recession still in deterioration, GDP reporting eventually should show a string of quarterly contractions, with the recession dating back to fourth-quarter 2006, long before the exacerbation of the current systemic solvency crisis. ... official GDP surrogates such as Gross National Product (GNP) and Gross Domestic Income (GDI) have shown varying patterns of quarterly contractions. GDP is the theoretical equivalent of GDI (consumption side versus income side) and is GNP net of the trade balance in interest and dividend payments.

"Based on existing GDP, GDI and GDP reporting, the following quarters have shown inflation adjusted quarterly contractions: 1Q07 (GNP), 4Q07 (GDP), 1Q08 (GDP/GDI), 3Q08 (GDP)."

Source: John Williams, Shadow Government Statistics (via The King Report), October 30, 2008.

Asha Bangalore: Consumer spending on watch list, no surprises here

"Consumer spending dropped 0.3% in September, following two months of steady readings. However, after adjusting for inflation, consumer spending has dropped in three out of the last four months. In September, inflation adjusted consumer spending declined 0.4% after a nearly flat reading in August (+0.02%).

"On a quarterly basis, the decline in the third quarter (-3.1%) is the first drop since the fourth quarter of 1991. In September, real consumer spending fell 0.4% on a year-to-year basis, which is the largest drop since January 1991. Why is this sharp decline important? Consumer spending is the largest component of GDP (a little over 70%) and it has been the engine of growth. At the cost of stating the obvious, a setback in consumer spending translates into overall weak economic conditions. Keeping up with the Halloween tradition, it is scary indeed!"

Source: Asha Bangalore, Northern Trust - Daily Global Commentary, October 31, 2008.

Asha Bangalore (Northern Trust): Falling prices lift sales of new homes

"Sales of new single-family homes rose 2.7% to an annual rate of 464,000 in September. Purchases of new single-family homes are down 66.6% from the peak in July 2005. The August sales mark of 452,000 units appears to be the bottom for the current business cycle.

"The inventory of unsold new single-family homes dropped to a 10.4-month supply from an 11.4-month mark in August. The downward trend is a positive factor. But the elevated level continues to suggest that additional declines in home prices are nearly certain."

Source: Asha Bangalore, Northern Trust - Daily Global Commentary, October 27, 2008.

Standard & Poor's: Case-Shiller - national trend of home price declines continues into the second half of 2008

"Data through August 2008, released today by Standard & Poor's for its S&P/Case-Shiller Home Price Indices, shows continued broad based declines in the prices of existing single family homes across the United States, a trend that prevailed throughout the first half of 2008 and has continued into the second half.

"The chart above depicts the annual returns of the 10-City Composite and the 20-City Composite Home Price Indices. Once again, the indices have set new records, with annual declines of 17.7% and 16.6%, respectively. However, the acceleration in decline was only moderate in August. The July data reported annual declines of 17.5% and 16.3%, respectively."

Source: Standard & Poor's, October 29, 2008.

The New York Times: Consumers feel the next crisis: it's credit cards

"First came the mortgage crisis. Now comes the credit card crisis. After years of flooding Americans with credit card offers and sky-high credit lines, lenders are sharply curtailing both, just as an eroding economy squeezes consumers.

"The pullback is affecting even creditworthy consumers and threatens an already beleaguered banking industry with another wave of heavy losses after an era in which it reaped near record gains from the business of easy credit that it helped create.

"Lenders wrote off an estimated $21 billion in bad credit card loans in the first half of 2008 as more borrowers defaulted on their payments. With companies laying off tens of thousands of workers, the industry stands to lose at least another $55 billion over the next year and a half, analysts say. Currently, the total losses amount to 5.5% of credit card debt outstanding, and could surpass the 7.9% level reached after the technology bubble burst in 2001."

Source: Eric Dash, The New York Times, October 28, 2008.

James Quinn (Telegraph): US faces deflation to compound its misery

"One of Wall Street's leading economists has warned that North America faces a period of significant deflation next year on tops of its already sizeable economic challenges.

"David Rosenberg, Merrill Lynch's chief US economist, believes that deflation will occur, adding to the recessionary environment North America already finds itself in and potentially delaying the nation's economic recovery.

"Mr Rosenberg was the first Wall Street economist to declare that the US had entered a recession back in January of this year, and had also long warned of systemic problems in the global credit markets.

"'We believe the next major macro-economic theme is deflation,' Mr Rosenberg writes in a research report. 'Within a year, we see a very good chance that [inflation] will be running below 0% on a year-over-year basis.'

"He argues that just as the economy was showing signs of a recession nearly a year before economic growth turned negative, today's current economic backdrop is deflationary.

"The respected economist goes on to explain that deflation can become self-perpetuating, as consumers begin to defer spending on hopes of further discounts as prices fall - so reinforcing the downward pressure on demand.

"'Likewise, firms that are faced with deflation to their top lines are typically forced to cut costs to protect their profit margins and in so doing, trigger a second-round negative income effect on their workers and suppliers, which also ends up exacerbating the trend towards lower pricing.'"

Source: James Quinn, Telegraph, October 27, 2008.

Bloomberg: Mishkin sees "significant" odds inflation may go too low

"Former Federal Reserve Governor Frederic Mishkin talks with Bloomberg's Kathleen Hays about the US government's response to credit turmoil, the housing and mortgage markets and Fed monetary policy."

Source: Bloomberg, October 28, 2008.