Changing the digits on the calendar from '08 to '09 may not have transformed the dire outlook for the global economy, but during the holiday-shortened New Year week investors appeared adamant to put the rout of 2008 behind them.

Although mercifully the door has been closed on 2008, let's recap some of the unprecedented movements experienced in financial markets during the year.

Equities:

• MSCI World Index: -42.1% (worst yearly performance since start of Index in 1970)

• S&P 500 Index: -38.5% (worst annual percentage decline since 1937 and 3rd worst on record; largest quarterly [4th quarter: -298] and daily [September 29: -107] points decline ever; 6th worst daily percentage decline [October 15: -9.0%])

• Dow Jones Industrial Index: -33.8% (worst annual percentage decline since 1931 and 3rd worst on record; largest quarterly [4th quarter: -2,330] and daily [September 29: -778] points decline ever; 6th worst daily percentage decline [October 15: -7.9%])

• S&P 500 and Dow Jones: There was no point in 2008 where the indices were up for the year at the close of a trading day. Since 1900, 2008 was only the 4th year (after 1910, 1962 and 1977) where the Dow never had a single day where it closed up for the year, according to Bespoke.

• FTSE Eurofirst 300 Index: -44.8% (worst yearly percentage fall since its creation in 1986)

• Nikkei 225 Average: -42.1% (biggest annual percentage decline on record)

• CBOE Volatility Index (VIX): Historical high in November based on new calculation, but remained below levels seen during the 1987 crash based on an previous calculation.

Treasuries:

• US Treasuries: Yields dropped to lowest levels since 1950.

• US 10-year Treasury Notes: Yields fell by 182 basis points - biggest yearly points decline since 1995 and the second biggest in the last 20 years.

Currencies:

• Japanese Trade-weighted Index: +25.0% (largest annual rise since currency was allowed to float freely in 1973)

• Pound against US dollar: -26.2% (worst annual decline since gold standard was abandoned in 1971)

• Pound against euro: -22.8% (worst yearly decline since launch of single currency in 1999)

Commodities:

• Reuters/Jeffries CRB Index: -36.0% (worst annual performance since inception of Index in 1956)

The table below highlights the performance of the principal asset classes for 2008. While West Texas Intermediate Crude (-53.5%), the S&P 500 Index (-38.5%) and the Reuters/Jeffries CRB Index (-36.0%) recorded large losses, US 30-year Treasury Bonds (+18.6%) fared very well, and the US Dollar Index (+6.0%) and gold bullion (+5.5%) also provided safe havens for risk-averse investors. (The returns for indices in individual countries are given in my December 31 "Stock market performance round-up".)

But the few trading days since Christmas Eve witnessed a strong rebound in global stock markets as investors brushed aside bleak economic data. This resulted in market participants scooping up beaten-down stocks and commodities, mending some of the bruising sustained earlier in 2008. The better spirit of equities was reflected in losses for some government bonds.

Despite a grim ISM report (see section on Economy below), the S&P 500 Index jumped by 3.2% after the release of the data, propelling many stock market indices to almost two-month highs. The MSCI World Index (+5.9%), MSCI Emerging Markets Index (+5.3%), Dow Jones Industrial Index (+6.1%), S&P 500 Index (+6.8%), Nasdaq Composite Index (+6.7%) and the Russell 2000 Index (+6.1%) all gained handsomely (albeit on thin volume) during the week straddling New Year's day.

Source: Daryl Cagle

December also marked the first monthly gain since August for the major US indices, with the Dow Jones and S&P 500 now up by 19.6% and 23.9% respectively since the lows of November 20, 2008.

The "storm" of 2008 has undoubtedly grown quieter in December, with the CBOE Volatility Index (VIX) having declined from 80.9 in November to 39.6 on Friday. Also, the average daily swing in the Dow Jones has fallen to ~300 points compared to ~430 points in November and ~590 points in October, according to Briefing.com.

Christmas Eve trading on Wednesday, December 24 marked the start of the Santa Claus Rally period, made up of the last five trading days of December and the first two of January. With one trading day to go on Monday, the combined gain for the S&P 500 Index for the first six days was 8.0%. The absence of a rally - and one now seems highly unlikely - has often been the harbinger of a sizeable correction or a bear market in the coming year. Hence the saying: "If Santa Claus should fail to call; bears may come to Broad & Wall."

But risks remain plentiful and Bill King (The King Report) reminds us that "just as night follows day, international conflicts follow economic crises". Escalating violence in the Middle East and tensions between Russia and the Ukraine served as a reminder and caused a 22.9% spike in the price of West Texas Intermediate Crude on the week.

Next, a quick textual analysis of my week's reading material (done between New Year's celebrations). No surprises here with keywords such as "economy", "financial", "market", "prices" and "rates" featuring prominently.

Readers often ask me about Richard Russell's (Dow Theory Letters) viewpoint on the stock market. Here is his latest take on matters: "It occurs to me that this is a good time to remember my old friend Marty Zweig's classic warnings: 'Don't fight the tape, don't fight the Fed'. Well, if you are bearish on 2009, you are indeed fighting the Fed and probably the tape. Why do I say that? Because the Bernanke Fed is going all out in its effort to turn the US economy around. Bernanke says the Fed will do whatever it takes to halt the current trend to deflation and to bring back prosperity and mild inflation to the US.

"The stock market seems to have finally climbed aboard the Fed's bullish bandwagon. All of which brings us to a very dramatic and critical juncture. If the market heads higher in early January, I believe that money on the sidelines [$8.85 trillion - 74% of US market cap] could begin to turn optimistic and even bullish," said the R man.

From across the pond, David Fuller (Fullermoney) added: "The crucial missing ingredient for stock markets to date has been confidence. Nevertheless that could change in January, given the high levels of cash held by most institutional investors. ... if stock market indices surprise the bearish consensus and start to break upwards rather than downwards from their trading ranges, institutional investors will be under increasing pressure to participate."

What the market does over the next few days will give a clue as to the rest of the year, according to Jeffrey Hirsch (Stock Trader's Almanac). "S&P gains during January's first five trading days preceded full-year gains 86% of the time." He also draws attention to the so-called "January Barometer" which states "as the S&P 500 Index goes in January, so goes the year". "The January Barometer predicts the year's course with a .741 batting average. 12 of the last 14 post-election years followed January's direction," said Hirsch. Also, the "ninth" year of decades is generally an up year for the stock market with the Dow Jones down only three times in the last twelve decades.

The table below shows the key resistance and support levels for the major US indices. With most global indices having breached the 50-day moving average (and after year-end also having taken out the December peaks), the next target is the November 4 highs, followed by the key 200-day average. On the downside, the December 1 (not shown on table) and the all-important November 20 lows must hold for the uptrend to remain intact.

In my opinion, selective buying in global markets is in order, and '09 may turn out to be a good year for a discerning stock picker. However, make sure to separate the wheat from the chaff because many companies will fall by the wayside during the new year. (Also see my posts "Stock market internals: further headway in 2009" and "Video-o-rama: Ring out the old, ring in the new" for more discussion of the outlook for stock markets in 2008.)

Economy

"Overall business confidence improved just a bit at the close of to 2008, but remains very dark with hiring intentions and expectations regarding the outlook in mid-2009 dropping to record lows," said the latest Survey of Business Confidence of the World conducted by Moody's Economy.com. The Survey results indicate that the entire global economy is solidly in recession.

Further evidence of the worldwide economic crisis came from the Semiconductor Industry Association, reporting that global sales of semiconductors declined by 9.8% in November compared with a year ago, and by 7.2% since the previous month.

Data reports released in the US during the New Year week mostly confirmed the dismal economic outlook.

• The Institute for Supply Management's Manufacturing Index is still contracting and fell by a larger-than-anticipated 3.8 points to 32.4 in December. The index is at its lowest level since 1980, with the forward-looking details also downbeat as new orders plunged to their lowest level since January 1948.

• The S&P/Case-Shiller Home Price Indices reported record annual declines, with the 10-City and 20-City Composite Indices falling by 19.1% and 18.0% respectively.

• The Conference Board's Consumer Confidence Index declined in December to a historic low of 38 - down by 6.6 points from November's 44.7. With consumer confidence in a perilous state, the outlook for spending appears dismal.

• Initial jobless claims decreased by 94,000 to 492,000 for the week ended December 27. Fewer-than-expected claims were filed, but holidays have been known to be more volatile for this indicator. Overall, labor market trends suggest persistent weakening.

• The ECRI Weekly Leading Index increased from 106.8 to 108 during the week ended December 26, but does not alter the Index's overall downward trend. The meaningful decline in the ECRI indicates a severe slowdown that could last deep into 2009.

Commenting on the implications of the worsening employment situation for the US consumer, Mark Vitner (Wachovia Economics Group) said credit availability and housing affordability were two important elements of consumer buying decisions, but that an even more important variable was consumers' comfort about their own employment and income prospects.

"Consumers typically have to have a job if they are going to buy a home or automobile. And even if consumers have a job, they are less likely to borrow and spend if they feel their job is at risk or their income could take a hit," said Vitner.

Elsewhere in the world, major economies remain mired in a severe slump. "Europe, Germany, France, and the UK all reported declines in indexes of purchasing managers in December," said Asha Bangalore (Northern Trust). China's factory sector has contracted for the fifth month running according to the CLSA China Purchasing Managers' Index. ... the Australian ... Manufacturing Index has recorded readings below 50 for seven consecutive months ... In sum, weak economic conditions across the world is a challenge for policy makers in the months ahead."

Source: US Global Investors - Weekly Investor Alert, January 2, 2009.

Assessing the global economic outlook, Nouriel Roubini (RGE Monitor) posed the following questions on RealClearMarkets: "So what lies ahead in 2009? Is the worst behind us or ahead of us?

"The United States will certainly experience its worst recession in decades, a deep and protracted contraction lasting about 24 months through the end of 2009. Moreover, the entire global economy will contract. There will be recession in the Eurozone, the UK, Continental Europe, Canada, Japan, and the other advanced economies. There is also a risk of a hard landing for emerging-market economies, as trade, financial and currency links transmit real and financial shocks to them," said Roubini.

Week's economic reports

Click here for the week's economy in pictures, courtesy of Jake of EconomPic Data.

| Date | Time (ET) | Statistic | For | Actual | Briefing Forecast | Market Expects | Prior |

| Jan 2 | 10:00 AM | ISM Index | Dec | 32.4 | 35.0 | 35.4 | 36.2 |

In addition to the Federal Open Market Committee (FOMC) releasing the minutes of its December 16 meeting (Tuesday, January 6) and the Bank of England's interest rate announcement (Thursday, January 8), the US economic highlights for the next week, courtesy of Northern Trust, include the following:

1. Employment Situation (January 9): Payroll employment is predicted to have dropped by 450,000 in December after a loss of 533,000 jobs in the prior month. The unemployment rate is expected to have risen to 7.0% during December from 6.7% in November. Consensus: Payrolls - -478,000 versus -533,000 in November, unemployment rate - 7.0% versus 6.7% in November.

2. Other reports: Consumer Confidence (December 30), Construction Spending, Auto Sales (January 5), Factory Orders, ISM Non-manufacturing, Pending Home Sales Index (January 6).

Markets

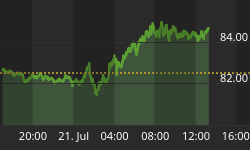

The performance chart obtained from the Wall Street Journal Online shows how different global markets performed during the past week.

Source: Wall Street Journal Online, January 2, 2009.

Good riddance to 2008! Let's hope that after one of the most tumultuous years in history, conditions will calm down - as always happens after a storm. And may this compilation of news items and words from the investment wise assist in keeping our portfolios on a profitable course.

To all the Investment Postcards readers, thank you for your loyalty and support. And remember, the biggest compliment you could give us is to broadcast word about the site and encourage your family, friends and colleagues to subscribe to the e-mail updates or RSS feeds.

Here's wishing you a blessed and calm 2009!

Source: Daryl Cagle

YouTube: Uncle Jay's review of 2008

"It's been a whole year since Uncle Jay has SUNG an entire episode, and here's the reminder why! It's the year-end review of the news, and maybe it'll seem a little better with music."

Source: YouTube, December 21, 2008.

The New York Times: The year in the markets

Click the image for an interactive graph.

Source: The New York Times, December 31, 2008 (hat tip: Barry Ritholtz).

Bloomberg: A recap of 2008

"A two-minute look into the year that changed the economic landscape."

Source: Bloomberg (via YouTube), December 31, 2008.

Win Rosenfeld (The Big Money): The five worst days of 2008

"You know it's been a bad year when you're arguing about what the five worst days were. Between the massive market fluctuations and the biggest banks going belly up, it's hard to know where to start. From a crowded field of contenders, here are The Big Money's five biggest buzz-killers."

Source: Win Rosenfeld, The Big Money, December 30, 2008.

Bloomberg: Marc Faber's 2009 outlook

Marc Faber says the global economy is going into severe recession and emerging markets will be hit the hardest.

Source: Bloomberg (via YouTube), December 31, 2008.

Bloomberg: Jim Rogers - "I'm prepared for the worst"

Source: Bloomberg (via YouTube), December 29, 2008.

CNBC: Map of the markets

"Where to put your money in 2009, with Michael Pento, Delta Global Advisors; David Kotok, Cumberland Advisors; Diane Brady, BusinessWeek; Dave Maney, Headwaters MB; and CNBC's Rebecca Jarvis."

Source: CNBC, December 31, 2008.

Bill King (The King Report): Unlikely that '09 will be as ugly as '08

"2008 will be a year of historic imfamy. The S&P 500 declined 38.5%, the biggest drop since 1937. The Dow Jones Industrial Average declined 33.8%, the largest drop since 1931.

"It is highly unlikely that 2009 will be as ugly. But this does not suggest that it will be a 'good' year.

"Back in October we commented that the stock market is following a clear historic pattern. A summer folly rally amid a receding economy and percolating financial duress produced an autumn collapse.

"And an October panic did not generate a low for stocks because during recessions, like in 1907 and 1929, October panic lows yield to new lows in November.

"But then a yearned rally appears. This usually extends into the first day or two of the New Year. But then January turns ugly on anticipated horrid earnings reports that will appear during the second and third weeks of the month. Finally there is a performance gaming rally over the last few days of January.

"When bonds rally sharply in Q4, they tend to make a significant peak early in January. Bonds by then are extended, even 'over-invested', and corporations and governments tend to burst the dyke by issuing beaucoup bonds for financing needs in the coming year.

"However, this year will be tricky because Weimar Ben is monetizing everything in sight. Weimar Ben can continue to monetize everything and anything - until the market revolts. And the revolt will likely come from the dollar.

"Though Ben and US solons desire a lower dollar in the hope of papering over the US's intractable structural problems, there is a line of demarcation for the dollar. If the dollar descents below that incalculable threshold, it's checkmate, Ben."

Source: Bill King, The King Report, January 2, 2009.

Financial Times: 2009 - predictions of some known unknowns

"The Financial Times team of pundits is back, once again, to risk its professional reputation on bold predictions of some known unknowns.

"Will the recession end in 2009?

"No, as far as the US, the UK, Spain and Ireland are concerned; possibly Yes for other European economies and Japan. Whatever happens, 2009 will not be pleasant. For all the cuts in interest rates and taxes, higher unemployment will be the dominant issue of the first half of the year, outweighing gains to real incomes from these policies and lower commodity prices. Uncertainty will be the watchword for the year, making any prediction precarious, but there is still a good chance that rising incomes will become powerful forces in the continental European and Japanese economies later in the year. For those economies that need much bigger rises in household savings rates to adjust for the recession, recoveries will be delayed. There is also a good chance the world will enter a debt-deflation trap, although I hope the authorities will do everything to avoid this. But even if we experience genuine green shoots of recovery, as I expect, 2009 will be a year to forget."

Click here for the full article.

Source: Financial Times, December 30, 2008.

Financial Times: Survey of economists - outlook for 2009

The Financial Times polled 67 leading economists for their views on the outlook for 2009. The full breakdown of their answers is given below.

1) Recession: How will this recession develop over the next twelve months? Will we see the green shoots of recovery by this time next year?

2) Risks: What are the three main risks that could profoundly exacerbate the recession? How concerned should people be?

3) Global outlook: Which part of the world will recover first and why?

Click here for the full article.

Source: Financial Times, January 1, 2009.

Edmund Conway (The Telegraph): Global economy to shrink for first time since the Second World War

"HSBC has warned that global gross domestic product will contract in 2009, describing this as 'an extraordinary development in the modern era'. In a comprehensive examination of the economic crisis, it predicts that next year will be the worst in peacetime both for rich countries and the wider global economy since the Great Depression.

"And in a further blow to the Chancellor Alistair Darling, the bank warned that the UK will endure its worst year of growth since the bleak winter recession of 1947, forcing the Bank of England to slash interest rates to only a quarter percentage point above zero. The gloomy forecasts are far more pessimistic than those from the Treasury or the International Monetary Fund.

"Stephen King, HSBC's chief economist, said: 'For a while, it was possible to pretend that the financial and economic crisis was merely a problem for the major industrialised countries.

"'Over the last three months, however, that theory has been blown out of the water. We have made savage downgrades to our forecasts with some of the emerging markets bearing the brunt of the bad news. On the basis of nominal GDP weights, we expect global GDP to shrink in 2009, an extraordinary development in the modern era.'

"He added that the serious risk now is that families and businesses will begin to hoard cash rather than spending it, as deflation rears its head across the rich world.

"'Stuffing cash under the mattress, however, will only end in cumulative tears,' he said. 'This, after all, was part of the dynamic associated with the Depression in the 1930s.'"

Source: Edmund Conway, The Telegraph, December 27, 2008.

Wolfgang Münchau (Financial Times): World economy in 2009 -- three priorities for recovery

"It is easy and difficult at the same time to predict the economy in 2009. It is easy to predict it will be an awful year for the US, Europe and large parts of Asia. The industrialised world will be in a deep synchronised recession. Global gross domestic product will probably contract also for the first time since the 1930s. There is not a great deal we can do to prevent this.

"The difficult part of the forecast is to predict whether policymakers will succeed in preventing the recession turning into a depression and lay the foundations for a sustainable recovery in 2010. What I can predict with near certainty is that policy will matter a great deal next year.

"We know that the current driving force behind this downturn is 'deleveraging'. Overindebted households and undercapitalised banks are adjusting their balance sheets, building up savings in the first case and restricting lending in the latter. There is no chance of a sustained economic recovery until that process is almost complete."

Click here for full article.

Source: Wolfgang Münchau, Financial Times, December 28, 2008.

Times Online: Car production faces global fall until 2010"Car production in North America will sink to its lowest level for more than 20 years next year and output in Europe will fall to a 12-year low, with Britain hit the hardest, according to PricewaterhouseCoopers (PwC).

"The accountancy firm is forecasting a 17% drop in the United States to 10.8 million cars and a 12% fall in the European Union to 15.5 million vehicles. Asia Pacific will experience the smallest fall, with a 5% decline to 26 million cars.

"PwC expects world production to fall by 10% to levels of output last seen in 2003.

"Calum McRae, automotive analyst at PwC, said: 'These figures demonstrate that there is further gloom to come before we can possibly see the effect of any bailouts or incentives.'"

Source: Christine Buckley, Times Online, December 30, 2008.

Financial Times: IMF argues for large stimulus packages

"Across-the-board tax cuts or bail-outs of troubled industries such as the automotive sector are likely to waste government money while doing little to stimulate the global economy, the International Monetary Fund warned on Monday.

"As governments around the world bring in tax cuts and boost spending to combat the global recession, a study by the IMF said such programs must be large but carefully designed.

"'There is a strong case for doing too much rather than too little,' said Olivier Blanchard, the fund's chief economist. But, he added, tax cuts should be aimed at people likely to spend money rather than save it.

"Although the IMF said it would resist giving a running commentary on policies, Mr Blanchard said signs of the stimulus plan emerging from the camp of US president-elect Barack Obama appeared to be hopeful. 'The size corresponds roughly to what we think is needed,' he said.

"Mr Obama's team is reportedly considering a fiscal stimulus worth $675 billion to $775 billion, or 5% to 6% of US gross domestic product, likely to include substantial long-term investment spending."

Source: Alan Beattie, Financial Times, December 29, 2008.

CNBC: Martin Feldstein on the stimulus package

"Discussing the kind of stimulus that should come out of Washington, with Martin Feldstein, Harvard University professor, President Emeritus of the National Bureau of Economic Research, & Council of Economic Advisors former chairman under President Reagan, with CNBC's Steve Liesman."

Source: CNBC, January 2, 2009.

Financial Times: GMAC gets $6 billion injection from US Treasury

"The US Treasury department late on Monday unveiled up to $6 billion in aid for GMAC, the financial services group which is critical to part-owner General Motors' turnaround.

"The Treasury said in a statement it would buy $5 billion in senior preferred equity with an 8% dividend from GMAC, characterizing the investment as part of 'a broader program to assist the domestic automotive industry in becoming financially viable'.

"It will also lend GM up to $1 billion to participate in a rights offering at GMAC in support of GMAC's reorganization as a bank holding company.

"Diminished access to capital had forced GMAC to cut back on vehicle financing, which in turn jeopardized GM itself.

"'With the Treasury investment, we intend to resume our automotive lending quickly,' GMAC spokeswoman Gina Proia said.

"The aid, which is being made under the Troubled Assets Relief Program (Tarp), comes after the Treasury earlier this month said it would extend a $17.4 billion emergency loan package to GM and Chrysler."

Source: Nicole Bullock, Henny Sender and Bernard Simon, Financial Times, December 29, 2008.

Karl Denninger (Market-Ticker): GMAC's "money-losing strategy" makes no sense

"The government 'buys' preferred equity that pays an 8% coupon. GMAC must pay that 8% coupon (9% if the government exercises the warrants).

"GMAC turns around and loans out money at 0% which it has to pay 8% to acquire, and at the same time decides that it will make loans to people with credit scores significantly worse than average, when before they would make loans only to people with scores that were slightly better than average. And we wonder how we got into this mess?

"The Federal Reserve and Treasury approved an application that contained as it's essence an intentional money-losing business strategy, enabling the literal looting of the public treasury under the false pretense of an 'investment'."

Source: Karl Denninger, Market-Ticker, December 31, 2008.

Financial Times: Fed pushes on with mortgage bond plan

"The Federal Reserve pushed ahead with its plan to buy mortgage bonds issued by Fannie Mae and Freddie Mac on Tuesday, saying it would start buying early next month and purchase up to $500 billion by the end of June.

"The aggressive tactics - the Fed had previously said it would buy this amount over 'several quarters' - highlights the central bank's determination to hammer down the risk spreads on the mortgage bonds and thereby reduce mortgage rates.

"The Fed also announced that it had selected four asset managers - BlackRock, Goldman Sachs, Pimco and Wellington Management - to manage the process. It had agreed a 'competitive fee structure' but did not disclose this.

"The Fed said 'the program is being established to support the mortgage and housing markets and to foster improved conditions in financial markets more generally'.

"The move comes as policymakers at the central bank and in both the outgoing Bush and incoming Obama administrations look to target mortgage rates in the hope that lowering them would arrest the decline in house prices and thereby support financial asset prices."

Source: Krishna Guha, Financial Times, December 30, 2008.

Bloomberg: Barclays's head says "worst is ahead" for US economy

"Ethan Harris, co-head of US economic research at Barclays Capital, and Richard DeKaser, chief economist at National City Corp., talk with Bloomberg's Peter Cook about the outlook for the US economy."

Source: Bloomberg (via Blinx), December 31, 2008.

Paul Krugman (The New York Times): The yield curve is wonkish

"I'm a little late getting to this, but ... I see that economists at the Cleveland Fed are taking some comfort from the positive slope of the yield curve. Long-term interest rates are higher than short-term rates, which is usually a sign that the economy will expand.

"Not this time, I'm afraid. It's all about the zero lower bound.

"The reason for the historical relationship between the slope of the yield curve and the economy's performance is that the long-term rate is, in effect, a prediction of future short-term rates. If investors expect the economy to contract, they also expect the Fed to cut rates, which tends to make the yield curve negatively sloped. If they expect the economy to expand, they expect the Fed to raise rates, making the yield curve positively sloped.

"But here's the thing: the Fed can't cut rates from here, because they're already zero. It can, however, raise rates. So the long-term rate has to be above the short-term rate, because under current conditions it's like an option price: short rates might move up, but they can't go down.

"Indeed, if we look at Japan we find that the yield curve was positively sloped all the way through the lost decade. In 1999-2000, with the zero interest rate policy in effect, long rates averaged about 1.75%, not too far below current rates in the United States.

"So sad to say, the yield curve doesn't offer any comfort. It's only telling us what we already know: that conventional monetary policy has literally hit bottom."

Source: Paul Krugman, The New York Times, December 27, 2008.

Karl Denninger (Market-Ticker): Uh oh ... monetary multiplier below zero

"What is this?

"I could go through the derivation of how money supply works in a fractional reserve monetary system, but won't, because most readers would have their eyes glaze over.

"The important part of this graph is what it denotes. Bernanke has lost control of 'N' (or velocity), which is the actual knob that he is trying to diddle when borrowing rates are changed (and in fact its the market that sets that, despite his protests).

"In fact the most useful tool in The Fed's box in terms of influencing monetary policy is the soapbox, that is, jawboning (whether it be by cajoling or threatening.)

"The problem with an M1 multiplier below one is that the effect of printing money is of course multiplied by the velocity. That is, if you print up $10 into the economy the impact it has on economic activity depends on how many times that $10 circulates in a given amount of time. The more it circulates the higher the impact and the more your efforts do for the economy.

"The bad news is that when the multiplier is less than one the more money you spew into the economy the worse the impact, as you get less for each additional dollar."

Source: Karl Denniger, Market-Ticker, December 30, 2008.

John Silvia (Wachovia Economics Group): ISM Manufacturing - economy remains in teeth of the recession

"December's ISM manufacturing index came in at 32.4, well within recession territory and consistent with levels of the 1980-82 recession period. Weakness remains in new orders, production and employment. The inventory correction is ongoing. Prices paid fell sharply to 1949 lows and suggests lower inflation ahead."

Source: John Silvia, Wachovia Economics Group, December 30, 2008.

Standard & Poor's: Case-Shiller - home price declines worsen

"Data through October 2008, released today [Tuesday] by Standard & Poor's for its S&P/Case-Shiller Home Price Indices, shows continued broad based declines in the prices of existing single family homes across the United States, with 14 of the 20 metro areas showing record rates of annual decline and 14 now reporting declines in excess of 10% versus October 2007.

"The chart above depicts the annual returns of the 10-City Composite and the 20-City Composite Home Price Indices. Following the lead of the 14 metro areas described above, the 10-City and 20-City Composites set new records, with annual declines of 19.1% and 18.0%, respectively.

"'The bear market continues; home prices are back to their March, 2004 levels.' says David Blitzer, Chairman of the Index Committee at Standard & Poor's. 'Both composite indices and 14 of the 20 metro areas are reporting new record rates of decline.'"

Source: Standard & Poor's, December 30, 2008.

Mark Vitner (Wachovia Economics Group): Consumer confidence falls to a new low"Worries about employment and income prospects were likely weighing on consumers' minds this holiday season, contributing to a larger than expected drop in consumer confidence. The Consumer Confidence Index fell 6.7 points to an all-time low of 38.0 in December, with most of the drop in the present situation series.

"While the present situation index is responsible for most of December's drop, the record low in the overall index is due mostly to consumers' extremely pessimistic view of future economic conditions. The present situation index plunged 12.9 points in December to 29.4, which is the lowest reading since the aftermath of the 1990/91 recession. The future expectations component, however, remains near all-time lows, even though it declined just 2.4 points to 43.8 December and remains above its October low.

"The Consumer Confidence Index is one of the longest running measures of consumer behavior, dating all the way back to 1947. The index has a very good record of tracking the performance of overall economic activity but has a very mixed record as a leading indicator."

Source: Mark Vitner, Wachovia Economics Group, December 30, 2008.

The Wall Street Journal: Retail sales plummet

"Price-slashing failed to rescue a bleak holiday season for beleaguered retailers, as sales plunged across most categories on shrinking consumer spending, according to new data released Thursday.

"Despite a flurry of last-minute shoppers lured by the deep discounts, total retail sales, excluding automobiles, fell over the year-earlier period by 5.5% in November and 8% in December through Christmas Eve, according to MasterCard Inc.'s SpendingPulse unit.

"When gasoline sales are excluded, the fall in overall retail sales is more modest: a 2.5% drop in November and a 4% decline in December. A 40% drop in gasoline prices over the year-earlier period contributed to the sharp decline in total sales.

"But considering individual sectors, 'This will go down as the one of the worst holiday sales seasons on record,' said Mary Delk, a director in the retail practice at consulting firm Deloitte LLP. 'Retailers went from 'Ho-ho' to 'Uh-oh' to 'Oh-no'."

"Luxury goods, once considered immune from economic turmoil, were hardest hit, with sales falling 21.2%, compared with a jump of 7.5% a year ago, when the economy had just begun to sputter. Including jewelry sales, the luxury sector plunged by a whopping 34.5%.

"During the same period last year, overall retail sales rose a modest 2.4%, helped by late-season discounting that enticed procrastinating shoppers. But this year, after a moderate uptick in shopping activity boosted by steep promotions the Friday after Thanksgiving, shoppers closed their wallets and reopened them only cautiously, worried by job losses, a sinking stock market and a recession climbing into its second year."

Source: Ann Zimmerman, Jennifer Saranow and Miguel Bustillo, The Wall Street Journal, December 26, 2008.

Reuters: Bush signs pension relief bill into law

"President George W. Bush on Tuesday signed into law a measure intended to help company pension plans and retirees that have been hard hit by the financial crisis.

"Despite some concerns about the legislation, Bush decided that in the current financial environment the benefits outweighed the problems, the White House said.

"Generally healthy multi-employer pension plans hurt by the stock market decline would not have to make drastic pension plan contribution increases and worker benefit cutbacks that many companies had feared.

"A multi-employer pension plan, unlike a traditional single-employer plan, covers workers from more than one company and allows workers to move from job to job and still contribute to the plan.

"People 70-1/2 years old or older would not have to take distributions from their retirement plans as required under current law, allowing them to keep savings intact and avoid a bear-market tax hit.

"White House spokesman Tony Fratto said the administration had concerns that the legislation would increase the costs of near-term claims on the Pension Benefit Guaranty Corporation and could result in some benefits lost to workers over the long term. 'Our concerns with the legislation remain, but we do believe that, in this current economic environment and current economic circumstances, that the benefits of the legislation outweighed our objections,' he said."

Source: Tabassum Zakaria, Reuters, December 23, 2008.

Financial Times: Auditors urge rethink on pension

"Auditors are pressing companies to reconsider how they calculate their pension liabilities and urging them to use formulas that could give rise to much larger reported deficits than would be the case if they stayed with the current approach.

Market volatility has raised questions over the so-called 'discount rate' used to calculate the present-day value of a fund's future liabilities.

"The lower the rate used, the higher the present liabilities will be. The rates currently used by companies to calculate those liabilities are roughly equivalent to those on less risky high-grade corporate bonds. However, these have soared amid the market turmoil, sharply shrinking reported fund deficits.

"Some schemes have actually reported a surplus even as the values of the stocks they hold have plunged."

Source: Norma Cohen and Jennifer Hughes, Financial Times, December 30, 2008.

Financial Times: Money flows out of hedge funds at record rate

"Investors pulled a net $32 billion from hedge funds last month, making 2008 the first year in their recorded history that the funds have had significant outflows and ending the industry's 18 years of asset growth.

"Money has been taken out of funds following every strategy, even those - such as macro funds - which were showing returns, according to data from fund trackers Hedge Fund Research.

"The funds enjoyed net inflows for the first part of the year, even as the financial crisis hit and traditional mutual funds began to show outflows.

"However, in September a tide of redemptions began, according to TrimTabs, another fund tracker.

"Conrad Gann, chief operating officer of TrimTabs, said: 'We estimate outflows in November were $32 billion, and there is an additional pipeline of redemptions that have not been filled, there could be $80 billion [of redemptions] in December.

"'There are $57 billion of redemptions that we know are in, that are not reflected yet,' he said.

"Mr Gann said it was difficult to estimate outflows for coming months because hedge funds had different redemption cycles.

"In recent months funds have also tried to halt outflows by limiting or suspending investor withdrawals. This means that data on outflows, which reflect actual repayments to investors, understates the true picture.

"This is the first year since at least 1990 that hedge funds have seen a drop in assets."

Source: Deborah Brewster, Financial Times, December 30, 2008.

MarketWatch: Sam Stovall bullish on 2009, his father less so

"It's been a horrible year for stocks overall - the worst, in fact, since 1931. Oft-cited market pundit Sam Stovall of Standard & Poor's and his father, Robert Stovall, a veteran money manager at Wood Asset Management, review the past year with MarketWatch's Steve Gelsi."

Source: MarketWatch, December 31, 2008.

Richard Russell: Stock crashes have look of completed declines

"Over the weekend, I reviewed the charts of hundreds of leading NYSE stocks. Many of these stocks have crashed. In almost all cases, RSI has plunged to severely oversold levels. I note that at the end of each crash, the price action has been forming a sideways pattern. These numerous crashes have the look of completed declines - declines from which bases are forming. Following a true crash, stocks and stock averages have a habit of recovering roughly 50% of the action lost in the crash.

"And I'm wondering whether these patterns are now indicating that a tradeable low has been reached by this bear market. The news continues awful, and yet these various stock bottoms, following crashes, appear to be holding."

Source: Richard Russell, Dow Theory Letters, December 29, 2008.

Bloomberg: Leuthold - cash at 18-year high makes stocks a buy

"There's more cash available to buy shares than at any time in almost two decades, a sign to some of the most successful investors that equities will rebound after the worst year for US stocks since the Great Depression.

"The $8.85 trillion held in cash, bank deposits and money-market funds is equal to 74% of the market value of US companies, the highest ratio since 1990, according to Federal Reserve data compiled by Leuthold Group and Bloomberg.

Leuthold, Invesco Aim Advisors, Hennessy Advisors and BlackRock, which together oversee almost $1.7 trillion, say that's a sign the Standard & Poor's 500 Index will rise after $1 trillion in credit losses sent the benchmark index for American equities to the biggest annual drop since 1931. The eight previous times that cash peaked compared with the market's capitalization the S&P 500 rose an average 24% in six months, data compiled by Bloomberg show.

"'There is a store of cash out there that is able to take the market higher,' said Eric Bjorgen, who helps oversee $3.4 billion at Leuthold in Minneapolis. 'The same dollar you had last year buys you twice as much S&P 500 as it did a year ago.'

"Leuthold Group, whose Grizzly Short Fund returned 83% in 2008 thanks to bets against equities, said in its December bulletin to investors that stocks offer 'one of the great buying opportunities of your lifetime'."

Source: Eric Martin and Michael Tsang, Bloomberg, December 29, 2008.

David Fuller: 10 tangible reasons for a rally

"I have listed and illustrated 10 tangible reasons for a rally (no cheerleading here), and also discussed a crucial missing ingredient.

1. Governments have flooded the system with liquidity. It takes time for this to filter through to the economy but it will reach the stock market more quickly.

2. Interest rates are at record lows for the US and UK, both short-term and long-term, and heading lower elsewhere. This is an ideal background for stock market recoveries.

3. Valuations are much improved, despite legitimate concerns over the earnings outlook for at least the first half of 2009. Equity yields are competitive with government bond yields, despite the near certainty of more dividend cuts than increases over the next six months.

4. Corporate bond yields peaked in October and November and have fallen significantly. They have also begun to improve their performance relative to government bonds.

5. Various measures of investor/advisor sentiment reached extreme lows in October.

6. The VIX Index peaked in October and is trending lower.

7. Commodity indices have fallen significantly, lowering inflationary pressures. Historically, equities have done best in disinflationary environments.

8. In many countries, the financial sector is showing strength relative to the broader indices. This is a key lead indicator.

9. Levels of cash are at record highs.

10. Most broad stock market indices show some evidence of base formation development. This is less clear for the DOW, but can be seen for the FTSE 100, DAX, SX5E, FSSTI and NKY, to mention a few of many.

"In conclusion, technical evidence remains more conducive to a stock market rally rather than another slump. Over the last three weeks we have repeatedly mentioned the December reaction lows. They need to hold to remain consistent with our expectations for a ranging stock market recovery extending well into Q1 2009.

"The crucial missing ingredient for stock markets to date has been confidence. Nevertheless that could change in January, given the high levels of cash held by most institutional investors. If stock markets languish in the New Year, as many expect, there will be little reason for investors to reinvest in the stock market. However, if stock market indices surprise the bearish consensus and start to break upwards rather than downwards from their trading ranges, institutional investors will be under increasing pressure to participate. Failure to do so would put them at a competitive disadvantage in terms of 2009's performance.

"Lastly, if the global economy does not show evidence that the recession is ending by Q3 2009, in response to the stimulus programmes, stock markets will be susceptible to a significant retracement of gains achieved during the first half of the year."

Source: David Fuller, Fullermoney, December 30, 2008.

Barron's: Seasonal patterns for the market

"Barron's Michael Santoli discusses what market patterns to expect in the closing days of 2008 and the beginning of 2009."

Source: Barron's, December 29, 2008.

Bespoke: Estimated earnings growth for the S&P 500

"Below we highlight historical earnings growth estimates for the S&P 500 for Q4 2008 and full-year 2009. As shown, EPS estimates have dropped sharply over the last few months, and analysts are currently expecting the S&P 500 to see year-over-year earnings fall by 12% in the fourth quarter.

"At the start of September, analysts were actually expecting growth of 40%, which was largely because financial companies were expected to bounce back from a very poor Q4 in 2007. Instead, these companies are struggling much more than they were at this time last year.

"Estimates for 2009 have been dropping significantly as well. Back in September, analysts were expecting 2009 earnings growth of 24.7% versus 2008. But estimates are now at just 4.5%, and judging by the current trend, analysts will be looking for negative 2009 growth in no time.

"Earnings for Materials are expected to fall the most at -63%, while Consumer Staples and Health Care are the only two sectors expected to see year over year growth."

Source: Bespoke, December 29, 2008.

John Hussman (Hussman Funds): Prices of Treasury bonds at dangerous levels

"... bond yields at this point are vulnerable to very sharp reversals. Given the level of extension in yields, it would not be difficult for the bond market to generate losses of say 10% in the 10-year Treasury bond, and as much as 20% to 25% in the 30-year Treasury bond over a very short period of time. Straight Treasuries may have safety from default risk, but the price risk is becoming downright dangerous.

"Corporate yields are much more reasonable, but there will be more fallout in this sector, and as I've noted before, taking a significant position in corporate would be essentially like a 'bottom call' in stocks, since corporate bonds tend to trade much like stocks during periods of elevated default risk.

"For our part, we strongly prefer Treasury inflation protected securities here. Despite near term deflationary prospects, the enormous expansion in government liabilities is unlikely to be accompanied by long-term inflation rates near zero, which is essentially the level that is priced into TIPS at present."

Source: John Hussman, Hussman Funds, December 29, 2008.

{kind=link}

{kind=link}