Our 2009 screening and ranking process included literally thousands of investment options. In addition to our standard watch list of roughly 200 investment alternatives, we also used several stock scanning models to identify other potential sources of opportunity. The final results left us with a collection of investments which congregated around the following overlapping investment themes:

- Expansion of the money supply / fiat currency concerns / inflation

- Commodities, clean energy, and water

- Economic shift from United States to Asia

- Infrastructure & government programs

- Baby boomer's transition from consumers to savers / consumer deleveraging

Since all investments involve opportunity costs, it is important to compare and rank investment alternatives. Our basic investment philosophy focuses on asset classes and their relative attractiveness. Given the state of the economic landscape and unprecedented actions from policymakers, we have broadened our scope of investment options to include individual stocks. Adding individual stocks allows us to more easily identify the major investment themes that are driving the markets. Many of these investment themes can be worked into our strategy using an asset class by investing in an index or specialty exchange-traded fund (ETF). In some cases, we may be better served to gain exposure to an investment theme via an individual stock or bond.

No Guarantee Government Polices Will Work

Despite recent gains, almost all major financial markets remain firmly in downtrends as we enter 2009. Some signs of technical improvement have come in recent weeks, but little to no change has occurred yet in long-term trends. Our screens and preparation for 2009 should not lead you to believe that all is well and money is surely to be made this year. Prudent and conservative entry and exit points for all investments will continue to be an important part of our risk management process. In simplified terms, we will hold on to winning investments and prudently cut losses on the inevitable poor performers. We will also be patient with entry points rather than blindly chase what easily could turn out to be a bear market rally. We are concerned about our performance over the next several years, not the first two weeks of 2009. When a new bull market finally arrives in some asset classes, there will be ample time to profit from the trend. A few positive early signals have been given, but not enough to declare an end to the bear market.

Theme One: Expansion Of The Money Supply

We have covered this topic for years, so there is nothing really new in this area except the alarming increase in the pace of the government's printing presses and ever-expanding scope of market intervention. A recent review of this theme can be found in Does The U.S. Government Print Money? and on this Weak U.S. Dollar page. Stocks of gold and silver mining companies (GDX, RGLD) and physical gold (GLD) and silver (SLV) scored well in the rankings. At the present time, the stocks appear more attractive than the physical metals, but that is subject to change in the event of further stock market losses. With financial deleveraging still taking place, the vast majority of investments, including those outlined here, carry above average risk. These investment themes and possible investment options were complied to help us be better prepared in the event the markets begin to focus on inflation rather than deflation. They are not presented as "buy at the market and hold them for 2009" ideas.

Theme Two: Commodities, Energy, Water, Green Technology

Although slowed by economic realities, demand for all goods is being created as more and more people around the globe migrate from poverty and the lower class to the lower-middle class. Expanding opportunities in Asia are helping people trade in bikes for cars. Access to better wages means moving up a rung on the economic ladder, which creates demand for more nutrient-rich foods, and consumer goods. This trend is a long-term driver for commodities. From a supply standpoint, the current credit crisis and economic downturn have caused many commodity producers to cancel capital-intensive projects. When the global economy improves, we may be looking at high commodity prices in short order. Government policies around the globe are pumping the financial system with fiat currencies. Once some of this money makes its way through the system, it will put additional upward pressure on all prices, including commodities.

Clean energy and green technologies are a subset of this theme. We can expect the government programs theme to provide support to environmentally friendly solutions in all fields. Since commodities are "hard" assets, they offer a way to protect investors from a weak dollar, increases in the money supply, paper currencies, inflation, etc. Therefore, the weak dollar and commodity themes are somewhat interchangeable.

Theme Three: Economic Shift To Asia

In line with the natural laws of the universe, the NFL's once dominant New England Patriots missed this year's playoffs. The Pats had a good year, but not as good as in recent years. Contrary to popular belief, global power also shifts according to natural laws. Changes in demographics, regulatory structures, technology, and countless other factors all point toward a gradual decline in America's global power. Britain was once the king of the hill and the pound was the world's reserve currency. Over time, power slowly shifted to the United States. The U.S. dollar replaced the pound as the world's reserve currency. A similar gradual shift is taking place today with power migrating toward Asia. While the timing is uncertain, the U.S. dollar one day may cease to be the preferred medium of exchange.

Theme Four: Infrastructure and Government Programs

In the unlikely event you had not noticed, the U.S. government now has an active role in the future of banks, insurance companies, automobile manufacturers, and brokerage firms. Numerous stakes have been taken and guarantees made. The Obama administration is working on a stimulus package which includes spending on roads, bridges, and other infrastructure. The infrastructure package may pump between $850 billion to $1 trillion into the economy. While economic fundamentals remain very concerning, we cannot ignore massive amounts of government spending; especially from a government that can seemingly print an endless supply of new money. We are rapidly moving into a period of "big government". Therefore, any company, sector, or asset class that can benefit from the expansion of government is related to this theme.

Theme Five: Baby Boomers Shift From Consumers To Savers / Consumer Deleveraging

Credit helped fuel the age of consumerism. Americans, and many foreigners, shifted from a "depression mentality" to a "McMansion mentality". This trend was sustainable when the baby boomers were in their prime earning years. It is no longer sustainable as the baby boomers head to retirement. The recent massive destruction in wealth caused by falling stock and home values may have served as a wake up call. The baby boomers may now realize saving is not such a bad idea. As personal savings increase, personal consumption and spending contracts. When consumers pull back their wallets, economic growth and output will suffer. This new trend is largely based on demographics, which cannot be altered by printing money or building bridges. The boomer theme also relates to the increased demand for health care, pharmaceuticals, and any product or service that can assist an aging population.

While the boomers represent the primary driver for this theme, consumers of all ages will have to make smarter purchasing and savings decisions in a weak economy where access to credit is limited, job security is diminishing, and net worth was hit with falling stock and home prices. The boomer/deleveraging theme is somewhat of a weak economy theme as well. For example, tobacco products and beer are considered to be recession proof since people will still smoke and drink even in a down economy.

What We Know As Of January 6, 2009

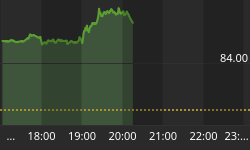

Economic fundamentals remain weak. Valuations are moderately attractive. The technicals are weak but showing some renewed signs of life. On many fronts, we see what appears to be a gradual reduction in risk aversion. We may also be seeing a little less fear of deflation and more concern about inflation. Asset prices tend to bottom between one and six months before the economy. We must allow for the possibility of investment gains before we see an economic improvement. The fear of missing a bottom may also be a catalyst if the recent gains and technical improvements can continue. Money is being created out of thin air and pumped into the economy. Investors should pay attention, keep an open mind, and be prepared for bullish and bearish outcomes. It is entirely possible we may be past the point where everything goes down. Some assets may begin to separate themselves from the pack in 2009, which means there will come a time to put some more capital to work. The chart below of the S&P 500 may help with the fears that we "are missing something" holding onto cash as the market makes "big gains" off the November 2008 lows. If you look at the percentages, these "big gains" have barely put a dent in the real losses that buy and hold investors have experienced since the market peaked in October of 2007. There will be plenty of time to make money when the odds shift back into our favor. These same concepts apply to almost all markets and all asset classes. When oil finds a bottom, we can afford to "miss" some of the early gains and still have an opportunity for excellent returns.

Final Thoughts As We Head Into 2009

- We are in a deflationary environment where principal protection remains the primary objective.

- A safe haven for the majority of your investment assets must be maintained until the deleveraging process has run it course and some semblance of order returns to the financial system.

- The severe dislocations in the economy and financial system will not be repaired in short order. Problems in the housing, credit, and financial markets are significant and cannot easily be corrected with government policy or intervention.

- As a result, even a well thought out investment approach using multiple asset classes must be adjusted to align with vastly different conditions. Credit events of this magnitude are very rare and thus are not easily addressed with even the most elaborate diversification strategies, including those developed by CCM. Our willingness to raise cash very early in this cycle and not blindly rely on asset class diversification shows we understand the state of the financial system and are willing to make the necessary adjustments to our investment approach and models. We have made adjustments and will continue to do so if conditions warrant.

- Actions already taken by policy makers and those being proposed by the Obama administration are sowing the seeds of future inflation, possibly severe inflation.

- Contingency plans mush be in place to deal with the possibility of rapid changes in market participant's willingness to take on risk as they transition from the well-founded fear of deflation to the well-founded fear of inflation. The transition of markets from a deflationary bias to an inflationary bias may take place at a surprisingly rapid rate.

- Contingency plans must be developed from a strategic perspective and implemented with tight risk management controls and proven tactics.

- Plans must include the almost inevitable need to protect the purchasing power of your assets at some point in the future.

- While we would prefer to maintain a fully invested position using multiple asset classes as a source of diversification, current conditions necessitate a different and more flexible approach.

- If deflation continues, the five major investment themes covered in this outlook may be of little value. However, if and when inflation begins to rear its ugly head, they will represent a good source of ideas to assist us with preserving the purchasing power of our assets. The technical screen below was compiled from literally thousands of investment options. It tells us at the present time many investors are concerned about future inflation (green & orange boxes). Economic weakness has been acknowledged via the heavy interest in the boomers/consumer deleveraging theme (yellow boxes). The frequency of results related to the infrastructure & government programs theme (see blue boxes), also points towards "big government" and massive amounts of deficit spending. Finally, the interest by market participants in the economic shift to Asia theme (purple boxes) also ties into concerns about U.S. inflation and the possibility of a weaker currency. The rankings below are one way of "listening to the market." The rankings also are an example of paying attention to what is actually happening rather than what we think may happen.

It Is Not Urgent To Redeploy Cash, But You Should Stand Ready

Since deflation is still the dominant theme in the minds of market participants, it is prudent to make the market prove to you that it can move higher. If you pick several entry points above current market prices for any investment, you enter markets only if real strength is present. If the investments cannot move through these price points (meaning they are not going up), you remain patient (and in cash).