The good news is:

• The market is oversold going into a seasonally strong period.

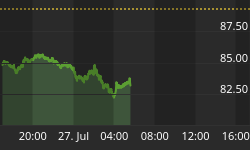

Short Term

After 3 consecutive down weeks the market is oversold.

The chart below covers the past 6 months showing the S&P 500 (SPX) in green and an indicator that is momentum of the McClellan Oscillator (MCO) calculated from NYSE advance - decline data in brown.

The MCO is a 5% trend (39 day EMA) subtracted from a 10% trend (19 day EMA) of NYSE declining issues subtracted from advancing issues. Momentum is a combination of Stochastics and RSI.

The indicator is at its lowest point at any time in the last 6 months and the previous lows have been followed by short term advances.

Intermediate term

New lows increased again last week.

Although the number of new lows at the November low was less than the October low there were still enough to imply a high likelihood of a retest of the November lows.

The chart below covers the past 6 months showing the NASDAQ composite (OTC) in blue and a 10% trend of NASDAQ new lows (OTC NL) in black. OTC NL has been plotted on an inverted Y axis so decreasing new lows move the indicator upward (up is good).

The indicator continued to move downward last week. The current value of the indicator is 83 so the indicator will move downward when there are more than 83 new lows.

The pattern I like to see at bottoms is one of strengthening secondaries while the blue chips retest their old lows and that pattern appears to be developing.

The chart below covers the period from the November lows through last Friday showing all of the major indices on semi log scales to show relative performance.

The Dow Jones Industrial Average (DJIA), shown in magenta, is the bluest of the blue and has been the worst performing since the November lows (up 6.96%) while the S&P mid cap (MID), shown in cyan, has been the best (up20.21%) followed by the Russell 2000 (R2K) (up 15.33%. The other indices shown are the SPX in green (up 10.57%) and the OTC (up 12.25%).

Another indicator offering some hope is NYSE On Balance Volume (NY OBV) which is a running total of NYSE declining volume subtracted from advancing volume.

The chart below covers the past year and a half showing the SPX in green and NY OBV in brown. NY OBV lead the way down from the October 2007 high through the November 2008 low and now appears to be leading the way up.

Seasonality

Next week includes the last 5 trading days of January during the 1st year of the Presidential Cycle.

The tables show the daily return on a percentage basis for the last 5 trading days of January during the 1st year of the Presidential Cycle. OTC data covers the period from 1963 - 2008 and S&P 500 (SPX) data from 1928 - 2008. There are summaries for both the 1st year of the Presidential Cycle and all years combined.

By all measures the period has been modestly positive. Interestingly, Monday has had a negative average return by all measures while the remaining 4 days of the week have been up by all measures.

Last 5 days January.

The number following the year represents its position in the presidential cycle.

The number following the daily return represents the day of the week;

1 = Monday, 2 = Tuesday etc.

| OTC Presidential Year 1 | ||||||

| Day5 | Day4 | Day3 | Day2 | Day1 | Totals | |

| 1965-1 | 0.61% 1 | 0.39% 2 | 0.62% 3 | 0.75% 4 | 0.36% 5 | 2.72% |

| 1969-1 | 0.23% 1 | -0.14% 2 | 0.09% 3 | 0.22% 4 | 0.39% 5 | 0.79% |

| 1973-1 | -1.47% 3 | -0.56% 5 | 0.00% 1 | -1.00% 2 | -0.19% 3 | -3.22% |

| 1977-1 | -0.32% 2 | -0.57% 3 | -0.49% 4 | -0.33% 5 | -0.19% 1 | -1.89% |

| 1981-1 | -1.20% 1 | 1.05% 2 | -0.41% 3 | 0.26% 4 | -0.04% 5 | -0.34% |

| 1985-1 | 0.61% 5 | 0.38% 1 | 0.41% 2 | 0.87% 3 | 0.04% 4 | 2.32% |

| Avg | -0.43% | 0.03% | -0.08% | 0.00% | 0.01% | -0.47% |

| 1989-1 | 0.52% 3 | 0.78% 4 | 0.22% 5 | 0.32% 1 | 0.52% 2 | 2.35% |

| 1993-1 | 0.76% 1 | 0.03% 2 | -1.31% 3 | -0.46% 4 | 0.24% 5 | -0.74% |

| 1997-1 | -0.81% 1 | 0.12% 2 | 0.06% 3 | 1.17% 4 | 0.65% 5 | 1.19% |

| 2001-1 | -3.67% 4 | 0.98% 5 | 2.05% 1 | 0.00% 2 | -2.31% 3 | -2.95% |

| 2005-1 | 0.56% 2 | 1.29% 3 | 0.05% 4 | -0.55% 5 | 1.31% 1 | 2.66% |

| Avg | -0.53% | 0.64% | 0.21% | 0.09% | 0.08% | 0.50% |

| OTC Summary for Presidential Year 1 1965 - 2005 | ||||||

| Averages | -0.38% | 0.34% | 0.12% | 0.11% | 0.07% | 0.26% |

| % Winners | 55% | 73% | 64% | 64% | 64% | 55% |

| MDD 1/25/2001 3.67% -- 1/31/1973 3.19% -- 1/31/1977 1.88% | ||||||

| OTC Summary for all years 1963 - 2008 | ||||||

| Averages | -0.08% | 0.18% | 0.07% | 0.09% | 0.35% | 0.59% |

| % Winners | 40% | 61% | 61% | 60% | 67% | 59% |

| MDD 1/28/2000 6.73% -- 1/30/1970 4.76% -- 1/30/2004 4.07% | ||||||

| SPX Presidential Year 1 | ||||||

| Day5 | Day4 | Day3 | Day2 | Day1 | Totals | |

| 1929-1 | -0.20% 6 | -0.31% 1 | 0.04% 2 | 0.35% 3 | 1.14% 4 | 1.02% |

| 1933-1 | -0.70% 4 | -0.14% 5 | -1.14% 6 | 0.29% 1 | -0.57% 2 | -2.27% |

| 1937-1 | -1.46% 2 | 0.80% 3 | -0.11% 4 | 0.79% 5 | 0.34% 6 | 0.35% |

| 1941-1 | 0.00% 1 | -0.57% 2 | -2.01% 3 | -1.76% 4 | 0.30% 5 | -4.05% |

| 1945-1 | 0.98% 5 | 0.45% 6 | 0.15% 1 | -0.59% 2 | 0.07% 3 | 1.05% |

| Avg | -0.28% | 0.04% | -0.62% | -0.18% | 0.26% | -0.78% |

| 1949-1 | -0.26% 3 | -0.26% 4 | -0.33% 5 | 0.20% 6 | -0.07% 1 | -0.72% |

| 1953-1 | -0.19% 1 | 0.12% 2 | 0.31% 3 | 0.27% 4 | 0.69% 5 | 1.19% |

| 1957-1 | -0.47% 5 | -0.74% 1 | 0.49% 2 | 0.45% 3 | -0.42% 4 | -0.68% |

| 1961-1 | 0.13% 3 | 0.15% 4 | 1.02% 5 | 1.19% 1 | -0.31% 2 | 2.19% |

| 1965-1 | 0.14% 1 | 0.09% 2 | 0.33% 3 | 0.29% 4 | 0.09% 5 | 0.94% |

| Avg | -0.13% | -0.13% | 0.37% | 0.48% | 0.00% | 0.58% |

| 1969-1 | 0.02% 1 | 0.01% 2 | 0.10% 3 | 0.04% 4 | 0.45% 5 | 0.61% |

| 1973-1 | -1.26% 3 | -0.24% 5 | -0.38% 1 | -0.16% 2 | 0.17% 3 | -1.86% |

| 1977-1 | -0.12% 2 | -0.77% 3 | -0.54% 4 | 0.14% 5 | 0.10% 1 | -1.18% |

| 1981-1 | -0.30% 1 | 0.99% 2 | -0.59% 3 | -0.08% 4 | -0.53% 5 | -0.52% |

| 1985-1 | 0.36% 5 | 0.03% 1 | -0.03% 2 | 1.15% 3 | 0.13% 4 | 1.65% |

| Avg | -0.26% | 0.00% | -0.29% | 0.22% | 0.06% | -0.26% |

| 1989-1 | 0.23% 3 | 0.88% 4 | 0.73% 5 | 0.40% 1 | 0.84% 2 | 3.08% |

| 1993-1 | 0.89% 1 | -0.01% 2 | -0.42% 3 | 0.13% 4 | 0.03% 5 | 0.62% |

| 1997-1 | -0.71% 1 | 0.00% 2 | 0.98% 3 | 1.51% 4 | 0.25% 5 | 2.03% |

| 2001-1 | -0.50% 4 | -0.19% 5 | 0.68% 1 | 0.70% 2 | -0.56% 3 | 0.13% |

| 2005-1 | 0.40% 2 | 0.48% 3 | 0.04% 4 | -0.27% 5 | 0.85% 1 | 1.50% |

| Avg | 0.06% | 0.23% | 0.40% | 0.49% | 0.28% | 1.47% |

| SPX summary for Presidential Year 1 1929 - 2005 | ||||||

| Averages | -0.15% | 0.04% | -0.03% | 0.25% | 0.15% | 0.25% |

| % Winners | 40% | 50% | 55% | 75% | 70% | 65% |

| MDD 1/30/1941 4.29% -- 1/31/1933 2.25% -- 1/30/1973 2.02% | ||||||

| SPX summary for all years 1928 - 2008 | ||||||

| Averages | -0.06% | 0.15% | 0.02% | 0.16% | 0.31% | 0.57% |

| % Winners | 49% | 53% | 48% | 63% | 65% | 60% |

| MDD 1/29/1938 6.33% -- 1/30/1932 5.05% -- 1/30/1970 4.55% | ||||||

Money Supply

The chart below was provided by Gordon Harms. Money supply has been growing faster than any time since late 1998. It is unlikely the market will fall significantly with money supply growing at this pace.

Conclusion

The market is oversold and appears to be developing a positive bottom pattern.

I expect the major indices to be higher on Friday January 30 than they were on Friday January 23.

This report is free to anyone who wants it, so please tell your friends. They can sign up at: http://alphaim.net/signup.html. If it is not for you, reply with REMOVE in the subject line.

Gordon Harms produces a Power Point for our local timing group. You can get a copy of the most recent one at: http://www.stockmarket-ta.com/.

Thank you,