This is a follow up to the 2009 year forecast issued on Jan 16, 2009

In the first quarter of 2009, we reached the climax of US banking and financial collapse.

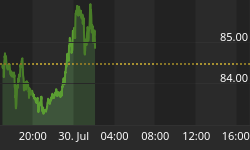

* Citigroup was brought down by souring mortgages and traded below a dollar. US government now has a controlling stake.

* Dow Jones traded below 7,000, not seen since 1998.

* The Fed having printed over $1.5 trillion to buy bad debts, promised to print $trillions more to buy mortgages and long term US treasuries to keep rates low

* Global central banks lowered and kept interest rates nearing zero percent

* Asian markets and commodities markets gathered momentum and broke away from US equities. Oil surged $15 from the low $35 to trade at $50.

Citigroup's 20 year chart and stunning fall from grace.

Our January calls so far have been mostly on track. What's in store for Q2 2009?

Gold:

We said in January:

"I look for side-way action for gold between $700 and $1,000 / oz as markets battle through fears of depression to come to grip s with inflation."

Gold acted stronger than we expected this quarter as it broke through the year-long consolidation. The Citibank crisis and bold moves by central banks to monetize debts forced global savers to seek refuge in gold. Fiscal deficits and record low rates will further provide momentum for gold. The chance of reaching past $1,000/oz has been further bolstered by oil's strong comeback at $50. For Q2 I look for range bound between $850/oz and $1,000/oz.

US Dollar:

We said in January:

"The factors that drove up the dollar are temporary; therefore a dollar correction could be underway soon. I see dollar index between 88 and 72 for 2009."

The dollar performed its best act and was squeezed to 89 before long term poor fundamentals come back in to play. I look for a dollar correction that will take the index back 80 in Q2 and 75 in 2009. However, an unlikely breakout over 90 would mean we are wrong about the dollar's bear trend.

S&P 500:

We said in January

"Today's dollar is perhaps half of what it was 10 years ago. The S&P500 index is trading at a decade low . At zero % interest rate, I don't see much downside and would peg S&P500 between 800 and 1,200 for 2009."

S&P500 staged a panic bottom in Q1 from banking crisis and is back trading above 800 level. With zero% interest rate and vast money looking for a home, we are neutral to mildly positive on the index.

Gold Stocks:

We wrote in January

"I am not wildly bullish on gold stocks yet as speculative spirits could take months to return . However a modest rebound to 150 from current 105 is very reasonable and represents healthy percentage gains."

The XAU zoomed to 140 in Q1, which is quite extraordinary given the extremely poor climate in equity markets. There is a lot of resistance ahead at 150 which will likely cap the index for Q2 while base metal and energy sectors play catch up.

Oil, Copper, Silver:

In January we wrote:

"Faced with imminent dollar correction and inflationary monetary policies, commodities at today's prices have more room to go up than down, particularly zinc which peaked much earlier and therefore has a stronger base. My calls for oil are between $40-$60 /barrel , copper $1.25-$2 /pound , silver $10-$15 /oz, and zinc 60cents to $1/pound ."

In Q1, China started stockpiling base metals and energy markets started to return to normalcy from extreme margin selloff. Remember, commodity prices go up regardless of economic activities in times of inflation, just ask the Zimbabweans with 85% unemployment and a loaf of bread costing 1 trillion Zimbabwean dollars.

Base metals and oil have staged very healthy gains in Q1, prompting us to possibly raise our above target for the year. For Q2, oil is likely to be between $40 and $60, while copper stays between $1.75 - $2.25

S&P TSX Ventures Index (Proxy to Junior Mining Stocks):

We wrote in January

"In the heat of the credit crunch in Nov 2008, we saw a handful of junior mining issues trading at upwards of 70% discount to cash values. Toronto saw zero IPOs in Q3. Unless oil dives to $20 and copper goes below $1, I would say the capitulation has already occurred in the junior resource sector.

Majors such as Teck and Rio Tinto are straddled with debt and depressed commodity prices , this make s junior buyouts less likely. Financing junior issues will continue to be difficult, and speculative appetite (i.e. dispensable cash) will not return to the 2008 level with growing unemployment.

Look for 700 as bottom and 1,250 as peak for 2009. Bargains abound today so you can be very selective. Avoid gigantic low grade deposits with big promises and big CapEx . Buy companies that are debt free, cash - rich with confirmed economic deposits, and preferably already producing or developing with secured financing."

Our call here has been mostly correct. I am mildly surprised by the relative strong performance of the junior resource sector in Q1 (up 35%). While I don't see much downside as value plays abound, note there is strong resistance at 1,000. I am cautious of the index and recommend taking profits and rotate to other beat-up companies that haven't enjoyed the run up.

Global Equities (using Shanghai Stock Exchange Index as Proxy):

I wrote in January that

"Asia is minimally involved in the subprime crisis and Asian consumers have collectively better balance sheets than American counterparts.

In Asia, 2009 will mark a major shift of focus from US exports to developing domestic consumption. Despite good fundamentals, I am not wildly bullish on Asian markets just yet. However a decent rebound of 20-25% from currently depressed level is achievable in 2009."

Shanghai rebounded 25% alone in Q1, faster that I anticipated. The index has de-coupled from the US equity markets and the chart is very bullish. I would raise my target for the index to 3,000 for the year. Buoyant Asian equities will have a positive impact on commodity prices.

Conclusion:

In this quarter, we saw the classic battle between inflationary and deflationary forces.

Debtors such as AIG, GE, and Russian metals producers are hurried to unload assets while savers of $trillions fear the dollar dilution and are looking for assets to preserve wealth.

We mentioned that in Q4 2008, the housing implosion bankrupted US banks and caused temporary hard squeeze on the dollar. In Q1 we likely saw the peak of the dollar. Mr. Bernanke and Mr. Obama continued with hyper-inflationary fiscal and monetary policies which will sparkle the resumption of commodity bull.

Asian markets are breaking away from US equities, this is what we anticipated. February car sales in China rose 25% from a year ago, signaling strong underlying pent-up demand. I look to accelerated global recovery and volatile markets, with positive uptrend ahead.