"...Additional resources from agreed sales of IMF gold will be used, together with surplus income..."

APRIL FOOL'S CAME a day late to the gold market this week.

"The biggest interest-rate cuts in history...An unprecedented fiscal expansion, injecting by next year $5 trillion into the world economy...expansionary policies as long as they are needed..."

So said Gordon Brown, summarizing the G20 summit of world leaders at its conclusion on Thursday.

On top of what's already been promised, the UK prime minister then announced "Additional resources of $1 trillion through the International Monetary Fund and other institutions [plus] $250 billion from Special Drawing Rights [the IMF bank reserve currency] issued to member countries...trebling the resources of the IMF with up to an additional $500 billion" on top.

What's more, Mr.Brown's and the other top 19 world leader have agreed "not 100 billion but $250 billion of trade finance...provided over the next 2 years through export credit agencies, including $50bn through the new World Bank initiatives..."

In short, "More money than ever before," as the prime minister put it.

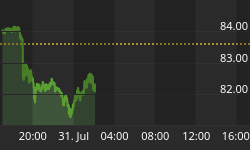

Meantime, however, the Gold Price dropped $30 an ounce, dipping below $900 for only the fourth time since February.

Why? "A Reuters story released just after noon UK time highlights considerable short-term risk to the gold market" gasped UBS in an email at lunchtime.

"We had expected any conversations and statements about gold at the G20 to be limited to the proposed sale of 403.3 tonnes of gold," went on John Reade, the Swiss bank's highly respected metals analyst in London.

"But a statement from the UK Treasury Minister and [a] G20 source suggests that more than this amount may be sold to support the IMF.

"This is potentially really bad news for gold market sentiment in the near term."

Those 400-odd tonnes, already proposed for sale by the International Monetary Fund (IMF) since February 2008, had look too small by half to several African delegates ahead of the G20 summit.

Gordon Brown himself has been agitating for IMF gold sales for the last 10 years, ever since he himself ordered the Bank of England to sell half the UK's national reserves at rock-bottom prices. (The Gold Price rose 17% as those sales then took place; when the IMF Sold Gold at the end of the 1970s, "dumping" 1,600 tonnes onto the market, the price rose eight-fold regardless...)

But anyone looking for G20 fresh action - rather than just a re-hash of existing commitments - only got it in money inflation, not in proposed gold sales by the IMF.

Citing only "agreed sales of gold" - and then confirming in questions-and-answers that the pre-proposed 403 tonne sale will be the limit - "Gold of the world is now being used to help the poor of the world," said Brown.

Here's hoping the poor take their chance to squirrel away a little more of that metal on Brown's latest gold-selling success. Because with all that money headed their way - barely 9 months after crude oil hit $150 per barrel and global inflation reached 30-year highs - they might just need all the help they can get.