Summary of Index Daily Closings for Week Ending Apr 2, 2004

| Date | DJIA | Transports | S&P | NASDAQ | Jun 30 Yr Treas Bonds |

| Mar 29 | 10329.63 | 2885.91 | 1122.46 | 1992.47 | 113^17 |

| Mar 30 | 10381.70 | 2883.64 | 1127.00 | 2000.63 | 113^12 |

| Mar 31 | 10357.70 | 2895.43 | 1126.21 | 1994.22 | 114^02 |

| Apr 1 | 10373.38 | 2918.64 | 1132.17 | 2015.00 | 113^15 |

| Apr 2 | 10470.59 | 2966.66 | 1141.80 | 2057.17 | 110^30 |

| SHORT TERM FORECAST (Next Two Weeks) | ||||

| TREND | PROBABILITY | Legend | ||

| Substantial Rise | Low | |||

| Market Rise | Medium | Very High | 80% | |

| Sideways | Medium | High | 60% | |

| Market Decline | Medium | Medium | 40% | |

| Substantial Decline | Medium | Low | 20% | |

| Very Low Under | 20% | |||

| INTERMEDIATE TERM FORECAST (Next 12 Weeks) | ||||

| TREND | PROBABILITY | Substantial | 800 points+ (DJIA) | |

| Substantial Rise | Low | Market Move | 200 to 800 points (DJIA) | |

| Market Rise | Medium | Sideways | Up or Down 200 (DJIA) | |

| Sideways | Medium | |||

| Market Decline | High | |||

| Substantial Decline | Very High | |||

This week the Dow Jones Industrial Average rose 257.62 points to close the week at 10,470.59, as forecast by last week's Short-term Technical Indicator Index reading of positive 73.00. The Shortterm TII has been accurate all but two weeks in 2004, and the two weeks it was off, it was accurate within its two week horizon. The rally was the expected bounce we've been calling for when we laid out the probability that the decline that took the Dow Industrials down to about 10,000 on March 24th, "would be followed by a rally back up to the 50 day moving averages."

We expect this rally to fizzle around the 50 day MA, or maybe a hair above it, and do not expect new highs to be reached. In the DJIA, the 10,753 intraday high on February 19th and the closing high of 10,737 on February 11th, 2004 should hold. If they don't, it will be due to the massive liquidity pumping we have been witnessing since the first of the year. That kind of M-3 growth has to go somewhere, and to the delight of the Master Planners, like water that finds a crack, massive fiat currency creation finds equities - for a while.

| Equities Markets Technical Indicator Index (TII) ™ | ||||

| Week Ended | Short Term Index | Intermediate Term Index | ||

| Nov 21, 2003 | 0.38 | (51.90) | Scale | |

| Dec 5, 2003 | (31.75) | (55.18) | ||

| Dec 12, 2003 | (5.83) | (54.43) | (100) to +100 | |

| Dec 19, 2003 | (6.50) | (47.03) | ||

| Jan 2, 2004 | (48.17) | (40.33) | Negative (Bearish) | |

| Jan 9, 2004 | (96.50) | (39.28) | Positive (Bullish) | |

| Jan 16, 2004 | (20.00) | (40.65) | ||

| Jan 23, 2004 | (8.13) | (32.15) | ||

| Jan 30, 2004 | 2.81 | (25.98) | ||

| Feb 6, 2004 | 11.75 | (20.19) | ||

| Feb 13, 2004 | (68.25) | (22.19) | ||

| Feb 20, 2004 | (30.00) | (22.36) | ||

| Feb 27, 2004 | (31.00) | (20.17) | ||

| Mar 5, 2004 | 16.00 | (17.17) | ||

| Mar 12, 2004 | ( 9.00) | (14.70) | ||

| Mar 19, 2004 | (12.00) | (27.60) | ||

| Mar 26, 2004 | 73.00 | (38.35) | ||

| Apr 2, 2004 | (3.00) | (35.61) | ||

This week the Short-term Technical Indicator Index comes in at negative 3.00, meaning we can expect the equity market to move net sideways next week. The move could be down-up or up-down, but is not likely to be impulsive. This indicator is a useful predictor of equity market moves over the next two weeks, both as to direction and to a lesser extent strength of move. For example, readings near zero indicate narrow sideways moves are probable. Readings closer to +/-100 indicate with a higher degree of confidence that an impulsive move up or down is likely over the short run.

The Intermediate-term Technical Indicator Index is useful for monitoring what's over the horizon - over the next twelve weeks. It serves as an early warning system for unforeseen trend changes of considerable magnitude. This week the Intermediate-term TII comes in at negative (35.61), warning that a significant reversal remains at risk over the next three months. It will take massive increases in M-3 to mitigate the damage or the timing, which may be occurring and could be successful.

We remain under a Dow Theory "sell signal," and triple tops and head and shoulders patterns are evident in several equity indices. The next two charts show that both the Dow Industrials and the Dow Transports are following the exact price patterns that led to previous significant declines during the past three years. In the case of the Industrials, the pattern has been that the index drops below its 50 day moving average and moves as far down as the 200 day moving average. It stops there, finding support, and reverses, bouncing back to try and bust up through the 50 day MA. But it fails to bust through, finding the 50 day MA's resistance too strong, then in a panic plummets a thousand or more points in a matter of a few weeks. This repeating pattern occurred four times between March 2001 and March 2003. The current price action is mirroring these patterns, with prices reaching their 50 Day MAs. If they fail to break higher, look for panic selling and a thousand point plus decline over the next two months. Friday's price action took the DJIA to its 50 day MA, but on the incredible jobs news, if news really moves markets, it probably should have risen higher.

In the case of the Transports, it's the same pattern, first with a break down below the 50 day MA, hitting and stopping at its 200 day MA, then bouncing merrily back only to smack its head against the 50 day MA like a cement ceiling. Friday's close left it marginally above its 50 day MA.

There is also a Bearish Head and Shoulders pattern that has fully completed in the Trannies, just as one had immediately prior to the last panic decline in 2002. In both cases, the right shoulder is thickening as prices hang on as long as possible between a declining 50 day MA and the 200 day MA. In 2002 the panic decline finally broke through the neckline of the pattern about the time the 50 day MA was about to cross below the 200 day MA. That convergence should occur this time in about two weeks. It is interesting to listen to all the perma-bull chatter about how this rally back from the 200 day MA is the end of the decline, that the decline to the 200 day MA was just a "normal correction" in an ongoing Bull market. Unless the rally breaks decisively above the 50 day MA, I'd strap on a parachute and be ready to eject. That's what history has repeatedly shown we should do.

Volume on rallies this week was average, not great, in the NYSE, and breadth on rally days, especially Friday, was uninspiring. So even if the indices retrace 78.6 percent of the move down to March 24th's lows, a strong move down from the retrace top has not been precluded.

The next chart is reprinted from last week's newsletter for comparison with a second Fibonacci chart on page five.

Last week's newsletter identified a nearly perfect .618 to .382 ratio between every single top or bottom and another top or bottom mate since the grand cycle top on January 14, 2004 using closing prices and trading days. Since this golden ratio has been consistent so far during this Bear market in the DJIA, it is logical to extrapolate this phi ratio into the future in order to determine high probability bifurcation points. Starting with the next determinant date in need of a phi mate, October 9th, 2002's low, if we count the number of trading days this date is from 1/14/2000 we come up with 687 days. 687 is .618 of 1111 total trading days. If we count 1111 trading days from 1/14/2000 we come up with June 15th, 2004 as the next significant top or bottom in the DJIA. We can't be sure at this time if it will be a top or bottom, but that should become apparent as we proceed into the spring. No guarantees, but so far this analysis has held with astonishing accuracy since 1/14/00, so why shouldn't we expect it to work as this Bear market continues?

After that, the next subsequent high/low that would need a phi ratio mate would be the 11/27/02 top. That date is 722 trading days from 1/14/00 and is .618 of 1168 trading days, getting us to a projected turn date of September 2, 2004. December 27th, 2002's low would have a phi mate of October 19th, 2004 and January 14th, 2003's top would have a phi mate of November 12th, 2004. The first turn date in 2005 looks like it will be the anniversary of this year's top, minus one trading day, February 10th, 2005, the phi mate of the 3/11/2003 bottom. My guess is these dates will be accurate +/- a week or so. It should be great fun watching this astonishing Fibonacci pattern unfold during the year.

The XAU is an index of 9 common stocks of companies involved in the gold and silver mining industry. The above chart explores the correlation of DJIA price movements with those of the XAU. There are two key empirical conclusions that can be drawn from this chart. On a short-term trend basis, there appears to be direct, contemporaneous correlation between the two indices, with a slight lag in the XAU. That is, the DJIA appears to make directional trend changes within a month or so before the XAU follows. This was part of my point in last week's newsletter. Should the DJIA take a dive over the next several months, I would expect the XAU to initially decline with it.

However, the unique dual nature of the XAU is also evident in the above chart. The XAU is much more than a basket of common stocks, it also represents a measure of commodities - gold and silver metals. While the chart shows XAU short-term correlation with the DJIA, it also shows that the XAU is up 76.7 percent since March 1999 while the Dow Industrials are up only about 5 percent. This is the metals' component bullish valuation coming through in the long run price measurement. So, should the DJIA decline and the XAU initially get caught in the downdraft, I look for an eventual -- maybe even early - reversal in the XAU and further long-term gains. What could help the gold and silver stocks even more is if a major currency, somewhere out there, decides to back its fiat paper with gold - a real possibility should (as) world economies collapse.

The point is the gold and silver stocks are not the metals, and will be subject to volatility from general equity market gyrations, but eventually should benefit as precious metals rise in value. After all, there is only so much gold and silver - and to increase supply it must be mined.

The Economy:

A mixed bag this week. The International Council of Shopping Centers and UBS reported this week that U.S. Chain Store Sales decreased 1.9 percent for the week ended March 27th. They blamed high gasoline prices. Yes, gas and oil prices are becoming a problem. OPEC, the Organization of Petroleum Exporting Countries, is cutting back oil production. This is coming on the heels of historically high crude prices that are now at risk of going even higher. High oil prices is a cost-push inflation generator, and is in effect a consumption tax. But when you create massive fiat dollars from thin air, you'll have this. Printing money might get you a rising equity market as stocks are priced like a commodity rather than as a function of discounted earnings - an election year Master Planner objective - but you get earnings-destroying cost-push inflation too. Any way you cut it, overproduction of fiat currencies eventually leads to economic slowdown, and increasing deflation risks.

Manufacturing activity figures disappointed this week. The National Association of Purchasing Management-Chicago reported that its Index of Manufacturing declined from 63.6 to 57.6. Readings below 50 indicate contraction. It was the inflationary component in the index that kept it from slipping further, the "prices paid" ingredient. New orders and production components fell sharply. The Commerce Department reported that U.S. Factory Orders rose only 0.3 percent in February on the heels of a revised 0.9 percent decline in January. But if you exclude the transportation orders, Factory Orders actually fell in February by 1.2 percent. A March measure from the Institute for Supply Management (ISM) reported that its index rose slightly from 61.4 in February to 62.5 in March. On the inflation/deflation front, the Producer Price Index rose a miniscule 0.1 percent in February, according to the Labor Department. Core PPI, excluding food and energy, was also reported to have risen only 0.1 percent. If the numbers are right, deflation isn't that far away. If.

The Labor Department got the headlines they were after on Thursday when they reported that Jobless Claims were 342,000 for the week ended March 27th. Of course they revised last week's figure up to 345,000. Yet each week the press reports that Jobless Claims are down. They are not down. At best you can say they essentially remain about the same as they have for several weeks now - which is too high for a so-called recovery.

Friday the Labor Department announced that non-farm payrolls rose 308,000. Out of nowhere, after anemic jobs growth reports month after month, bang! we go from 21,000 in February to 308,000 in March. Hmmm. Oh, and the Labor Department revised February's figure, more than doubled it to 46,000. Hmmm. So sorry. Small mistake. Oh, and while all of a sudden out of nowhere all these U.S. jobs were created, the Labor Department tells us the average number of hours worked per week declined, and that the leading jobs indicator, temporary help payrolls, fell, and the unemployment rate went up as 179,000 more good folks were counted as looking for work but couldn't find any. Hmmm. Average weekly earnings are down. Twenty-four percent of jobless workers have been unemployed for more than 27 weeks - a 20 year high. Hmmm. Since March 2001, the U.S. has lost 2.3 million jobs according to the National Bureau of Economic Research, the longest period of time without net new job growth since the Labor Department tracked this. Now maybe I just fell off the turnip truck but, ah, 308,000 new jobs in March alone? The same day, Gateway announced it's cutting 2,500 jobs and Sun Microsystems announced 3,300 fresh pink slips.

The last time we saw this many jobs created in one month in the U.S. was in April 2000, the very beginning of the 80 percent crash in the NASDAQ, the 50 percent crash in the S&P 500, and the 40 percent pummeling the DJIA took. It marked the beginning of the last - and perhaps continuing - recession. So assuming the jobs number is remotely accurate, it doesn't necessarily correlate to good times. No matter how you feel about the accuracy of this number, ya gotta hand it to Labor, they're doing their yeoman's part to get Dubya reelected. Or are they? Folks, hear it here first. This number just may have gotten John Kerry elected in November. I'll explain why in the Bonds section.

Is it any surprise that according to the Conference Board, a business research group based in New York, its Index of Consumer Confidence fell in March to its lowest reading since October 2003, down to 88.3?

Big changes coming at the Dow Industrials. Outta here (to borrow a phrase from my favorite baseball broadcaster Harry Kalas) are AT&T, Eastman Kodak Co. and International Paper Co. In are Verizon Communications Inc., American International Group, Inc. and Pfizer. This decision comes courtesy of The Wall Street Journal and commences April 8th, 2004. They will adjust the weightings so that there is no change to the index's valuation at the opening on that day. The DJIA picks up an insurer and a drugmaker and loses a film producer and forest products company.

Money Supply, the Dollar, & Gold:

M-3 was up again for the latest week reported by the Federal Reserve, up $10.2 billion for the week of March 22nd. This represents an increase of a whopping $177.9 billion since the first of the year, an annualized growth rate of 8.74 percent. Extraordinary when you consider this same Fed is keeping interest rates at 46 year lows, targeting 1.0% in Fed Funds and jawboning long rates down pretty much every day in spite of reported GDP growth over 4.0 percent and a cacophony of good news messages, "the jobs are coming, the jobs are coming." Well, something isn't making much sense. There must be real concern about deflation's threat inside the sacrosanct halls of the temple. That something, I believe, is the ominous technical picture for equities, the deflationary force a major stock market decline could become, and the imperative that stocks stay up uP UP in an election year. One thing that has been clear, massive printing of money can sustain stocks, delay declines, and trump technicals. The Master Planners know this and are playing their ace - liquidity pumping. It hasn't stopped. I'd feel a whole lot better if M-3 growth was around 2 to 3 percent. That seems a reasonable level. If it continues, at some point, hyperinflationary money growth will lead to a decline in the dollar and bonds which will lead to a major decline in equities which will lead to deflation. Happened once before - Germany in the early 20th century.

Take your pick of scenarios for Gold, the metal. If inflation, then gold rises as a commodity. If deflation, then a paradigm shift occurs where gold is perceived as money, and thus rises. Any way you cut it, the long run picture for gold - the metal - looks Bullish. Gold stocks should rise along with any rally in the general equity market. Should equities decline sharply and gold - the metal - be perceived as having intrinsic monetary value, gold stocks should do an about face, digress from a general decline in equities, turn up and follow the metals. Over the long run, gold stocks are in a Bull market.

Bonds and Interest Rates:

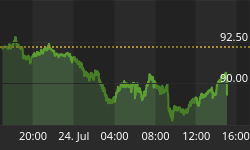

The chart below (courtesy of www.stockcharts.com) shows that the 30 Year U.S. Treasury Bond over the past two years may be forming a massive Bearish Head & Shoulders pattern. If so, it is one ominous looking creature. The distance from the Head to the Neckline is about 18 points - meaning the minimum downside price target would be around 82 should the right shoulder's formation complete. We would have to see prices decline about 11 points from current levels for pattern confirmation, so this is more of a possibility than a probability at this time. Still, it is worth mentioning now given the near-perfect formation taking place, along with several fundamental Bearish developments for bonds that may be under way.

We learned this week that a difference of opinion is growing inside the Federal Reserve as to whether interest rates should be allowed to float higher or not. CNNMoney.com quoted both the Atlanta and St. Louis Federal Reserve Bank Presidents, warning that interest rates should not be kept low for too long. Plus we are hearing rumors that the Japanese Central Bank may no longer buy the U.S. Dollar by the cargo plane load. Japan has been taking these dollars and turning around and buying our U.S. Treasuries with them. Their goal has been to keep the yen competitively devalued against the dollar - thereby making Japanese products cheaper overseas, stimulating their economy. This has allowed the Fed to print as much money as they wanted because they knew there was a ready buyer supporting its price. Should Japan stop buying dollars, and stop buying our bonds, and should the Fed decide it is soon a good time for interest rates to rise, well, simply, bonds could sink. How soon we don't know, but the risks of holding bonds has increased.

It Looks Like A Massive Bearish Head & Shoulders Is Developing in the 30 Year Treasury Bond

The risk of holding bonds has especially increased now that the Labor Department adjusted, revised, re-adjusted, re-figured, and seasonally-adjusted (thank you Richard Russell for the right adjectives to describe this counting process, www.dowtheoryletters.com) the March non-farm payroll numbers to a whopper of a 308,000 figure. Bonds tanked on this figure - an unintended consequence I'm sure. And they will continue to tank. Why? Well if the economy is truly on fire as most government statistics proclaim, if money supply is truly at banana republic breakneck pace, if the last bastion of concern about economic slowdown - jobs - is now a myth, then interest rates at 46 year lows simply are not justified.

The Labor Department has now painted the Federal Reserve into a corner. No more excuses to keep short-term rates at 1 percent. Reason gone. The Fed has two choices: first, either raise rates, or second, announce that the government's robust economic figures are phony and deflation is really knocking at the door, so they must keep rates low. Or, I suppose there is a third option. Announce to the world they don't give a hoot about monetary stability, don't give a hoot about deflation or inflation, that all they care about is getting the boss reelected so to damnation with everything, interest rates are staying low until Dubya cleans Kerry's clock in the autumn. My best guess? We can look forward to rising interest rates. Get ready, the party is over. The Master Planners can't be too happy with this number, or won't be once they put some thought behind it. It's too high. They would have been better off stopping the counting process at "re-adjusted" and announcing 140,000 or so new jobs.

The Bottom Line:

All roads lead to deflation. Whether we travel there now or follow the scenic route of hyperinflation that leads to a dollar collapse that leads to a bond collapse that leads to a stock market collapse that leads to economic collapse that leads to deflation, we cannot be sure. The actions of the Federal Reserve clearly show they prefer winding lanes and trees and streams, anything to postpone the inevitable. Sadly, the longer that correction is delayed, the worse it will be. Deflation will hurt more from loftier price levels than from here because with liquidity-driven bubble expansion comes everburgeoning debt loads, because M-3 growth - liquidity - is a function of lending/borrowing.

The equity market is technically poised to continue its downward trek once prices reach back up and kiss their 50 day moving averages, then turn and drop. Should prices break decisively higher above their 50 day moving averages, then chalk this latest decline up as another aborted attempt by the Bear, an M-3 honey trap set by the Master Planners that locks the Bear up for a while longer. Should that occur, we'll take another look at the developing patterns to determine how high markets could go before the final top is in. I remain confident the 50 day MA resistance levels will hold, but one cannot ignore the massive quantities of money the Fed is flooding the markets with at this time, and it's possible short to intermediate-term Bullish result. Caution is wise.

"And when they had carried out all that was written concerning Him,

they took Him down from the cross and laid Him in a tomb.

But God raised Him from the dead;

God has fulfilled this promise to our children in that

He has raised up Jesus, as it is written in the second Psalm . . ."

Acts 13: 29, 30, 33

| Key Economic Statistics | ||||||||

| Date | VIX | Mar. U.S. $ | Euro | CRB | Gold | Silver | Crude Oil | 1 Week Avg. M-3 |

| 10/31/03 | 16.00 | 92.98 | 115.57 | 247.00 | 384.6 | 5.06 | 29.11 | 8876.5 b |

| 11/07/03 | 16.84 | 93.20 | 115.11 | 249.75 | 383.4 | 5.05 | 30.85 | 8876.8 b |

| 11/14/03 | 17.33 | 91.58 | 117.60 | 256.25 | 398.0 | 5.41 | 32.37 | 8860.6 b |

| 11/21/03 | 18.98 | 90.72 | 119.09 | 250.50 | 396.0 | 5.29 | 31.61 | 8851.4 b |

| 11/28/03 | 16.32 | 90.28 | 119.65 | 253.25 | 398.0 | 5.39 | 29.96 | 8850.0 b |

| 12/05/03 | 17.23 | 89.17 | 121.60 | 256.00 | 407.3 | 5.49 | 30.73 | 8807.8 b |

| 12/12/03 | 16.46 | 88.44 | 122.74 | 261.75 | 410.1 | 5.64 | 33.04 | 8812.9 b |

| 12/19/03 | 15.71 | 88.53 | 123.58 | 259.50 | 409.9 | 5.72 | 33.02 | 8807.2 b |

| 1/02/04 | 18.30 | 86.93 | 125.76 | 256.75 | 416.1 | 5.96 | 32.52 | 8819.8 b |

| 1/09/04 | 16.79 | 85.40 | 128.19 | 266.50 | 426.8 | 6.49 | 34.31 | 8828.5 b |

| 1/16/04 | 14.98 | 88.05 | 123.57 | 265.50 | 407.0 | 6.33 | 34.00 | 8849.5 b |

| 1/23/04 | 14.88 | 88.81 | 125.81 | 266.50 | 408.0 | 6.36 | 34.94 | 8864.5 b |

| 1/30/04 | 16.46 | 87.48 | 124.42 | 262.10 | 402.9 | 6.25 | 33.05 | 8895.3 b |

| 2/06/04 | 16.00 | 86.15 | 126.83 | 260.50 | 403.6 | 6.27 | 32.43 | 8884.9 b |

| 2/13/04 | 15.62 | 85.68 | 127.25 | 264.85 | 410.8 | 6.58 | 34.56 | 8895.5 b |

| 2/20/04 | 16.05 | 87.40 | 126.96 | 264.50 | 397.5 | 6.53 | 34.25 | 8932.2 b |

| 2/27/04 | 14.53 | 87.89 | 124.52 | 273.90 | 396.8 | 6.71 | 36.16 | 8946.6 b |

| 3/05/04 | 14.52 | 88.75 | 123.28 | 274.00 | 401.6 | 6.99 | 37.26 | 8956.3 b |

| 3/12/04 | 18.21 | 89.60 | 121.80 | 272.00 | 395.6 | 7.06 | 36.19 | 8946.7 b |

| 3/19/04 | 19.15 | 88.56 | 122.47 | 280.20 | 412.7 | 7.56 | 37.62 | 8987.2 b |

| 3/26/04 | 17.12 | 89.30 | 120.90 | 278.25 | 422.3 | 7.71 | 35.73 | 8997.6b |

| 4/02/04 | 15.81 | 88.80 | 121.12 | 280.00 | 421.1 | 8.15 | 34.39 | - |

Note: CRB near its high, new high for silver.

The Passion of The Christ is now playing in your local theater

Go to www.thepassionofthechrist.com for more information.