Credit has to be given to Mr. Greenspan. By bailing out the S&L Associations in 1990 he contributed to the creation of the emerging market bubble of 1994, which led to the Mexican crisis. Then, by bailing out Mexico - with the then acting Treasury Secretary Robert Rubin's help - he contributed to the emerging market debt excesses that led to the Russian crisis and the LTCM debacle of 1998. Again he bailed out the system with an enormous liquidity injection and created in the process financial history's biggest bubble - the NASDAQ bubble of 1999/2000. But until then, Mr. Greenspan was only a "serial" bubble blower. He managed to create bubbles, but only one at the time and in different asset classes, at different times and in different parts of the world. But this time around, we have to give him far more credit for his monetary achievements and nominate him for a Nobel Price in bubble creation. After all, he is the first central banker in the history of capitalism who has managed to not only create a credit bubble in the US, which has led to the entire mortgage refinancing scheme, excessive household borrowings, over-consumption, and a growing current account deficit, but he has also miraculously managed to create bubbles all over the world - in stocks and bonds of emerging economies, the currencies of Australia, New Zealand and South Africa, in housing, and lastly in Chinese capital spending, which is now growing by more than 40% per annum, as well as in commodity prices (see figure below).

In addition, as a result of the growing US current account deficit, which is offset by current account surpluses in Asia, he has managed to create a bubble in foreign exchange reserves of Asian central banks. As can be seen from the figure below, Japanese foreign exchange reserves have exploded on the upside since year 2000, whereby the same situation of soaring foreign exchange reserve growth can be found in China as well as in most other Asian countries.

So, what terrorists are to peace loving citizens - we must exclude from these Mr. Bush & Co - Mr. Greenspan is to sound money, which is not supposed to lose its purchasing power. In short, he is for the honest saver, who depends on the purchasing power of his money to be maintained for his retirement or for his children' sake, the world's most dangerous man!

In the meantime, US industrial production is hardly growing, as can be seen from the continuous decline in commercial and industrial loans (see figure below courtesy of Bridgewater Associates).

So, all Mr. Greenspan has created is a huge financial and asset bubble everywhere in the world, but no real improvement in the US economy, which is like a drug addict and requires more and more credit to stay afloat. As someone once said, in order to avoid a hangover, you must keep on drinking...

The problem, however, is that the US requires an increasing amount of credit growth in order to keep real estate and stock prices up and to make them move higher, which in turn supports the US consumer's excessive consumption. But, at the same time, while asset prices in the US are soaring, output is not rising for the simple reason that the market has discounted this "evil" Fed induced con game.

We all know from basic economics that the only way in which monetary policy can really affect output is if it comes as a surprise - and this only in the short-term. If, however, everybody knows that monetary policy will be easy, everybody will move prices instead of output, and the monetary expansion will be "neutral" at best. But what is now suddenly happening is that the investment community, through the market mechanism, is beginning to catch on to the fact that there is much more credit growth out there than productive capacity, and therefore prices have risen in some cases, such as for commodities, very rapidly.

It would seem to me that the realization by the investment community that Greenspan's game cannot end well has begun to reverse expectations. Suddenly, out of the blue, the bond market has collapsed and brought down stock and commodity prices along with it.

As I have maintained before, this is not a time to play hero like the brain-damaged president of the US in Iraq. It is a time to stay of out of all assets and be patiently waiting for better buying opportunities. In particular, I am concerned about the US housing market.

In some areas of the US, housing prices have been rising at almost 30% per annum in recent years and overall prices have doubled since 1997. The question, therefore, arises when this housing boom, which was fueled by ultra low interest rates and allowed people to refinance their homes, will come to an end. This is an important question because US consumption since year 2000 was not driven by capital spending and employment gains, but purely by asset inflation in the housing market, which allowed people to take out larger and larger mortgages and spend the additional funds (well understood, "borrowed funds") on consumer durables such as cars and consumer non-durables. Now, however, there is a problem with the housing market. If the US economy continues to strengthen, interest rates, which are negative in real terms, will have to rise considerably and this could lead - if not to a housing crash - so at least to a less buoyant market. In addition, as we can see from the figure below (courtesy of Bridgewater), the inventories of unsold homes are at a record. Therefore, should higher interest rates, driven by a stronger economy, lead to less home purchases by individuals, home-builders who are holding these inventories could get hurt quite badly.

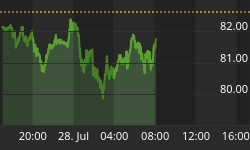

I would, therefore, recommend to all investors who believe that the US economy is expanding solidly to sell all homebuilding companies' stocks here or on any rebound. Personally, however, I am not so sure about the strength of the US economy, since consumption is purely driven by additional borrowings and government spending, which leads to larger and larger budget deficits. In fact, I have just bought some US treasury bonds with the view that, in the next few weeks, investors' expectations about future growth could be somewhat disappointed. After all, every asset-inflation, which drove consumption in the past, such as was the case in Japan in the late 1980s and in Hong Kong prior to 1997, came to a bitter end. Thus, with bond prices being near-term oversold, any disappointment about economic growth could lead to a modest or even strong rebound in bond prices. If you look at the figure below, which shows the recent performance of 10 years US Treasury bonds, it would appear that there is some support around this level and that a modest rebound is probable.

Still, this short term rebound aside, bonds may shortly be completing a longer-term head-and-shoulders top, which would mean that in future we could see lower bond prices or much higher interest rates. Such an outcome could spoil all other asset inflation parties and lead to lower home, commodity and stock prices.... Therefore, once again, patience and staying aside from the markets may be the best option.