Asha Bangalore (Northern Trust): Rebound in inventory accumulation in store for 2010?

"Total business inventories held steady in January. Factory inventories increased 0.2% in January, while wholesale and retail inventories dropped 0.2% and 0.1%, respectively. Total business sales advanced 0.6% during January, after a 1.00% increase in the prior month.

"The inventory-sales ratio of the business sector was down one notch to 1.25 in January; the record low for this ratio is 1.24 set in 2005. As the economy gathers momentum, inventories are projected to make a sizable contribution to real GDP, which could be in the first-half of 2010 or later in the year. The timing is unclear but it is nearly certain that an inventory accumulation led spike in real GDP is in store for 2010."

Source: Asha Bangalore, Northern Trust - Daily Global Commentary, March 12, 2010.

Asha Bangalore (Northern Trust): Total continuing claims holding at elevated level

"Initial jobless claims fell 6,000 to 462,000 during the week ended March 6. The four-week moving average of initial jobless claims is up nearly 8,000 from a low of 469,000 in February. Continuing jobless claims rose 37,000 to 4.558 million and the insured unemployment rate held steady at 3.5%.

"Total continuing jobless claims, inclusive of those under special programs, edged down slightly to 10.2 million during the week ended February 20; these claims have held at over 10 million for eleven consecutive weeks. A meaningful decline of these claims should signal that labor market conditions are indeed improving."

Source: Asha Bangalore, Northern Trust - Daily Global Commentary, March 11, 2010.

Asha Bangalore (Northern Trust): Strength of February retail sales impressive

"Retail sales increased 0.3% in February, after a downwardly revised 0.1% increase in January (previously reported as a 0.5% increase) and a 0.2% drop in December (prior estimate was 0.1% decline). Excluding gasoline and autos, retail sales advanced 0.9% in February reflecting gains in sales of furniture (+0.7%), apparel (+0.6%), electronics and appliances (+3.7%), sporting goods (+1.2%), and general merchandise (+1.0%).

"However, the January-February data of retail sales show a smaller increase in retail sales compared with the fourth quarter tally. Unless consumer outlays on services and March retail sales are significantly strong, the gain in consumer spending during the first quarter is most likely to be smaller than the fourth quarter's annualized increase of 1.7%."

Source: Asha Bangalore, Northern Trust - Daily Global Commentary, March 12, 2010.

MoneyNews: Obama may pay homeowners to sell at loss

"The Obama administration, which has been trying to keep defaulting owners in their homes, reportedly will start paying some of them to leave under a new program that would let owners sell for less than they owe and will give them a little cash to boot.

"The new program implemented by President Barack Obama reportedly will allow homeowners to make short sales and receive a payment from the government to do so. A short sale occurs when someone sells his or her house for less than the value of the mortgage.

"With five million households behind on their mortgages, the Obama administration faces loud cries for more assistance. Its $75 billion mortgage modification plan hasn't helped many homeowners.

"The new program, which takes effect April 5, makes mortgage lenders accept the short sales, which means they won't be paid back the full amount of their loans, The New York Times reports.

"To entice all parties to participate, servicing banks will receive $1,000 for the first mortgage and another $1,000 for the second if there is one. That's the same payment as in the mortgage modification plan.

"The new angle is $1,500 in relocation assistance' for the homeowner.

"We want to streamline and standardize the short sale process to make it much easier on the borrower and much easier on the lender,' said Seth Wheeler, a Treasury senior adviser.

"But lenders emphasize that participating homeowners won't have it easy.

"This is not an opportunity for the customer to just walk away,' J. K. Huey of Wells Fargo told The Times.

"If someone doesn't come to us saying, I've done everything I can, I used all my savings, I borrowed money and, by the way, I'm losing my job and moving to another city, and have all the documentation,' We're not going to do a short sale.'"

Source: Dan Weil, MoneyNews, March 9, 2010.

Bloomberg: Fannie, Freddie ask banks to eat soured mortgages

"Fannie Mae and Freddie Mac may force lenders including Bank of America Corp., JPMorgan Chase & Co., Wells Fargo & Co. and Citigroup Inc. to buy back $21 billion of home loans this year as part of a crackdown on faulty mortgages.

"That's the estimate of Oppenheimer & Co. analyst Chris Kotowski, who says US banks could suffer losses of $7 billion this year when those loans are returned and get marked down to their true value. Fannie Mae and Freddie Mac, both controlled by the US government, stuck the four biggest US banks with losses of about $5 billion on buybacks in 2009, according to company filings made in the past two weeks.

"The surge shows lenders are still paying the price for lax standards three years after mortgage markets collapsed under record defaults. Fannie Mae and Freddie Mac are looking for more faulty loans to return after suffering $202 billion of losses since 2007, and banks may have to go along, since the two US-owned firms now buy at least 70 percent of new mortgages.

"If you want to originate mortgages and keep that pipeline running, you have to deal with the push-backs,' said Paul Miller, an analyst at FBR Capital Markets in Arlington, Virginia, and former examiner for the Federal Reserve. It doesn't matter how much you hate Fannie and Freddie.'

"Freddie Mac forced lenders to buy back $4.1 billion of mortgages last year, almost triple the amount in 2008, according to a Feb. 26 filing. As of Dec. 31, Freddie Mac had another $4 billion outstanding loan-purchase demands that lenders hadn't met, according to the filing. Fannie Mae didn't disclose the amount of its loan-repurchase demands. Both firms were seized by the government in 2008 to stave off their collapse."

Source: Bradley Keoun, Bloomberg, March 5, 2010.

Financial Times: Big bank oversight to stay with Fed

"Banks with more than $100bn of assets will be overseen by the US Federal Reserve in a regulatory reform plan that represents a partial victory for the central bank after months of attacks in Congress.

"Chris Dodd, the Senate banking committee chairman, had proposed hiving off all bank supervision to a single regulator but is set to propose this week that the 23 largest institutions stay under the Fed's oversight, according to people familiar with the plans.

"At issue over the weekend was the regulation of several hundred state chartered institutions that also want to remain under the Fed's supervision.

"While attention has been focused on argument between Democrats and Republicans over the powers and location of new consumer protection functions, which may also be housed within the Fed, other elements of regulatory reform - deemed more important by many institutions and policymakers - are close to fruition.

"A new resolution' regime to deal with failing, but systemically important, institutions would allow the government to wind up a company quickly to avoid contagion spreading through the financial system.

"But in a concession to Republican fears about giving government too much power over business, a bankruptcy judge would provide checks and balances.

"The regime is designed to prevent a repeat of the costly bail-out of AIG or the damaging bankruptcy of Lehman Brothers.

"But Democrats have had to come up with a complex system that incorporates a role for the judiciary to meet Republican concerns, while also limiting the time and scope of a judge's intervention to prevent an unruly process that infects the entire financial system.

"The Fed's retention of authority over the biggest banks is partly a result of demands by Tim Geithner, Treasury secretary and former president of the New York Fed, who has told senators that only the central bank is qualified to oversee the core of the system."

Source: Tom Braithwaite, Financial Times, March 7, 2010.

The Wall Street Journal: Cracking down on swaps

"Following Greece's economic crisis, European leaders are considering banning credit-default swaps, WSJ Brussels bureau chief Stephen Fidler reports on the News Hub."

Source: The Wall Street Journal, March 10, 2010.

Financial Times: France and UK seek hedge fund deal

"Gordon Brown and Nicolas Sarkozy will on Friday try to hammer out a compromise deal over European Union reforms that the US and UK believe could damage the hedge fund and private equity industries.

"The British prime minister shares the concerns of Tim Geithner, US treasury secretary, that a draft EU directive to introduce tighter regulatory controls could impose new barriers to business.

"London believes that French cultural opposition to hedge funds lies behind the drive to clamp down on the operation of alternative investment funds'. British officials say Mr Brown will discuss the issue when he meets the French president in London on Friday, ahead of an EU summit this month.

"The debate over the shape of financial regulation and the EU directive has raised transatlantic tensions.

"Mr Geithner, in a letter to Michel Barnier, Europe's internal market commissioner, voiced concern about various proposals that would discriminate against US firms'.

"The US has stopped short of threatening retaliatory action. However, if the directive becomes law in its current form, Europe-based fund managers could face reprisals in the US Congress for what is being seen as an attempt to dictate the global regulatory landscape.

"Senior EU officials hit back on Thursday at the US criticism. A spokesman for Michel Barnier, the new EU internal market commissioner who is responsible for financial services regulation and to whom Mr Geithner addressed his concerns, said that the EU decision to act on hedge funds was in line with a G20 decision to reinforce transparency in the financial system.

"Britain, Europe's biggest centre for hedge funds, is leading opposition to aspects of the directive, which it fears could impede the operations of funds based in London."

Source: George Parker, Sam Jones, Nikki Tait and Tom Braithwaite, Financial Times, March 11, 2010.

Financial Times: Eurozone eyes IMF-style fund

"Germany and France are planning to launch a sweeping new initiative to reinforce economic co-operation and surveillance within the eurozone, including the establishment of a European Monetary Fund, according to senior government officials.

"Their intention is to set up the rules and tools to prevent any recurrence of instability in the eurozone stemming from the indebtedness of a single member state, such as Greece.

"The first details of the plan, including support for an EMF modelled on the International Monetary Fund, were revealed at the weekend by Wolfgang Schäuble, the German finance minister.

"I am in favour of stronger co-ordination of economic policies in the EU and in the eurozone,' Mr Schäuble told newspaper Welt am Sonntag.

"If France and Germany can agree on such proposals - long urged by Paris - they are likely to set the basis for the most radical overhaul of the rules underpinning the euro since the currency was launched in 1999.

"The German thinking emerged as George Papandreou, the Greek prime minister, flew to Paris to seek the support of Nicolas Sarkozy, French president, for his government's drastic austerity programme.

"We must support Greece, because they are making an effort,' Mr Sarkozy said before the meeting. If we created the euro, we cannot let a country fall that is in the eurozone. Otherwise there was no point in creating the euro.'

"His words appeared to underline the greater readiness in France than in Germany to provide some sort of financial support or guarantee for the Greek economy. Angela Merkel, the German chancellor, insisted that no such support had been sought or discussed when she met Mr Papandreou on Friday.

"Both France and Germany agree Greece should not turn to the IMF for support, so the idea of an EMF has clear attractions for Paris, though it could hardly be set up in time to help Greece."

Source: Quentin Peel and Scheherazade Daneshkhu, Financial Times, March 7, 2010.

John Authers (Financial Times): Credit market - no news is good news

"John Authers says that it is good news that the credit market is much less newsworthy than it used to be."

Click here for the article.

Source: John Authers, Financial Times, March 10, 2010.

David Fuller (Fullermoney): What about US Treasury bonds?

"I remain a long-term bear of US Treasuries. It seems self-evident that US 10-year Treasury yields will revert to more normal levels of 5% to 6%, sooner or later. In the event of serious inflationary problems resulting from spiralling debt and money printing, they could even soar to levels not seen since the early 1980s.

"However, I remain an agnostic on timing. Arguments for yields remaining low for an indefinite period are equally convincing and this uncertainty is reflected by the ranging price action. So I will continue to watch, perhaps being tempted if rangebound 10-year yields retest their lower boundary near 3.15% and hold, or when they eventually maintain a break above 4%.

"Meanwhile, the longer they remain rangebound near current levels, signalling neither a Japan-style deflationary slump or growing inflationary pressures, the better it will be for the global equity bull market."

Source: David Fuller, Fullermoney, March 9, 2010.

MoneyNews: China embraces US Treasuries, wary about buying more gold

"China, the world's biggest holder of foreign exchange reserves, renewed its commitment to the US Treasury market on Tuesday but said it would be wary of adding to its gold holdings.

"The country's chief currency regulator said China would attract more capital inflows this year, partly reflecting expectations of a stronger yuan, but he left the market none the wiser as to when Beijing might let the currency resume its rise.

"The US Treasury market is the world's largest government bond market. Our foreign exchange reserves are huge, so you can imagine that the US Treasury market is an important one to us,' Yi Gang, head of the State Administration of Foreign Exchange (SAFE), told a news conference.

"The exact composition of China's reserves, the world's largest, is a state secret and the subject of intense scrutiny by global investors aware that, with such large sums at stake, even marginal portfolio shifts have the potential to move markets.

"Speaking during the annual session of parliament, Yi expressed the hope that China's presence in the US Treasury market would not become a political football. China, he stressed, was not in the game of short-term currency speculation.

"It is market investment behavior, and I don't want it to be politicized,' he said. We are a responsible investor, and we can surely achieve a win-win result in the process of investing.'

"Yi dampened hopes of gold bugs that China might be itching to add to the 1,054 tons of the metal in its reserves.

"On a 30-year horizon gold was not a great investment, he said, and China would simply drive up prices if it piled into the market.

"It is, in fact, impossible for gold to become a major investment channel for China's foreign exchange reserves. I have 1,000 tons now, and even if I doubled that holding, according to current prices, that would be about $30 billion,' Yi said."

Source: MoneyNews, March 9, 2010.

The Wall Street Journal: Bull market turns one

"As the bull market notches its first year anniversary, the News Hub panel weighs in on whether investors can still make money and how the market will react when the interest rates inevitably adjust."

Source: The Wall Street Journal, March 9, 2010.

John Authers (Financial Times): Price of Nasdaq's crash

"In a week of anniversaries, it is 10 years since the Nasdaq Composite peaked, crashed and burned. The dotcom bubble seems to be from another world, a speculative aberration that is now over.

"But we are still living with its consequences.

"The dotcoms were a classic tale of speculative excess and overvaluation, to be compared with Japan in the 1980s or the US in the 1920s. As a chart shows, the fallout was identical.

"But the Federal Reserve took deliberate steps to avoid a repeat of the US in the 1930s or Japan in the 1990s. It slashed interest rates, helping ensure that the macroeconomic damage from the dotcom crash, in the form of a very brief and shallow recession, was remarkably light.

"The consequences of those steps have proved to be long lasting. The 1990s were driven by irrational exuberance' - huge and naively confident investments in the stock market by retail investors.

"The past decade was driven by leveraged investors. Those low interest rates made it far cheaper for investors such as hedge funds to magnify their returns with leverage. Thus they came to drive the market.

"They were helped by another artefact of the dotcom crash. Mutual funds (and the portfolios of the new breed of day traders) crashed with the Nasdaq. Hedge funds, able to sell short and to switch between asset classes, were able to make money during the years of the dotcom bust. That in turn attracted huge new flows from institutions, who are as prone to chase performance as anyone else.

"As a result, many of the technical and leverage-driven strategies used by hedge funds, and by banks' proprietary trading operations, became top-heavy. Far too much money was thrown at structured credit investments, or at emerging markets' currencies.

"We all now know the consequences. A decade on, they are the consequences of the Nasdaq boom."

Source: John Authers, Financial Times, March 9, 2010.

Bespoke: Bespoke's international snapshot

"Below we provide our trading range charts for 20 major country indices around the world. For each chart, the blue shading represents the index's normal trading range', which is between one standard deviation above and below the 50-day moving average (white line). The red shading represents between one and two standard deviations above the index's 50-day moving average, and vice versa for the green shading. In general, the red shading is an initial overbought level, and a move above the red zone is an extreme overbought reading that suggests a short-term pullback is in the cards.

"Only Sweden and Malaysia are currently trading above the red zone into extreme overbought territory. Canada, Brazil, the UK and Switzerland are trading within their red zones and are trending nicely higher, while the rest of the country indices are within their normal trading ranges. None of the countries are currently oversold, but some of them don't have attractive chart patterns. China, Hong Kong, Taiwan, South Korea and Spain are all struggling to stay above their 50-days at the moment and have a lot of work to do to return to long-term uptrends."

Source: Bespoke, March 11, 2010.

Bespoke: S&P 500 sector breadth

"The percentage of stocks in the S&P 500 currently trading above their 50-day moving averages stands at 78%. As shown in the chart below, this is getting up to the top end of the range the indicator has seen during the bull market. It still has a little bit farther to go before it reaches extreme overbought territory.

"On a sector basis, Financials currently has the highest reading at 94%. This level is at the top of its range over the last year, and it's the most overbought of any sector. Consumer Discretionary has the second highest reading at 89%, followed by Materials and Industrials which both stand at 81%. Telecom and Utilities - two sectors that have been severely lagging recently - have the lowest readings at 56% and 51% respectively."

Source: Bespoke, March 11, 2010.

Bespoke: Large caps vs small caps

"While the last year has been a period where practically all stocks, regardless of style or size, have risen, some stocks have risen more than others. Small caps (Russell 2000) have risen 95%, while large caps (S&P 500) are up a relatively modest 68.5%. This trend, however, is anything but a recent one. Small caps have essentially been outperforming large caps for the last decade. The chart below shows the ratio of the S&P 500 divided by the price of the Russell 2000. When the line is rising, large caps are outperforming small caps, and when the line is declining, small caps are outperforming.

"Based on the relationship between the S&P 500 and the Russell 2000, relative performance between large and small cap stocks follows long-term cyclical trends. As shown in the chart below, periods of outperformance and underperformance by either category are measured in years rather than months. Even with the typical cycle lasting several years, though, the current cycle has been the longest of them all. After peaking out in 1999, large caps have been consistently underperforming small caps for ten years and counting. When it ends is anyone's guess, but it's hard not to argue that large caps are at least due for their day in the sun."

Source: Bespoke, March 9, 2010.

Bespoke: Estimated earnings growth for Q1 2010 and beyond

"Below we highlight the estimated year-over-year earnings growth for the S&P 500 for the next three quarters, along with expected growth ex financials. While ex-financials growth was low in Q4 09, it is also beginning to pick up again. For the first quarter, S&P 500 earnings are expected to be up 28.7% versus Q1 09. Earnings are expected to grow 28.6% in Q2 10, and then drop a little to 22.3% in the third quarter.

"For the first quarter, seven sectors are expected to see year-over-year growth, while three sectors are expected to see a decline. The Materials sector is expected to see the most growth versus Q1 09 at 144%, followed by Financials (86.6%), Technology (51.9%), Consumer Discretionary (47.8%), and Energy (44.7%). Telecom is the only sector expected to see a noteworthy decline at -15.1%. Utilities and Industrials are currently estimated to see year-over-year earnings fall by about 1%."

Source: Bespoke, March 10, 2010.

Bloomberg: S&P rally slowed by fastest cash depletion since 1991

"Equity mutual funds are burning through cash at the fastest rate in 18 years, leaving them with the smallest reserves since 2007 in a sign that gains for the Standard & Poor's 500 Index may slow.

"Cash dropped to 3.6 percent of assets from 5.7 percent in January 2009, leaving managers with $172 billion in the quickest decrease since 1991, Investment Company Institute data show. The last time stock managers held such a small proportion was September 2007, a month before the S&P 500 began a 57 percent drop, according to data compiled by Bloomberg.

"For Parnassus Investments and Janney Montgomery Scott LLC, depleted reserves is a sign returns will fall from last year, when the S&P 500 rose 23 percent, the most since 2003. Bulls say any pullback is a buying opportunity because investors have $3.17 trillion in money-market funds and may return to stocks after putting 16 times more money into bonds since last March.

"It's not a red light, but it's a flashing yellow light that the strongest part of the rally is probably over,' said Jerome Dodson, who oversees $3.6 billion as president of Parnassus in San Francisco and estimates the S&P 500 will climb 6 percent to 9 percent this year. There's not as much buying power out there.'

"Investors are trying to gauge how much money is left to move shares after the S&P 500 surged 70 percent in the 10 months starting in March 2009, and then began an 8.1 percent slide on Jan. 19. The drop, which matches the average size of 117 moderate corrections' tracked by Birinyi Associates Inc. since 1945, may herald a second phase of the bull market after last year's advance surpassed every rally since the 1930s."

Source: Lynn Thomasson, Bloomberg, March 8, 2010.

David Fuller (Fullermoney): Stock markets have further upside potential

"It has been a good four weeks and counting for global stock markets. All technical evidence to date suggests that we have seen a normal correction to the cyclical bull market's trend mean represented by rising 200-day moving averages. The only minor negative is that persistent rallies have replaced short-term oversold conditions with short-term overbought readings. If this matters beyond brief pauses, we would see it in the form of downward dynamics and failed upside breaks from trading ranges.

"However, a more important factor is likely to be the months spent by most equity indices in ranging consolidations, as they gradually worked their way over to their rising MA mean. In the absence of downward dynamics, perhaps caused by some currently unexpected fright, stock markets remain capable of running on the upside.

"Meanwhile, Wall Street has not led - it seldom does - but its all-important leash effect is positive. The US's rally has been led by small-cap indices and the S&P is approaching its January high. Some temporary resistance may be encountered in this region but once again, a downward dynamic would be required to suggest more than a brief pause.

"China's leash effect is second only to Wall Street and stopped being negative with the upside key day reversal on February 3. A break above 3,110 would reaffirm a new pattern of higher reaction lows, although considerably more strength is required to make the overall pattern unequivocally bullish once again."

Source: David Fuller, Fullermoney, March 9, 2010.

David Fuller (Fullermoney): What will be the warning signs for equities?

"In reverse order, I maintain that we are in a cyclical bull market for equities and a secular bull trend for precious metals and most industrial commodities. For instance, gold has a 10-year uptrend - the S&P 500 clearly does not.

"However there has been a high degree of correlation so any sharp sell-off in equities will weigh on commodities for which there has also been considerable investment interest. Nevertheless, most commodities have bounced back quickly, bottoming in October 2008, for instance, in line with most other Fullermoney themes, while the S&P and most other OECD country stock markets did not reach their lows until March 2009.

"The main point behind my stock market warning signals, which I have mentioned before and will again, is that too much good news is bad news. 1) Strong economic growth competes for capital and invites monetary tightening by central banks; 2) strong growth and too much speculation would lift oil prices over the low $80s highs for this cycle to date, towards headwind levels of $100 or more; 3) US 10-year Treasury yields above 4% would be an advance warning but the real danger area is above 5%; 4) a very weak USD could undermine confidence but this is clearly not a threat today. Also watch the February lows for stock market indices; the cyclical bull is intact while they hold."

Source: David Fuller, Fullermoney, March 5, 2010.

Bloomberg: Buy Asia stocks before "green" light, Goldman says

"Investors should buy Asian stocks outside Japan after valuations dropped and before sentiment strengthens further, Goldman Sachs Group Inc. said.

"By the time all the lights turn green, the race will already be well under way,' Goldman Sachs analysts led by Timothy Moe wrote today. Sentiment and valuation will improve as the year progresses, and we would prefer to be early.'

"The MSCI Asia-Pacific excluding Japan Index remains 0.5 percent lower this year, having rebounded from year-to-date losses of as much as 9.7 percent. Stocks slid earlier this year on concern that China will tighten lending to combat faster inflation and that Greece's debt crisis will spread.

"Analysts' earnings growth estimates for this year have climbed to 26 percent on average, near Goldman Sachs's 30 percent forecast, according to the report. The most profitable securities firm in Wall Street history is predicting a 21 percent increase in Asian corporate earnings in 2011.

"The MSCI index's valuation has dropped to 14.4 times estimated earnings from as high as 29.3 times in November, after profit estimates were upgraded, according to weekly data compiled by Bloomberg.

"We view the risk/reward balance very positively from a strategic perspective,' the Goldman Sachs analysts wrote.

"Goldman Sachs said it remains most optimistic on the outlook for stock markets in China, South Korea and Taiwan. Indexes tracking Chinese shares traded in Shanghai and Hong Kong and Taiwan's Taiex index have retreated at least 5 percent this year, among the 10 worst performers globally. South Korea's Kospi index has fallen 1.4 percent."

Source: Shiyin Chen, Bloomberg, March 11, 2010.

MoneyNews: S&P - US debt level poses risk to strong dollar

"The US dollar is still the most important world currency, Standard & Poor's said on Thursday, but added that rising levels of US debt and dependence on foreigners to finance much of pose risks to the currency's primacy.

"Without a credible plan to rein in fiscal spending, the agency said external creditors could reduce dollar holdings, which could put pressure on the United States' AAA' credit rating, which keeps government borrowing costs low.

"For now, the credit ratings agency said the size of the US economy - the world's largest - and the depth of its financial markets mean the dollar will continue to dominate global trade and foreign exchange transactions.

"Those advantages helped the dollar retain its top status despite the financial crisis of 2008-09, which began in the United States, S&P said in the report.

"The agency also said the dollar's role is an important factor supporting the United States' AAA credit rating - the highest investment-grade rating.

"The main risk to the dollar's status comes from the growing amount of US government debt, S&P said, particularly the share held by foreign central banks and sovereign wealth funds.

"It also said widening US fiscal deficits were a risk, adding without a medium-term fiscal consolidation plan that the market views as credible, external creditors could reduce their dollar holdings, especially if they conclude that euro zone members are adopting stronger macroeconomic policies.'"

Source: MoneyNews, March 11, 2010.

Financial Times: Beijing studies severing dollar peg

"China's central bank chief laid the groundwork for an appreciation of the renminbi at the weekend when he described the current dollar peg as temporary, striking a more emollient tone after months of tough opposition in Beijing to a shift in exchange rate policy.

"Zhou Xiaochuan, governor of the People's Bank of China, gave the strongest hint yet from a senior official that China would abandon the unofficial dollar peg, in place since mid-2008. He said it was a 'special' policy to weather the financial crisis.

"This is a part of our package of policies for dealing with the global financial crisis. Sooner or later, we will exit the policies.'

"Mr Zhou's comments contrasted with recent Chinese comments on its currency policy in the face of international criticism that the renminbi was undervalued. In December, premier Wen Jiabao said: We will not yield to any pressure of any form forcing us to appreciate.' Chinese officials have repeatedly emphasised the need for a stable exchange rate.

"However, while the recent increase in consumer prices in China has strengthened the hand of those officials who think the currency should now rise, it is not clear that this argument has yet won over the country's senior leaders.

"Indeed, Mr Zhou gave no hint about the possible timing of a shift in policy."

Source: Geoff Dyer, Financial Times, March 6, 2010.

Bespoke: Bespoke's commodity snapshot

"The stock market is up about 65% since the 3/9/09 low, but oil has actually outperformed stocks over this time period with a gain of 72.64%. Below we highlight the performance of ten major commodities over the last year. As shown, copper is up the most with a gain of 108%, while orange juice ranks second with a gain of 101%. Of the three main precious metals, platinum is up the most at 50%, followed by silver at +33.73%, and then gold at +22.16%. Even natural gas is up since the March 9th, 2009 low with a gain of 16%. Wheat and corn are the only commodities shown that are down over the last year. Corn is down 11%, while wheat is down 18.27%."

Source: Bespoke, March 9, 2010.

Bill King (The King Report): Why is gold declining?

"Our view is gold is retrenching because:

• UK QE has ended (for now)

• US QE will end in three weeks (for now)

• The ECB did a massive €295B drain (can you imagine the market reaction if Bennie Mae drained $500B in one shot?]

• China is signaling that it wants to rein in inflation by tightening credit, hiking real estate down payments to 50% and allowing the yuan to appreciate

• Europe's sovereign debt crisis has ebbed (for now)

• Food commodities have broken down

• Gold stocks have greatly underperformed gold since mid-January (gold stocks tend to lead)"

Source: Bill King, The King Report, March 11, 2010.

Financial Times: Goldman and JPMorgan enter metal warehousing

"As piles of base metals from aluminium to nickel build up due to poor demand, Goldman Sachs and JPMorgan have entered the little known but very profitable business of metal warehousing. The deals reflect banks' appetite for exposure to physical commodities beyond traditional commodities derivatives.

"Stockpiles at London Metal Exchange's registered depots surge to an all-time high of 6m tonnes - up from 1m in 2007. Traders and bankers say warehousing is a classic anti-cyclical' business as it flourishes when demand for metals is lacklustre and stockpiles mount.

"The business is booming right now,' says a commodities banker in London.

"The current prosperous period contrasts with much of the 2000-2008 cycle, when strong economic growth and metals consumption reduced LME inventories to near-record lows, sharply cutting warehouses' income.

"Traders say the bank decision will reshape the close-knit warehousing industry as Goldman Sachs and JPMorgan will control the depots where more than half of the LME's registered stocks are held. The LME is the world's largest metal exchange."

Source: Javier Blas, Financial Times, March 2, 2010.

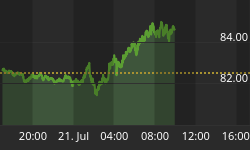

The Wall Street Journal: What's behind oil's spike?

"Oil prices hit an eight-week high today at $82 a barrel. WSJ's Grainne McCarthy explains what's behind the spike, including the potential for demand to pick up as the economy begins to recover. She joins Dennis Berman and Simon Constable in the News Hub."

Source: The Wall Street Journal, March 10, 2010.

Bloomberg: Copper imports by China may fall 16%, analyst says

"China's net imports of refined copper may fall 16 percent this year as manufacturers run down stockpiles and domestic production increases, an analyst at Shanghai Nonferrous Metals, said.

"Net inbound shipments may fall to 2.6 million metric tons, said Zhou Qian in an interview at a Nanjing conference today. Real demand may grow 14 percent to 7.55 million tons, he said.

"Inbound shipments of refined copper fell for the first time in three months in January as domestic supplies increased and seasonal demand slowed. The country has been running down stockpiles in bonded warehouses, Macquarie Group Ltd. has said. Traders store shipments in a bonded zone before paying duties.

"Downstream demand is expected to be quite strong from real estate and transport industries in 2010, and still grow modestly from the home appliance sector,' Li Lan, a researcher at Beijing General Research Institute of Mining and Metallurgy, said in Nanjing. In addition, demand from electronics makers may increase too as exports improve.'

"A steeper fall in imports may be avoided by firm demand and as scrap supplies fail to return to levels before the financial crisis, said Zhou. Buyers may run down stockpiles by about 350,000 tons this year, he said, without giving figures for total current inventories. China may produce 4.6 million tons of copper in 2010, up 12 percent from an estimated 4.11 million tons last year, Zhou said."

Source: Richard Dobson and Tan Hwee Ann, Bloomberg, March 9, 2010.

Bloomberg: China may start raising interest rates as prices gain

"China's inflation accelerated in February, according to a survey of economists, and exports climbed in the month, increasing the likelihood of the central bank raising interest rates from a five-year low.

"Consumer prices rose 2.5 percent from a year before, the most in 16 months, according to the median of 29 estimates in a Bloomberg News survey before tomorrow's report. While the gain was likely exaggerated by seasonal factors, economists project the momentum to continue, sending the rate to as high as 4.4 percent during the year, a separate survey showed last week.

"Inflation, property speculation and risks for banks are among Premier Wen Jiabao's prime concerns after a record 9.59 trillion yuan ($1.4 trillion) of loans jumpstarted growth last year. Central bank Governor Zhou Xiaochuan said March 6 that while stimulus policies must end 'sooner or later', China needs to be cautious in timing an exit because a global recovery isn't solid'.

"We believe the central bank sees inflation as a big danger to the economy,' said Wang Qian, an economist with JPMorgan Chase & Co. in Hong Kong. As such, the central bank is likely to hike interest rates soon to manage inflation expectations.'

"Wang sees a 0.27 percentage point increase in the one-year lending and deposit rates as early as this month. In January, consumer prices rose 1.5 percent, the third monthly increase after a nine-month run of deflation.

"Price pressures are stemming from rising commodity costs, an overhaul of resource prices and the expansion of credit, the nation's top economic planning agency said in a report to lawmakers last week. Producer prices may have climbed 5.1 percent in February, the biggest gain in 16 months, the Bloomberg News survey showed."

Source: Paul Panckhurst and Chris Anstey, Bloomberg, March 10, 2010.

Financial Times: China export growth beats estimates

"Chinese exports rose 45.7 per cent in February from a year earlier, beating forecasts and providing fresh evidence of a robust recovery in the economy poised to overtake Japan this year as the world's second-largest.

"The export number points to solid underlying improvement in external demand, which should provide significant support to China's recovery in 2010,' said Brian Jackson, an analyst at RBC Capital Markets. This should make policymakers in Beijing more comfortable with the idea of allowing currency appreciation to help deal with building price pressures.'

"Chinese exports registered their biggest fall of the financial crisis in February 2009 and analysts were expecting high growth figures as a result but the performance last month was better than most had predicted. Exports had risen 21 per cent in January.

"Imports rose 44.7 per cent in February from a year before.

"The strong trade figures are partly due to a low base in February last year and but it is clear that exports are recovering strongly and this trend is likely to continue,' said Zhu Jianfang, chief economist at Citic Securities in Beijing. Rising imports show domestic demand is also very strong.'"

Source: Jamil Anderlini, Financial Times, March 10, 2010.

CNBC: China needs to drive consumption

"China needs to encourage consumption, says Tomo Kinoshita, deputy head of economics, Asia ex-Japan at Nomura International. He explains why inflation is not a big threat and why shifts in labor could become a problem, with CNBC's Chloe Cho and Anna Edwards."

Source: CNBC, March 11, 2010.

Financial Times: Debunking the myth of a China collapse

"Global sentiment towards China's economy and asset markets has turned from exuberance just a few months ago to overriding concern about the side-effects of last year's remarkable credit growth. A number of commentators have warned of credit excesses and an over-investment bubble, which they say could bring economic turmoil.

"Critics have also pointed to China's Rmb 4,000bn stimulus programme and last year's 33 per cent surge in new bank lending as obvious hallmarks of excess liquidity and a lowering of lending standards. Some have raised concerns about hidden debt risks among local government investment entities, while media reports of Chinese "ghost cities" and empty commercial property are cited as evidence of local excesses.

"The worst-case fears concerning the property market are based on a layer of truth and we have previously highlighted the untenable nature of price increases in some big cities, as well as the possibility that last year's boom was partly fuelled by misdirected bank loans. However, there are crucial differences between China's property markets and those of the US or Dubai.

"Unlike the dramatic increase in household leverage that precipitated the US sub-prime crisis, Chinese household debt amounts to approximately 17 per cent of GDP, compared to roughly 96 per cent in the US and 62 per cent in the eurozone. Homebuyers in China are required to make minimum downpayments of 30 per cent before receiving a mortgage, and at least 40 per cent for a second home.

"Although price increases in the Chinese residential market appear rapid (over 20 per cent in 2009), such headline figures cannot be viewed in isolation. Over the past 5 years, urban household incomes grew at a 13.2 per cent compound annual growth rate, compared to an 11.9 per cent CAGR in home prices. Pockets of overheating can be found in some regional markets: in Beijing, Shanghai, Shenzhen and Hangzhou, for instance, prices outpaced income growth by more than 5 percentage points over the same period. But this can be seen as a symptom of new urban wealth being put to speculative use rather than the profligate use of leverage.

"The combination of excessive leverage and mortgage securitisation were at the epicentre of the US sub-prime crisis. Both these factors are absent in the Chinese context. The commercial property sector has inspired just as much concern, with prices rising 16 per cent in 2009, despite low rental yields and prime office vacancy rates as high as 21 per cent and 14 per cent in Beijing and Shanghai, respectively. Yet occupancy and rental rates have started to pick up for prime properties."

Click here for the full article.

Source: Jing Ulrich, Financial Times, March 10, 2010.

Bloomberg: Greek crisis is over, rest of region safe, Prodi says

"The worst of Greece's financial crisis is over and other European nations won't follow in its path, said former European Commission President Romano Prodi.

"For Greece, the problem is completely over,' said Prodi, who was also Italian prime minister, in an interview in Shanghai today. I don't see any other case now in Europe. I don't think there is any reason to think the euro system will collapse or will suffer greatly because of Greece.'

"Greek officials are trying to convince investors they can cut the nation's budget deficit, which at 12.7 percent of gross domestic product was Europe's largest in 2009. The government last week announced spending cuts and tax increases totaling 4.8 billion euros ($6.5 billion), the third round of austerity measures this year.

"French President Nicolas Sarkozy said on March 7 the 16-nation euro region must support Greece, which has more than 20 billion euros of debt falling due in April and May, or risk destroying the currency. German Chancellor Angela Merkel, who runs Europe's largest economy, has so far refused to give the green light to any aid package.

"Intervention by European nations to date was enough' and countries such as Spain and Portugal have plenty of time' to get their finances in order, said Prodi.

"Investors don't yet share Prodi's optimism about Greece. While the extra yield they demand to hold Greek 10-year debt rather than German equivalents has eased 88 basis points from a record of 396 in January, it's still more than four times the level of two years ago. The premium on Spanish 10-year bonds is 69 basis points, twice what it was two years ago.

"Greek Prime Minister George Papandreou, during a trip to the US yesterday, said President Barack Obama supported the measures that Greece is taking to put its public finances in order.

"We're not asking for a bailout, we're not asking for financial help from anyone,' Papandreou told reporters in Washington yesterday. We are taking measures to put our economy on the right path.'"

Source: Bloomberg, March 10, 2010.

Telegraph: Fitch warns Britain and questions Greek rescue as sovereign risks grow

"Brian Coulton, the agency's head of sovereign ratings, said the UK has seen the most rapid rise in the ratio of public debt to GDP of any AAA-rated country' and is courting fate with its leisurely plan to halve the deficit by the middle of the decade.

"It is frankly too slow, a pedestrian pace. Why the UK thinks it has more time than other countries, we're not sure. This needs to be reoriented,' he told the Fitch forum on sovereign hotspots.

"A string of European states are stepping up the pace of retrenchment, aiming to cut deficits to 3pc of GDP within three years. The risk is that Britain will soon stick out like a sore thumb, left behind with a shockingly large deficit long after such loose fiscal policy can be justified as a crisis measure. The UK deficit this year is 12.6pc of GDP, the highest among G10 states.

"The Government is clearly counting on a Korean' recovery, modelled on Korea's fast return to trend growth following the Asian crisis in 1998. It relies on rising output and tax revenues to plug much of the deficit. This is an optimistic assumption,' said Fitch.

"There is a distinct possibility' that Britain will face something closer to Japan's Lost Decade' when a bursting debt bubble left the country on a permanently lower growth path. The UK faces the same massive deleveraging by the private sector,' said Mr Coulton."

Source: Ambrose Evans-Pritchard, Telegraph, March 9, 2010.

Did you enjoy this post? If so, click here to subscribe to updates to Investment Postcards from Cape Town by e-mail.