I have worried for a while about what might happen when we approach the end of March (see for example this comment in January), when the Fed's buying program officially end. Until today, it seemed that even with all of the concerns about Greece and the ever-growing pile of debt that the Treasury needs to finance the market was remarkably sanguine. Too sanguine, perhaps.

We began the day with Portugal getting downgraded to AA- by Fitch and more back-and-forth about whether Greece can get help from the IMF (which seems the only feasible alternative for her now). Durable Goods was stronger-than-expected, +0.9% ex-transportation, but New Home Sales weaker-than-expected at a new all-time low. It looked like it may be another quiet day, although bonds felt heavy.

Heavy, indeed. As the day went on, Treasuries began to slip more seriously, and swap spreads imploded for a second day. I can't see sell-side flows from where I sit, so I can't discern whether this is tied to corporate issuance, as I originally thought (which seems unlikely, now), some speculator blow-up, or simply a panicky technical breakdown as 10y swap spreads break to all-time lows (see chart below, source Bloomberg).

10y Swap Spreads Reached Rock-Bottom (and then started to dig)

There are even some fairly optimistic ways that this sort of contraction in swap spreads could develop, although the fact that the move is so precipitous makes me think they are unlikely: banks currently hold lots of Treasuries in lieu of loans as assets. If a bank suddenly started making lots of floating-rate loans, it would behoove them to sell swap spreads to simultaneously remove the Treasuries from the balance sheet and match their assets (a short-dated, floating-rate loan) to their liabilities (long-dated fixed-rate, ordinarily). I doubt that's what is happening, but I don't have a good answer.

The bottom line is that Treasury debt is cheapening relative to other interest rates, which isn't surprising when there is so much of it. In fact, not only is it not surprising, it is to be expected - and even more than that, it is entirely consistent with history. See the chart below (Source: Bloomberg), which shows that this shouldn't be particularly surprising after all.

The More You Sell, The Cheaper The Price: Econ 101

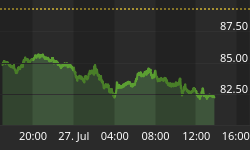

Exhibit 2 in that argument? The Treasury today auctioned a $42bln 5y note that was poorly received and sported a long tail. The 10y note contract fell 1-06 today, the biggest drop in some time, and 10-year nominal yields spiked to 3.83%. The intermediate-term chart below shows the importance of today's selloff. There is some further support for prices between here and 4% yields (see Chart, source Bloomberg), but this is the wrong time of year to expect support to hold in the bond market.

A Bad Place For Yields With Quarter-End Yet To Come

With the Fed not buying and the Treasury with no choice but to sell, I am not sure I want to be the buyer. I guess I am not the only person thinking that at the moment! We all know that yields are artificially low right now. Soon, we might get to find out how low.

Initial Claims on Thursday is the release of note. Consensus calls for a further improvement, to 450k from 457k. I never seem to hear any commentary about why Claims aren't improving as fast as the bullish economists keep telling us they should. The forecasts keep getting pushed back - every week is expected to show a little improvement, seemingly because economists sort of think they should be improving. But the 2010 low is still the 433k recorded in the first week of the year. I am singularly unimpressed with the behavior of the Claims data. It is all well and good to say "well, employment is a lagging indicator," but at some point before we get job growth I would still expect to see businesses stop laying people off! There is also another auction tomorrow, this time of $32bln 7-year notes. How about a little fire, scarecrow?!

Today was a rare exception where we got volatility during the annual NCAA tournament, although to be fair there were no games played today. But the sudden, sharp move in bonds and spreads makes me nervous, especially since March 31st has been making me nervous for a couple of months anyway. As of this writing (3pm ET), stocks are only down 0.5%, but if rates start to trend higher then equities are unlikely to remain an island in the storm. I would be very defensive into the end of the quarter - not because I expect something bad to happen, but because I have no real reason to expect something good to happen.