For the week, the S&P500 fell 6.4% (down 0.4% y-t-d), and the Dow dropped 5.7% (down 0.5%). The Banks were hit for 7.2% (up 21.0%), and the Broker/Dealers were smacked for 7.3% (down 3.3%). The Morgan Stanley Cyclicals were hammered for 9.2% (up 2.5%), and the Transports were hit for 8.0% (up 4.8%). The Morgan Stanley Consumer index declined 4.6% (up 1.6%), and the Utilities fell 4.1% (down 6.1%). The S&P 400 Mid-Caps sank 8.1% (up 4.1%), and the small cap Russell 2000 dropped 8.9% (up 4.4%). The Nasdaq100 fell 7.6% (down 0.6%), and the Morgan Stanley High Tech index dropped 7.5% (down 4.2%). The Semiconductors sank 7.8% (down 3.7%). The InteractiveWeek Internet index fell 7.8% (down 0.3%). The Biotechs were clobbered for 12.6%, reducing 2010 gains to 11.2%. Although bullion surged $29, the HUI gold index declined 2.6% (up 5.0%).

One-month Treasury bill rates ended the week at 7 bps and three-month bills closed at 12 bps. Two-year government yields dropped 14 bps to 0.74%. Five-year T-note yields sank 23 bps to 2.13%. Ten-year yields fell 23 bps to 3.42%. Long bond yields dropped 25 bps to 4.27%. Benchmark Fannie MBS yields declined 12 bps to 4.27%. The spread between 10-year Treasury and benchmark MBS yields widened a notable 11 bps to a six-month high 85 bps. Agency 10-yr debt spreads widened 5 bps to 43 bps. The implied yield on December 2010 eurodollar futures actually rose 7 bps to 0.895%. The 10-year dollar swap spread increased 4.25 to 4.75. The 30-year swap spread increased 2.5 to negative 20.75. Corporate bond spreads widened. An index of investment grade bond spreads widened 35 to 128 bps.

Debt issuance slowed markedly. Investment grade issuers included Ironshore Holdings $250 million, and Lennox International $200 million.

Junk issuers included Beazer Homes $300 million, American Petroleum $285 million, Lantheus Medical Imaging $250 million, and Oncure Medical $210 million.

Convert issues included Owens Brockway $600 million.

International dollar debt sales included Ineos Finance $570 million.

U.K. 10-year gilt yields declined 8 bps to 3.83%, and German bund yields sank 22 bps to 2.79%. Greek bond yields surged 348 bps to 12.42%, and Portuguese yields jumped 114 bps to 6.27%. The German DAX equities index was clobbered for 6.9% (down 4.1% y-t-d). Japanese 10-year "JGB" yields dipped one basis point to 1.27%. The Nikkei 225 sank 7.2% (down 1.7%). Emerging markets were hit hard. For the week, Brazil's Bovespa equities index sank 6.9% (down 8.3%), and Mexico's Bolsa fell 3.7% (down 2.0%). Russia's RTS equities index was down 13.2% (down 5.5%). India's Sensex equities index fell 4.5% (down 3.9%). China's Shanghai Exchange sank 6.8%, boosting 2010 losses to 18.0%. Brazil's benchmark dollar bond yields jumped 14 bps to 5.01%, and Mexico's benchmark bond yields surged 23 bps to 5.13%.

Freddie Mac 30-year fixed mortgage rates declined 6 bps last week to 5.00% (up 16bps y-o-y). Fifteen-year fixed rates fell 3 bps to 4.36% (down 16bps y-o-y). One-year ARMs sank 18 bps to 4.07% (down 71bps y-o-y). Bankrate's survey of jumbo mortgage borrowing costs had 30-yr fixed jumbo rates down 4 bps to 5.78% (down 56bps y-o-y).

Federal Reserve Credit dipped $1.5bn last week to $2.311 TN. Fed Credit was up $96.8bn y-t-d (13.3% annualized) and $229bn, or 11.0%, from a year ago. Elsewhere, Fed Foreign Holdings of Treasury, Agency Debt this past week (ended 5/5) increased $4.9bn to a record $3.075 TN. "Custody holdings" have increased $106bn y-t-d (11.0% annualized), with a one-year rise of $410bn, or 15.5%.

M2 (narrow) "money" supply was up $20bn to $8.470 TN (week of 4/26). Narrow "money" has declined $42bn y-t-d (1.5% annualized). Over the past year, M2 grew 1.4%. For the week, Currency added $1.7bn, and Demand & Checkable Deposits increased $1.8bn. Savings Deposits surged $24.7bn, while Small Denominated Deposits fell $4.5bn. Retail Money Fund assets declined $3.7bn.

Total Money Market Fund assets (from Invest Co Inst) dropped $19.0bn to $2.853 TN. In the first 18 weeks of the year, money fund assets have dropped $440bn, with a one-year decline of $934bn, or 24.7%.

Total Commercial Paper outstanding jumped $32.9bn last week to $1.102 TN. CP has declined $61bn, or 16% annualized, year-to-date, and was down $314bn from a year ago (22%).

International reserve assets (excluding gold) - as tallied by Bloomberg's Alex Tanzi - were up $1.260 TN y-o-y, or 18.9%, to a record $7.981 TN.

Global Credit Market Watch:

May 7 - Bloomberg (James G. Neuger and Gregory Viscusi): "European leaders agreed to set up an emergency fund to halt the spread of Greece's fiscal woes, seeking to prevent a sovereign debt crisis from shattering confidence in the 11-year-old euro. Jolted into action by the sliding currency and soaring bond yields in Portugal and Spain, leaders of the 16 euro countries said the workings of the financial backstop will be hammered out before the markets open on May 10. "We will defend the euro, whatever it takes," European Commission President Jose Barroso told reporters early today after the leaders met in Brussels."

May 7 - Bloomberg (Anchalee Worrachate): "Greek bonds tumbled as world leaders prepared to discuss ways to fix Europe's debt crisis and halt the contagion that's sending government securities across the region lower. The extra yield investors demand for holding 10-year Greek, Spanish or Irish debt instead of benchmark German securities surged to the highest since before the euro's debut in 1999 and U.S. Treasuries headed for the steepest weekly gain in more than a year."

May 7 - Bloomberg (Shannon D. Harrington): "The 13-month rally in credit markets is unraveling... Money markets showed banks may be the most reluctant to lend to each other in six months and a derivatives index used to protect against European bank failures soared the most on record. U.S. company bond sales are poised for the slowest week this year, while in Europe they all but disappeared..."

May 7 - Bloomberg (Abigail Moses): "The cost of insuring against losses on European bank bonds soared to a record, surpassing levels triggered by the collapse of Lehman Brothers... The Markit iTraxx Financial Index of credit-default swaps on 25 banks and insurers soared as much as 40 bps to 223, according to JPMorgan... Swaps on Greece, Portugal, Spain and Italy rose to or near all-time high levels."

May 7 - Bloomberg (Sarah McDonald): "The cost of protecting Asian corporate bonds from default surged the most in more than 14 months after the European Central Bank resisted investor pressure to take new steps to contain Greece's debt crisis and U.S. stocks slumped."

May 4 - Bloomberg (Simon Kennedy): "European Central Bank President Jean-Claude Trichet, who capitulated on a January pledge not to relax lending rules for the sake of one country, may have to sacrifice more principles to prevent Greece from bringing down the euro. Trichet yesterday diluted rules for the second time in a month to guarantee the ECB will keep taking Greek government bonds as collateral for loans. The central bank may have to extend that to other nations, renew a program of lending unlimited cash to banks for a year, and even start buying government debt if the 110 billion-euro ($146 billion) bailout plan for Greece fails to stem the euro's slide, economists said."

May 7 - Bloomberg (Lukanyo Mnyanda and Paul Dobson): "The pound sank the most in a year and a half against the euro and British bonds fell as the U.K. election failed to produce an outright winner, fueling concern that measures to tame the budget deficit will be delayed."

May 4 - Bloomberg (Emre Peker): "The leveraged-loan market shrunk last month to its size in July 2007, right before the onset of the credit crunch, amid a lack of new issues of collateralized loan obligations, CreditSights Inc. said. The amount of loans on the S&P/LSTA Leveraged Loan Index, representing about 95% of the institutional market for U.S. bank debt, dropped by $9.95 billion to $500 billion in April..."

Global Government Finance Bubble Watch:

May 7 - Bloomberg (Saburo Funabiki): "The Bank of Japan said it would pump 2 trillion yen ($21.8 billion) into the financial system to help stabilize the market after the Greek debt crisis set off a plunge in stocks worldwide... The injection was the largest since December 2008...

Currency Watch:

The dollar index surged 3.2% this week to 84.45 (up 8.5% y-t-d). For the week on the upside, the Japanese yen increased 2.7%. For the week on the downside, the Brazilian real declined 5.8%, the Swedish krona 5.3%, the Norwegian krone 5.3%, the Danish krone 4.2%, the euro 4.2%, the South Korean won 4.1%, the Mexican peso 4.1%, the Australian dollar 4.0%, the British pound 3.0%, the Swiss franc 2.8%, the Canadian dollar 2.4%, the New Zealand dollar 1.8%, and the Singapore dollar 1.7%.

Commodities Watch:

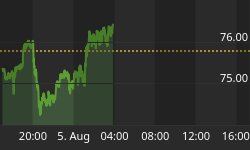

The CRB index was slammed for 5.9% (down 7.8% y-t-d). The Goldman Sachs Commodities Index (GSCI) dropped 8.4% (down 4.0% y-t-d). Spot Gold surged 2.4% to $1,208 (up 10.1% y-t-d). Silver dipped 1.4% to $18.39 (up 9.1% y-t-d). June Crude sank $10.92 to $75.23 (down 5% y-t-d). June Gasoline fell 11.1% (up 3.8% y-t-d), while June Natural Gas gained 2.1% (down 28% y-t-d). July Copper was drilled for 6.0% (down 6% y-t-d). May Wheat gained 1.7% (down 8% y-t-d), while May Corn slipped 0.4% (down 12% y-t-d).

China Bubble Watch:

May 5 - Bloomberg: "Baoshan Iron & Steel Co., the biggest supplier of automotive steel in China, said car production is slowing after a more than 50% gain in the first quarter. Steel demand from automakers in China has dropped "a bit,' General Manager Ma Guoqiang told investors..."

India Watch:

May 7 - Bloomberg (V. Ramakrishnan): "India should tax foreign capital inflows into the equity market that stay invested for less than two years to protect its financial system and sustain economic growth, said former central bank governor Bimal Jalan. "If you have unstable, unpredictable, volatile capital flows which are affecting financial stability as well as the real economy's stability, then you have to find a way of handling them so that they are not free for all,' Jalan, who headed the Reserve Bank of India between 1997 and 2003, said..."

May 5 - Bloomberg (Rakteem Katakey): "India is poised to overtake Japan to become the world's third-biggest crude oil importer... in a nation where 30 percent of the population is younger than 15 years."

Asia Bubble Watch:

May 4 - Bloomberg (Stephanie Phang and Michael Munoz): "Malaysia's export growth doubled in March as the global rebound lifted demand for the country's electronics and commodities, boosting expansion in Southeast Asia's third-largest economy. Overseas shipments rose 36.4% from a year earlier..."

Latin America Bubble Watch:

May 7 - Bloomberg (Iuri Dantas and Andre Soliani): "Brazil's consumer prices accelerated further beyond the government's 4.5% target in April on soaring food costs... Prices rose 5.26% in April from a year earlier..."

May 3 - Bloomberg (Gabrielle Coppola): "Brazilian banks are selling a record amount of subordinated dollar bonds to meet a surge in loan demand as growth in Latin America's largest economy accelerates. Itau Unibanco Holding SA, Brazil's biggest lender by market value, and the financial unit of Votorantim Participacoes SA led $3 billion of the offerings this year... More than half the sales took place in April. A 17% jump in loans in March to a record is fueling the sales because the securities can count as capital..."

May 4 - Bloomberg (Fabiola Moura): "Latin America and the Caribbean's faster-than-forecast recovery from the global financial crisis requires "careful' macroeconomic measures to avoid the emergence of a bubble, the International Monetary Fund said."

Unbalanced Global Economy Watch:

May 7 - Bloomberg (Greg Quinn): "Canada had the biggest jump in employment on record last month... Employment rose by 108,700 in April, the most in records dating back to 1976... The jobless rate fell to 8.1% from 8.2%...

May 7 - Bloomberg (Joao Lima): "Portugal's trade gap narrowed 3.7% in the first quarter from the same period last year as exports increased 15%..."

May 4 - Bloomberg (Denis Maternovsky and Ilya Arkhipov): "Moscow Mayor Yuri Luzhkov's wife earned more than $1 billion last year, an amount that would take the 73-year-old leader almost four millennia to match at his current income. Luzhkov, who has run Europe's most-populous city since 1992, declared 30.9 billion rubles ($1.05 billion) in income for his wife, ZAO Inteko holding company owner Yelena Baturina, 47..."

U.S. Bubble Economy Watch:

May 3 - Bloomberg (John Detrixhe and Craig Trudell): "Companies sold $33.7 billion of junk bonds in April, a record for the month... Moody's... says issuance may rise 10% this year, while investment-grade sales drop 7%."

May 4 - Bloomberg (Don Jeffrey and William Rochelle): "U.S. bankruptcy filings by individuals and businesses fell in April to the second-highest level since changes to the law in 2005 made it harder for individuals to seek protection from creditors. Filings totaled almost 146,000 in April..."

Real Estate Watch:

May 4 - Bloomberg (John Gittelsohn and Nadja Brandt): "BP Plc's burgeoning oil spill in the Gulf of Mexico may hurt property owners more than any storm as sludge threatens to wreak long-term damage on the region's most valuable asset: its environment. "I've been through Hurricane Camille, Hurricane Frederick and Hurricane Katrina,' said Greg Miller, owner of Fort Morgan Realty and Development Inc. in Gulf Shores, Alabama. "They all pale in comparison to this.'"

May 5 - Bloomberg (Peter Woodifield): "Wealthy Greeks helped push up London luxury-home prices at the fastest rate in two years as they seek a "safe haven' from their country's sovereign debt crisis, Knight Frank LLP said... Prices of houses and apartments costing more than 1 million pounds ($1.52 million) rose about 21% in April from a year earlier..."

Central Bank Watch:

May 4 - Bloomberg (Jacob Greber): "Australia's central bank increased the benchmark interest rate for the sixth time since early October... to 4.5% from 4.25%..."

May 5 - Bloomberg (Josiane Kremer): "Norges Bank raised its benchmark interest rate a quarter point, resuming a tightening cycle policy makers shelved last quarter as they seek to balance the krone's appreciation against rebounding household demand. The central bank increased the overnight deposit rate to 2%..."

Fiscal Watch:

April 30 - Wall Street Journal (Nick Timiraos): "The U.S. government's massive share of the nation's mortgage market grew even larger during the first quarter. Government-related entities backed 96.5% of all home loans during the first quarter, up from 90% in 2009... The increase was driven by a jump in the share of loans backed by Fannie Mae and Freddie Mac...'Fannie and Freddie have to get smaller and less relevant in order to revamp them, and instead, every day they're getting bigger and bigger and bigger,' said Paul Bossidy, chief executive of Clayton Holdings LLC, a mortgage analytics firm."

May 5 - Bloomberg (Jamie McGee and Darrell Preston): "Warren Buffett... said the U.S. would probably feel compelled to rescue a state facing default after the government committed $700 billion to bail out financial firms and automakers. "It would be hard in the end for the federal government to turn away a state having extreme financial difficulty when they've gone to General Motors and other entities and saved them,' Buffett, 79, told shareholders... "I don't know how you would tell a state you're going to stiff-arm them with all the bailouts of corporations.'"

New York Watch:

May 6 - Bloomberg (Henry Goldman): "New York Mayor Michael Bloomberg presented a $62.9 billion budget for fiscal 2011 that eliminates 11,000 positions, or 3.6% of the city's workforce, in light of a $1.3 billion potential loss of state aid. Proposing no new taxes for the year that begins July 1, Bloomberg said the city may fire 4,419 of its 80,000 teachers and eliminate about 2,000 more through attrition."

May 4 - Bloomberg (Michael Quint): "New York Governor David Paterson said his next emergency spending bill will furlough 100,000 state workers for one day a week to help keep the government operating in the absence of a budget."

"Liquidationist" Revisited

John Maynard Keynes dismissed the "austere and puritanical" "liquidationists." Over the years, Chairman Bernanke has similarly ridiculed the "Bubble poppers" - those in the late 1920's that believed that the Fed needed to tighten policy to rein in out of control securities leveraging, speculation and economic imbalances. Dr. Bernanke has blamed "overzealous" central banking for contributing to the Great Depression.

Andrew Mellon has proved the perfect poster child for those seeking to simplify, distort and discredit so-called "liquidationist" analysis: "Liquidate labor, liquidate stocks, liquidate the farmers, liquidate real estate... It will purge the rottenness out of the system. High costs of living and high living will come down. People will work harder, live a more moral life. Values will be adjusted, and enterprising people will pick up the wrecks from less competent people"...

History has not been kind to Andrew Mellon and "liquidationist" thinking. Mr. Mellon could have phrased his views in a more palatable fashion. All the same, there was actually an expansive body of writings and insightful economic analysis during the late-twenties and into the depression that went significantly beyond moral judgments. An impressive group of scholars and statesmen from this period believed that the U.S. Credit system and economy had become grossly distorted from a runaway inflation that had commenced back with the outbreak of the First World War.

These "old timers" had survived repeated inflationary booms, busts and destabilizing monetary instability going back to the 1860's. From experience, they understood the perils of rapid Credit expansion and the necessity of reining in excesses early in the cycle. The "anti-inflationists" were convinced that the only way to return to a more even keel was to bring down the inflated price level; to bring down inflated asset values; to bring down inflated incomes; and to stabilize economic output at more sustainable levels.

After a massive inflation, the "old timers" understood that the only way to return balance and monetary order to the system was through quashing speculation, financial excess and economic profligacy. And this view was much more based on the understanding of the inherent instability of Credit inflations than it was a "puritanical" judgment. Sustaining a Bubble was certainly not a viable option.

From Dr. Bernanke (extracted from his speech, "Asset-Price "Bubbles' and Monetary Policy", October 15, 2002): "The correct interpretation of the 1920s, then, is not the popular one--that the stock market got overvalued, crashed, and caused a Great Depression. The true story is that monetary policy tried overzealously to stop the rise in stock prices. But the main effect of the tight monetary policy... was to slow the economy--both domestically and, through the workings of the gold standard, abroad. The slowing economy, together with rising interest rates, was in turn a major factor in precipitating the stock market crash. This interpretation of the events of the late 1920s is shared by the most knowledgeable students of the period, including Keynes, Friedman and Schwartz, and other leading scholars of both the Depression era and today.

...There is little credible evidence of a bubble in the U.S. stock market before March 1928...yet, in part because of the workings of the gold standard, U.S. monetary policy had already turned exceptionally tight by late 1927... Tighter policy earlier would have brought the Depression on all the more quickly and sharply... The Federal Reserve went on to make a number of serious additional mistakes that deepened and extended the Great Depression of the 1930s. Besides trying to pop the stock market bubble, the Fed made little or no effort to protect the banking system from depositor runs and panics. Most seriously, it permitted a severe deflation in the price level, which drove real interest rates sky-high and greatly increased the pressure on debtors. A small compensation for the enormous tragedy of the Great Depression is that we learned some valuable lessons about central banking. It would be a shame if those lessons were to be forgotten."

Through the teachings of Keynes, Friedman, Bernanke and others we have been taught flawed analysis and educated in the wrong lessons from the terrible experience of the Great Depression. The doctrine of inflating Credit, while disregarding speculation and Bubble dynamics, is fraught with myriad dangers. And, well, we're now 20 months into Dr. Bernanke's - and global central bankers' - experimental "helicopter money" and "government printing press" assault on the Credit crisis. Not for a moment have I expected such overzealous inflationism to do anything other than exacerbate financial and economic fragility.

The financial world would be a safer place today had Trillions of additional dollars (and euros, yen, etc.) of liquidity not been unleashed upon the markets. After all, ultra-loose financial conditions accommodated 20 months of historic deficit spending in Greece, periphery Europe, here at home and all about. Massive government borrowing likely fomented heightened trading activity and speculation in sovereign Credit default swap markets around the world. Clearly, synchronized fiscal and monetary stimulus incited speculative excess throughout global securities markets.

The "inflationists" would argue that fiscal and monetary stimulus was essential for fostering U.S. economic recovery. A "liquidationist" ("anti-inflationist") would counter with the argument that the cost of Trillions of additional government debt and related marketplace distortions far outweigh what will prove ephemeral benefits. Attempts to avert system adjustment and restructuring - efforts to sustain the previous Bubble economy structure - will prove unsuccessful. This will in large part be because of the enormous amounts of ongoing Credit expansion and monetary profligacy required for such an endeavor. There are a host of issues related to the government throwing Trillions (of new "money") at a maladjusted economy. I have over the years broadly referred to these consequences as "Monetary Disorder." Some of these effects have made themselves conspicuous of late.

Reflating the stock market has been a key facet of government reflationary measures. Rising stock prices were instrumental in boosting household and business confidence. The revival of "animal spirits" in debt and equities markets was integral to much improved sentiment - and the advancement of a bullish consensus view that economic fundamentals were sound and the recovery on sound footing. And there's nothing like the cocktail of inflating markets, escalating confidence, and ultra-loose financial conditions to ensure the rapid emergence of speculative excess.

The financial world would be a safer place today had electronic "frequent trading" not proliferated throughout the government policy-induced stock market reflation. And financial stability was similarly not bolstered by near-zero rates having enticed over $1 TN of money market assets out to the global risk markets. The revival of bullish expectations, the revitalization of speculative excess and the unprecedented flow of finance into the riskier assets - in the face of latent financial and economic fragility - has set the stage for another round of financial tumult - further investor disappointment and disillusionment.

Perhaps "purge the rottenness out of the system" is too strong. But the financial world would be a safer place today had zealous government market intervention not bailed out the crisis-imperiled "leveraged speculating community". At one point yesterday, the Japanese yen was almost 6% higher against the dollar - and up a stunning 8% against the euro, Swedish krona and some other currencies. Those that had speculated on "carry trades" - say, borrowing in yen to finance leveraged long positions in euro-denominated Portuguese bonds - were crushed yesterday in what was likely a significant unwind of money-loosing trades.

The reemergence of "contagion" definitely makes the financial world an unstable and uncertain place in which to operate. A crisis in confidence in Greek debt led to dislocation in the market for Greece's Credit default swap (CDS) protection - that jumped to Portugal and then quickly engulfed European CDS and beyond. Dislocation in European bonds and CDS placed significant downward pressure on the euro and upward pressure on the dollar - in the process fostering general currency market instability. Most commodities (not gold!) sank, while the emerging markets came under heavy selling pressure. Global tumult incited a flight into bunds and Treasuries, causing additional havoc for myriad other "carry trades". Here at home, spreads between Treasury yields and higher-yielding debt instruments (i.e. MBS and corporate bonds) began to "blow out." In short order yesterday, the yen melted up, Treasuries melted up, risk spreads widened dramatically and 2008-style deleveraging returned in full force.

Throwing Trillions at a highly-speculative and dysfunctional global financial "system" has begun to present itself as a somewhat more conspicuous failure. The Greeks and Europeans are furious. And I doubt the ECB is too impressed right now with the "inflationist" prescription of monetizing euro debt issues. Here at home, confidence is shaken but not yet broken. The dollar is well-bid and yields are low, so things could definitely be worse. There should be, however, little doubt that the sequence of Goldman Sachs testimony, Greek riots, the eruption of contagion risk, and a quick 1,000 point market downdraft has reversed momentum away from Greed and firmly in the direction of Fear.