Below is an excerpt from a commentary originally posted at www.speculative-investor.com on 16th May, 2010.

Gold

A point we've made numerous times over the years is that gold is not primarily a play on a decline in the US dollar's foreign exchange value; it is a play on a general decline in monetary confidence.

Evidence in support of this view is the fact that the spectacular advance in the gold price that began during the second half of 1978 and ended in January of 1980 was accompanied by stability in the US dollar's value against most other major fiat currencies. The recent market action constitutes additional evidence.

The increase in the US$ gold price from its early-February correction low in the mid-$1000s to last week's high of $1250 has clearly been driven by plunging confidence in the euro, not the US$. The following chart comparison of the US$ gold price and the euro confirms that this is the case (the chart shows the US$ gold price gathering strength over the past few months as the euro accelerated downward against the US$).

As investors with substantial exposure to gold, one concern we have right now is that the surge in the US$ gold price and the accompanying plunge in the euro/US$ exchange rate has pushed the euro-denominated gold price (gold/euro) 16% above its 50-day moving average. Consequently, in euro terms gold is now more 'overbought' than it was at the intermediate-term peak of May-2006 and almost as 'overbought' as it was at the intermediate-term peak of February-2009. The situation is depicted below.

During the final 18 months of gold's long-term bull market the technical indicators we use to help us weigh risk against reward will stop working, because during this period gold will probably become extremely 'overbought' and then quickly double in price. Our opinion is that the end of the bull market is still a few years away and, therefore, that the traditional indicators should continue to be useful for a while, but there is a small -- although not insignificant -- possibility that a complete breakdown in the euro could send gold into 'blow-off' mode earlier than expected. This is why it is very important to maintain a sizeable 'core' gold position, despite the elevated level of gold/euro.

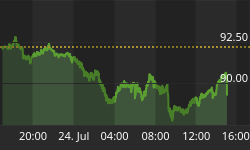

In US$ terms, gold would need to rise to at least 1300 to be at risk of experiencing something more serious than a routine short-term correction.

Silver

At this time gold is the only pure monetary commodity, which is why it has been the only major commodity to make new price highs in response to the burgeoning debt crisis. Silver, on the other hand, is part monetary commodity and part industrial commodity. This has meant that since late 2007 it has been subject to powerful countermanding forces. Specifically, it has been pushed upward by falling confidence in the official monetary system and pulled downward by the global economic downturn. The end result is the following chart, which shows that over the past two years silver has gone nowhere in a very interesting way.

At some point the rise in the monetary component of silver's overall demand should overwhelm the industrial component, propelling silver sharply higher in both gold and US$ terms. However, as things currently stand we think silver's position is more precarious than gold's. This is because it is butting up against considerable chart-based resistance (gold has no overhead resistance) and because the broad stock market has probably embarked on an intermediate-term decline (silver tends to weaken relative to gold when the stock market trends downward). Experienced options traders could therefore use SLV (silver ETF) January-2011 put options to partially hedge their exposure to gold- and silver-related investments.

We aren't offering a free trial subscription at this time, but free samples of our work (excerpts from our regular commentaries) can be viewed at: http://www.speculative-investor.com/new/freesamples.html.