Tuesday saw yet another huge rally off of deep intraday lows. The stock market, at one point down nearly 3%, ended the day flat on heavy volume of 1.8 billion shares. The VIX, at one time during the day around 44, ended at 34.61.

These are not staid, sedate, institutional-style flows we are seeing. The common thought is that the volume and the swings are coming courtesy of hedge fund business, and I am sure that is part of it. However, I believe there is probably also some significant hedging of equity derivatives that is driving flows. Dealers who are short options, either explicitly or embedded in deals, tried to buy them back where they could (pushing the VIX higher) or, if the price is too egregious, they are forced to delta hedge. That would cause buying on rallies and selling on declines. Now, there's no way for me to establish whether this is in fact happening, so it's 100% speculation on my part. But the volume and the large swings in both directions just smack to me of short-gamma activity.

Swings in nominal fixed-income markets are more muted - the market just seems to move one way! The June 10y Note contract (which will shortly be deliverable and so open interest is rolling to Sep) rallied 16/32nds with the 10y yield falling to 3.17%. This happened despite the furious rally in stocks and the large jump in Consumer Confidence to 63.3! Remember, though, that Consumer Confidence is neutral at 100, so this level means that consumers are now finally as confident as they were at the absolute depths of the last recession (see Chart below, source Bloomberg).

The current "optimism" would have been deep pessimism in 2003.

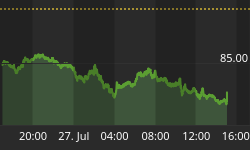

By contrast, the ABC Consumer Comfort Index has barely moved off its lows and is well below the 2003 levels (see Chart below, Source Bloomberg).

ABC Consumer Comfort still near the lows.

The difference in these two measures captures a key insight into the Conference Board's improvement. The former number includes a forward-looking expectations component, while the latter only measures current conditions. Indeed, if you compare the ABC figure to the Consumer Confidence "Present Situation" part of the index there is no discrepancy, as the chart below illustrates.

The improvement in confidence is all guesswork about the future.

This is less comforting to me than if the improvement was based on stuff that consumers were actually seeing, rather than what they were expecting to see. In a similar vein, the "Jobs Hard To Get" subindex, while improving slightly, hasn't improved significantly at all.

And yet, on financial news networks today there were discussions about the "risk of a double dip." A double dip? With Unemployment still well above 9%, shouldn't we resolve the first dip first? It is hard for me to see how a second "dip" from here would be distinguishable as a second recession given the current levels of resource underutilization. But it is consistent with what Consumer Confidence is saying - people are looking forward as if they expect the expansion (an organic expansion, not one based entirely on government spending, as the recent quarters have been) to begin any minute. It is the same optimism that brought stocks to a level that was discounting such an expansion, and it unfortunately means that confidence may well be due for a depressing mark-to-market unless growth miraculously starts to boom.

There are few signs of that, and despite the rally back today market conditions are still ugly. The 2011 TIPS got cheaper still today, with inflation swaps down further, and bid/offer spreads on TIPS grew back towards levels last seen in late 2008 and early 2009. For the Jan-2011 TIPS, an 8-month piece of paper, the bid/offer spread quoted on one dealer's screen was 14/32nds, for a grand total of $5mm size. The 10y TIPS are nearly 1 point wide bid/offer.

I don't know what tomorrow brings, market-wise, but I remain pretty happy to not be a part of it. I suspect we still have further to go on the downside. Trending markets have bounces/retracements, but when a bounce happens intraday, like it did today, that often helps delay a longer bounce. Economically speaking, we will get data on Wednesday from Durable Goods for April (Consensus: +1.4%, +0.5% ex-transportation) and New Home Sales for April (Consensus: 425k). In the market's current mood, I think these will be viewed as "old news" and not elicit a lasting reaction.