Many events of potentially vital significance to investors occurred virtually every day during last 4 weeks or so, weekends excepted.

But suppose, you, like most ordinary investors were busily attending your own day-to-day life, causing you to miss much of the detail of what was happening in May in the investment world, save a few headlines almost no one could miss.

Below is a brief synopsis of the month of May's events. It is highly unlikely that one will come across a month so chock full of daily happenings for quite a while. The key investment issues are highlighted. Some of these issues are discussed briefly below the listing.

One of my main purposes in presenting this list is to show, in my view, the near impossibility of trying to "figure out" what impact of the economic happenings and data will be when it comes to your investments, especially with regard to the relatively short term. The information is far too complex and even contradictory, with many events seemingly highly negative but others equally positive. That said, I believe there is considerable advantage to be gained in trying to figure out what this data may suggest for the longer term.

May 3 US manufacturing data show the strongest growth in nearly 6 years.

May 4 International stock and bond markets sagged, apparently rejecting the days' old deal to bail out Greece that was intended to stop the European debt crisis from spreading.

May 5 Euro drop reaches a 14 month low against dollar in reaction to the European debt crisis; bond yields continue soaring in Western Europe.

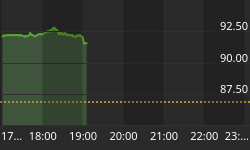

May 6 Dow drops 1000 points intraday, biggest ever, mostly in minutes, but ends the day down "only" 348 points.

May 7 US adds jobs at a pace not seen since before the recession, but the unemployment rate rose to 9.9%.

May 10 The European Union announces a $955 billion plan to try to avert the debt crisis.

May 11 A new government is formed in Britain which must tackle a huge deficit with a divided Parliament.

May 12 Gold, often viewed as an inflation signal, rises to a record $1243 an ounce.

May 13 Major US stock indices failed to hold levels considered important by technical market analysis, suggesting to adherents that the bull market may be changing course: The Dow started the day at 10897; by the end of the month, it was down to 10137.

May 14 California, often a forerunner of trends, reported an increased budget deficit of $19 billion, and draconian cuts to deal with it.

May 17 General Motors reported a quarterly profit, its first in 3 years, as compared to last year's $6 billion 1st qtr. loss. (Many had written off the company as dead and unworthy of government help.)

May 18 Oil is still leaking in the Gulf, threatening an ecosystem disaster, and prospects for new offshore drilling are in danger, but the price registers a "bear" territory drop of 20%.

May 19 US inflation is reported at a 44 year low. Also, the Euro reaches a 4 yr. low vs the dollar, and down 20% from its recent high in Nov.

May 20 US Dow stocks fell into the first 10% correction in over 14 months.

May 21 Market volatility (VIX index) reaches it highest point since early 2009.

May 24 Junk bond market plummets to lowest level since Dec. 2008.

May 25 Yields on the 10 and 30 yr. US treasury bonds drop to their lowest level since last year, and the two yr., the lowest level ever. Also, many international stock markets fall to their lowest levels of the year.

May 26 Durable goods orders rise to biggest annual gain since 1976.

May 27 30 yr. fixed mortgage rates drop to 4.78%; adjustable mortgages are at a 5 1/2 yr. low of 3.95%.

May 28 Dow ends month with worst percentage drop for May (7.9%) since 1940. S&P 500 and NASDAQ drop an even greater percentage for the month.

Note: Even with our seemingly comprehensive listing of newsworthy items, it is likely that we have omitted some addition items of strong importance. As some might put it, May was one "piece of work."

One's reaction upon reading the list (assuming one's eyes' don't glaze over after reading just a few items) might be that of troubling doubts about some of one's investments, especially stocks, ranging all the way to outright fear. Or, there might be a reaction similar to "I feel I've been through this all before," resignation, or even apathy to what one has little ability to clearly comprehend or analyze. Of course, we might express this latter reaction in more constructive terms as a welling up of stoicism, patience, and a renewed gritting of the teeth to "stay the course," or even thoughts as how to possibly profit from the "May-hem."

One's course of action, if any, might, then depend of which of the above reactions one experiences.

Suppose, though, that someone truly had missed most or all of this investment-related news. If they then exposed themselves to various sources of the latest advice on investing, I have observed that somewhere close to half of the advice would be akin to "buying opportunity for stocks" vs. "time to trim down," with the same schism with regard to bonds and cash.

What this suggests is that not even the experts can ferret out the "true" meaning of May's events as far as your investments are concerned. As some might express it, there is even more uncertainty in the markets than is usually the case.

For what it's worth, here is our brief take on some these events and data:

-

The 10% correction was more of a good happening than a bad one. A correction was needed for reasons that are hard to explain, but essentially to restore a greater degree of value and to allow investors who want to buy with the incentive to do so. (We had told investors to expect it and possibly defer purchases in anticipation.)

-

The European debt crisis probably has nearly as many good aspects for US investors as bad. These include a) helping to keep Fed controlled interest rates on hold; b) enabling European countries to export their wares more cheaply into the US (weak Euro) which will help boost their weak economies and also to keep US inflation low; c) creating a "safehaven" for US bonds among world investors; and d) bringing governments (hopefully including the US) a step closer to attacking out of control budget deficits.

-

While many US data releases (especially manufacturing) are showing strong growth, they reflect relative change from the extreme lows of a year ago. They are still way below pre-recession levels on an absolute basis.

-

In spite of highly loose monetary and stimulative fiscal policy, inflation is nowhere on the horizon.

-

No one can truly say what the effect of the Gulf oil spill will be on the US economy. However, what might be implied is that the drilling and extracting of offshore oil will become less likely to occur and more expensive when it does. This will likely cause oil to become even more costly in the future as well as advancing even further the case for alternative sources of energy.

-

While there is no assurance that stocks won't keep falling for a while longer, and that volatility will go away soon, the US equity market continues to look like a decent long-term investment. However, diversified foreign equity markets as well as international bonds appear to have lost a fair amount of appeal because one faces the challenge of both weak European growth and further potential currency losses which present strong headwinds to US investors.

-

US Treasury bond yields have returned to unattractively low levels. Other types of US bonds appear to show somewhat better prospects. Cash and equivalents remain essentially useless as an investment, but only as a storing place for upcoming cash flows or emergency use.