Stocks launched higher near the close of trading, pushing the market back to an unchanged close after trading slightly lower for most of the day. The second consecutive day of nearly-unchanged finishes, combined with the fact of five consecutive low-volume trading days, would tend to suggest indecision and argue that a reversal lower may be imminent. However, I am a bit cautious about that technical interpretation in this case, for two reasons. First, the entirety of both ranges was above the previous range high on June 3rd; thus, these last two days may represent quiet consolidation of gains and non-rejection of these prices. Second, the market today managed the unchanged feat despite some pretty weak data. (As an aside, the Note contract gained 21/32nds and the 10y yield fell to 3.19%.)

Economists had forecast Initial claims to decline, like they forecast every week; instead, however, Claims rose to 472k. Again, much to the consternation of economists, the economy isn't spontaneously improving and there is no evidence at this point to suggest a self-sustaining economic expansion is underway. The Initial Claims rise was underscored by a drop in the "Employment" subcomponent of the Philly Fed Index (which itself surprised by declining to 8.0) to -1.5, indicating contracting employment (albeit only marginally).

These do not indicate that the economy is collapsing anew, but they do highlight the fact that (as I just said) the scheduled improvement is not taking place. This is bad news for equities, whose valuations are predicated on the notion that they are discounting the first few years of the expansion. If the expansion isn't expanding yet, then we've no business being at these levels.

So the marginally improving technical picture I alluded to above no means indicates I am bullish on stocks for the medium-term. The risk of a near-term collapse has receded, and I can imagine some modest incremental gains. More likely, we have earned some summertime chop while we wait for more data to clarify whether the possession arrow is pointed to the bulls or bears right now.

I haven't mentioned CPI yet. That figure came in slightly above expectations. With rounding, the year/year headline fell to 2.0% (next month, it will fall to around 1% since the June '09 jump will drop out of the calculation), and core CPI remained unchanged at 0.9%. Moreover, core CPI ex-housing stayed at 2.2%. Regular readers will know that I believe it is not only legitimate, but almost a requirement, to remove housing from the index at the moment, since that is a sector of the economy that we know to be unwinding a bubble and, therefore, is unlikely to reflect the broad pricing trends in the economy. Clearly, the pressure on rents is helping individuals; but the reason we exclude certain items is so we can get a better reading on the underlying trend and, in this unusual case, housing is both (a) behaving idiosyncratically and (b) large enough to affect the overall reading.

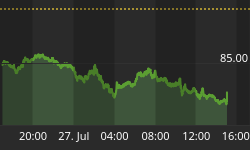

Even with housing included, however, core inflation almost ticked up to 1% year/year as core was just a snick higher than expected. This really doesn't have a big econometric significance, since the difference is well within the variance of the indicator, but it does have some psychological significance to buyers of inflation-indexed securities. These folks have been under some pressure after the outright decline in core inflation in January and the near-zero performance since then. Actually, the 0.12% month/month advance in core inflation was the highest since last October! Not much to write home about, unless you tend to write home about wiggles in core CPI, but a beleaguered TIPS owner might see something bottom-like in the following chart (Source: Bloomberg):

If you look really hard, you might imagine a bottom in core inflation

(To be clear, I don't think we have quite seen the bottom yet, but it is approaching. My models call for a slight further dip into late Q3/early Q4.)

One quick word here about CPI as a number. I don't feel like I can ever say often enough that despite all of the conspiracy theories you will read about on the Web about the CPI, it actually is a pretty good measure of what it is supposed to measure, and does a reasonable job of measuring the rise in the general price level (to see an explanation of why it might not feel like CPI is doing its job, see my column here).

Some people, however, tell me they avoid TIPS because they are pay based on a "made up" or "manipulated" government number. I want to tell you that is a bad idea, and you don't even have to believe that CPI is correct for it to be a bad idea. All you have to do is believe that the market is not completely fooled by the number.

If CPI wasn't a reasonable approximation of inflation, then as I point out in that other column your standard of living over the last 20 years would have plummeted. Compounding even a small error would be devastating, never mind the huge errors that people claim CPI represents. But suppose that CPI was in fact mis-measuring inflation by, say, 3%. Suppose CPI claimed inflation was 2% when in fact it was really 5%.

If that is the case, then if markets are efficient at all TIPS will be priced to incorporate the correct level of inflation. Consider how nominal interest rates are set by the market, for starters. If I am going to lend you money for 10 years, I need to first determine what real return I need on my money in order to entice me to lend it to you rather than to consume it myself. To that, I then add an inflation premium to reflect my expectation of the decline in purchasing power over that period (and, perhaps, a risk premium). This is Fisher's construction (1+nominal) ≡(1+real)(1+expected inflation)(1+risk premium).

TIPS replace the (1+expected inflation) part with actual realized inflation over the holding period, so their yield is simply the real return demanded on money.

But what if I, as a buyer of TIPS, believe inflation to actually be mis-stated by 3%? Then obviously, I will insist on a higher real yield of TIPS by about 3%. If my required real return is 2%, I will require that TIPS be priced to yield 5%. That way, I will actually receive 5% + fake inflation; since fake inflation=true inflation-3%, this means I will get 5% + (true inflation - 3%) = 2% + true inflation. So if the CPI is bogus, then the bonds in equilibrium should be priced to reflect the real yield that investors need if they are to actually realize the true real yield they require. In fact, in some emerging economies where the official inflation figures are indeed bogus the inflation-linked bonds linked to the official index are priced "cheap" to those that are linked to an independent index. That TIPS are not priced this way suggests that most investors believe CPI is correct, or close enough.

Now, perhaps you might retort that these are all dumb institutional investors who have money to invest and no place to put it, so they have to invest this way. But take it a bit further: if that is the case, then other issuers besides the U.S. government should be itching to issue bonds linked to inflation that look really cheap but in fact are not. If TIPS are trading at 2%, and I issue an inflation-linked bond at 3.5%, then it looks like I'm 150bps over Treasuries and if I am a quality borrower it should be snapped up by the same dumb investors...meanwhile, however, I know that I'm actually issuing debt at 3.5%-3% "fake spread" = 0.5% (true) real yield and I know I can invest this money in projects to increase the value of my firm.

Clearly, there is no such deluge of issuers; if there were then it would tend to push TIPS toward that equilibrium price that reflects the amount by which CPI is "wrong."

So economists, inflation experts, investors, and issuers all think the CPI is pretty close to right. Conspiracy theorists and the math-challenged feel otherwise. There are plenty of ways that we can improve economic data, which are after all merely imperfect measures of the underlying reality. But I believe CPI has been very well constructed and is one of the government-produced numbers that we can actually feel reasonably comfortable with.