As long as US economic data shows fresh round of deterioration, and the Eurozone is able to supress event risk on the sovereign front, the Japanese yen shall cotinue to draw the lion's share of risk-aversion flows away from the USD. But let's first go over the USD's recent decline before further dissecting the yen flows.

The 7% decline in the USD's trade-weighted index from its June highs has evolved from stabilizing global equities to broadening weakness in the US data front. The resulting decline in US bond yields has accelerated the USD sell-off to the extent of eroding US yield differentials relative to EUR, GBP and JPY. The broad downgrade of the US growth outlook by the FOMC shuts the door on any remaining form of policy tightening this year, thereby, exacerbating the decline in yields. In fact, the minutes of the FOMC meeting allowed for renewed easing in if the outlook were to worsen appreciably.

The chart below shows the spread between German and US 10-year yields (GE minus US) has improved to -0.31%, the highest since October 2009. A decent Spanish bond auction and eroding liquidity concerns in the Eurozone have helped accelerate the euros rebound. Renewed declines in US new home sales, payrolls and consumer confidence are tipping the balance into a possible double dip recession. US 10-year yields have also fallen relative to their UK and Japanese counterparts, nearing their worst levels in 12 months.

EURUSD broke above $1.29 but may fail to close the week above the 100-DAY MA, which would have been the 1st positive cross this year. Euro remains propped with the potential of extending towards $1.3130. A close below $1.26 would be required next week to fuel hopes for a prompt USD rebound. Otherwise, $1.3130 is next in the cards.

EUR diverged from GBP as EURGBP broke above the key 0.84 preliminary resistance, eyeing 0.8490. I maintain my negative bias on EURGBP considering widespread sovereign questions in the Eurozone and the contrasting inflationary picture between the above-target 3.2% UK CPI and the Eurozones 1.4%.

Yen Does it Again In July 7th I wrote The combination of US earnings season with European stress tests will likely stand in the way of equities regaining their April highs, while the expiration of US jobless benefits and homebuyer credits could speed the way for the downside. Such a scenario paves the way for deteriorating risk trade, with the JPY most apt to assume the role of risk-aversion beneficiary. Many observers are loath to mull USDJPY below the mid 80s, citing opposition from Tokyo. But with the USD part of USDJPY equation remaining vulnerable to US data uncertainty and the JPY part gaining from the aforementioned red flags to global growth and risk appetite, the implications for sub 85 USDJPY are becoming increasingly suggestive. And with global bond yields caving in to disinflationary pressures and growth concerns, Japanese capital will turn away from yield appetite to safety appetite.

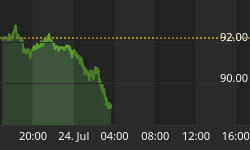

Today, US 10 yr yields drop below 3.00%. USDJPY knives below yesterdays 87.20 target, now eyeing 85.80 as the deteriorating stochastics call for extended JPY strength. The chart below shows the double bottom in the VIX may rebound towards 34-35, which case USDJPY will have a valid grounds for retesting the 84.80 lows.

My original analysis from October 2008 explained how USDJPY would continue to break to new lows as long as the case for a Fed tightening remained weak. With the June FOMC minutes showing the first economic in nearly a year, and bond yields under pressure, the door for a 2010 tightening has been firmly shut.

Dj-Vu from May 21st equities made a late session rally on news that Goldman Sachs would settle its lawsuit with the SEC, but news of Googles earning miss was not ignored by Asian markets. Nikkei-225 fell 2.9% on what is said to be fears of prolonged yen strength.

Wednesdays VIDEO MARKET ANALYSIS explaining the rationale for choosing GBPJPY and EURJPY

For more frequent FX & Commodity calls & analysis, follow me on Twitter.com/alaidi