The recent hallucinatory rally, triggered by positive earnings spin and the wonderful news that the European banking system is really just fine despite the fact that none of the banks seems to think the other banks are fine, has puttered a bit over the last couple of days. While today's -0.7% setback is far from catastrophic, neither is it awe-inspiring as the market drifts from levels that would have signaled a technical triumph. The 10y yield is still below 3%. The VIX is off its recent lows, which is the only reason it doesn't seem like lazy summer trading. 24.25 is a pretty high level for the VIX, historically. Some folks are apparently still nervous.

Soft durable goods orders (-1.0%, versus +1.0% expectations) and durables ex-transportation (-0.6%) may have contributed a little bit to the nervousness, although non-defense capital goods ex-aircraft was positive following a positive spike last month. (And people criticize the leaving out of food and energy from CPI! What about taking out all defense, all non-capital goods, and all aircraft!? There is a reason for it, though; that subcomponent of durables is the most correlated with overall growth, although "most correlated" still isn't very good).

This news followed the mixed news on Tuesday. The rise in the Case-Shiller Home Price Index put the year-on-year rise at 4.6%, the fastest pace in four years and unmitigated good news (unless you worry about inflation). But Consumer Confidence slumped again, this time to 50.4, and the "Jobs Hard To Get" subcomponent rose to 45.8. Consumer confidence is a decent co-incident indicator. If people are losing confidence, it tends to confirm all of these other tepid readings we are seeing and supports the notion of weakness in the job market. Double-dip? Too early for an official pronouncement, but a stall at this point in the recovery - if it was in fact a recovery, which I dispute - is fairly unusual. At some point the economy, to paraphrase "Red" Redding from The Shawshank Redemption, needs to get busy living, or get busy dying.

.

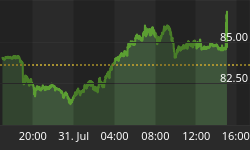

In other interesting news today, Visa Inc. reported stronger-than-expected earnings. The spin in the financial press is that "more consumers paid with plastic," and the number of processed transactions rose 14% according to a Bloomberg article. But at the same time, we know that revolving credit is declining and has been declining for 20 months now (see Chart below). How do we square this?

Revolving credit is declining hard. But VISA is doing just fine. Why?

This might suggest that more people are using credit cards to smooth over short-term bumps in cash flow, but diligently paying down balances so that the turnover of balances is rising. This would be good news for VISA, and for the economy, although the higher velocity it implies would be bad news for inflation.

This may not be a ridiculous interpretation. In May we found that consumer defaults on credit cards - which do not happen until the account is at least six months behind - rose to an all-time record of 9.14% (according to the S&P/Experian Consumer Credit Default Indices, which date only to 2004 - see the story here) before declining to 8.81% in June.

If revolving credit is declining because responsible people are diligently paying off balances, leaving the irresponsible people to default, it could explain the hesitancy of the default ratio to fall very much - the smaller pool of outstanding balances would be lower quality, consisting of more people who were not paying off their cards because they can't pay off their cards.

Meanwhile auto loan defaults have been declining...because less credit is being extended to weak borrowers. Mortgage loan defaults have fallen...because fewer mortgages are being made to bad borrowers and the worst mortgages have already defaulted. In the case of non-revolving credit such as mortgage and auto loans, there is little incentive for a good credit to pay down early. They are borrowing money at much lower rates than they are on credit cards, and once they pay it off they can't run the balance back up (indeed, credit is still very tight; you may not be able to get another home loan!). As a consequence, the quality of these pools should tend to improve first, but that also doesn't tell us a lot about whether people are getting new-found responsibility.

The early rise in delinquencies for subprime, and then Alt-A and Prime loans, and then every other kind of loan, were the signals that all was not right in the economy (and in these pockets of the credit markets). The improvement in revolving credit turnover, combined with a decline (albeit for a single month) in credit card delinquency rates, may be an early sign of something good happening in the economy. Not great, mind you, but a sign that attitudes toward personal credit are returning to more-rational standards. We have a long way to go on this score, but the vector is finally pointing the right way. Maybe.

Tomorrow, the main data is Initial Claims (Consensus: 460k), which as you will recall has been quite volatile lately because of the GM non-shutdown. The turbulence continues to imply we shouldn't rely too much on this release, although every week that goes by improves the quality somewhat.