The stock market since the May "flash crash" and early July cycle low has been a trading range affair characterized by alternations between high and low volatility levels, or what pundits have taken to calling "volatile volatility." As Steven Sears in his Barron's column of July 26 pointed out, "The back-and-forth action is just the latest reminder that volatile volatility is a central fact of the 2010 market." After being spoiled by last year's extremely low volatility market, participants are shell-shocked at the heightened levels of volatility in recent months.

The cyclical context for this year's volatility can be found in a Kress Cycle pattern characterized by crossing currents: on the one hand the 4-year cycle due to bottom in late September is an obstacle against a runaway type market like we saw in 2009; on the other hand the 6-year cycle is still in its ascending phase and is acting as a support against the resumption of a crisis-type market like we saw in 2008.

Compounding the volatility factor more recently has been the crosscurrents between the rising short-term cycle (the one that bottomed in early July) and the declining short-term cycle that's bottoming right now. Once the latest cycle bottoms we should see less downside pressure on stocks heading into August. Yet there remains another volatility factor to be considered as we head closer to September, and that's the upcoming 4-year cycle bottom. The bottom line is that we haven't seen the last of Mr. Volatility, at least not until the fourth quarter

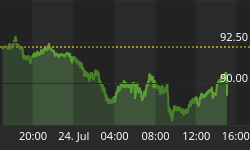

Here's what the year-to-date Volatility Index (VIX) looks like. As you can see, VIX is well off its highs from earlier this spring but still well above its lows from January-April. VIX is currently still below the dominant immediate-term 15-day moving average, but we could witness a short, brief spike above it before the short-term cycle bottom is in within the next couple of days.

Despite the increased "volatile volatility" on an interim basis, the financial recovery remains on a sound footing and it's unlikely we'll witness anything like what we saw in May with the panic sell-off anytime soon. With this in mind, I want to emphasize that we've arrived at a point in the financial recovery cycle in which we'll want to place greater emphasis on the 30/60/90-day moving averages as trend evaluators and less emphasis on the 15-day MA. That means on all current and future trading positions we'll be making greater allowance for volatility by using either the 30-day, 60-day, or, on some occasions, the 90-day MA as our rolling stop loss guide. And we'll begin with a recommended trading position review later in tonight's report.

Everyone wants to know what the next "big thing" will be in the financial market. While many are diligently searching for the next potential bubble mania or hot trend, it's my belief that we won't be seeing anything approaching a bubble or runaway trend in any of the major sectors anytime soon. Instead, a slow grinding trend is more likely.

Symptomatic (or perhaps causal?) of the volatile volatility this year has been the conflict between the advocates of government stimulus and those who favor fiscal austerity policies. Conservatism and fiscal austerity are the new buzzwords in the more right-leaning members of the financial press, while the left-leaning segment of the press favors more stimulus. It's hard sometimes to discern which of these two major factions has the upper hand, though the austerity advocates enjoys a much bigger and more sympathetic audience than it did before the credit crisis. Just witness these headlines from the latest issues of the leading financial magazines: "As the world slides toward a double dip, pressure for fiscal austerity increases," "Consumer confidence falls again," "Doubts about new regulation and the fate of the economy have corporations playing it safe," "The rush to hedge against black swan events, "Wall Street's hottest new product is fear."

Then there was the July 4 issue of Businesssweek magazine which contained the following elongated front cover headline: "The Greek people are angry. While young anarchists wielding Molotov cocktails get most of the attention, far greater numbers stew in tiny apartments, livid at their leaders for capitulating to the markets and saddling them with a life-changing burden. Here's the thing: Their leaders are right. And in misery lies hope." That such a stunning endorsement of austerity could be read on a major U.S. news publication can only be chalked up to the life-changing chaos of the credit crisis.

The above sampling of headline sentiment is but a small testament to the residual fear that is serving to bolster the financial marketplace in the wake of the credit crisis. It might be argued that revolutionary events like the credit crisis would naturally be expected to engender a profound shift in personal philosophy. The two years since the credit crisis has indeed witnessed a sea-change in philosophy, including the way that most people view the economy and financial markets. The dominant philosophy of the years B.C.C. (before the credit crisis) was one of financial profligacy and of unfettered confidence in Keynesian economic policy. It was a widely accepted belief that government stimulus was the answer to any financial market downturn, no matter how severe, and the word "austerity" was virtually unknown to those outside the Third World. Yet today, true to reactionary human nature, the ones who deplored austerity in favor of financial liberality are now embracing the former while rejecting the latter.

It's also a sign of the times that while there is a growing populist leaning toward fiscal austerity, governments, most notably the U.S., still favor fiscal stimulus and are still mainly steered by 20th century Keynesian policy. This is one reason why "volatile volatility" will continue to be a theme at least in the foreseeable future. Conflict between competing philosophies creates friction and lends itself toward volatility without giving either side a decisive advantage over the other. Hence the tendency toward trading range volatility of the sort we've witness in the past year and as seen in the Volatility Index (VIX) chart shown above.

Another reason for increased volatility is the uncertainty surrounding this year's upcoming Congressional elections. Add in the uncertainty surrounding the government's proposals to raise corporate taxes on foreign earnings, incomplete free-trade deals with major U.S. trading partners and the recent financial overhaul and we have the fundamental backdrop for volatility to persist until at least the 4-year cycle bottoms or until the political situation clears up, whichever occurs first.

Years in which the 4-year cycle is bottoming and a Congressional election takes place almost always witness sizable volatility spikes, e.g. 1994, 1998, 2002 and 2006. This year is proving to be no different. The combination of cycle pressure with political uncertainty is apparently sufficient enough reason for the reappearance of volatility. The case that most closely corresponds to this year would be 1994. It was in that year that a newly elected Democrat president was faced with the likelihood of a Congressional changing of the guard in the November elections, which is exactly what ended up happening. The year 1994 also witness a simultaneous bottom in the 4-year and 10-year cycles, which conspired to keep stock prices below their highs from earlier in the year. The year 1994 also saw a "flash crash" in the spring of the year with a double bottom price low in the NASDAQ 100 Index at the end of June (sound vaguely familiar?)

On a related note, one of the trends that will most likely become increasingly dominant is the focus on include industry groups that have a history of relative stability in periods of extended market uncertainty, like utilities and pharmaceuticals, plus some high-yield bond and income funds. Already these investments are making a bit of a splash among smart money investors and some of them have developed a measure of forward momentum unusual for conservative investment vehicles.

A trend that savvy investors are embracing this year is to focus on high-yield stocks of companies with strong earnings growth and relative price strength as a way of hedging against market volatility. As John Hussman of Hussman Funds said recently when describing his fund family's allocation strategy, "We also like dividend yields, which can help reduce the volatility of individual holdings - provided those dividends are well covered by stable earnings." He advises investors to seek companies that have a long history of stability even in the face of economic downturns.

Four-year cycle bottom/election years also tend to favor a trading range strategy, namely buying when the price oscillators reach decisively "oversold" levels and when stocks pull back to benchmark price support levels, then selling when the oscillators read "overbought" and prices hit key resistance levels. Until the intermediate-term hi-lo momentum (HILMO) indicators become synchronized again on the upside (see chart below), we'll need to be wary of the potential for continued volatility increases at times between now and the 4-year cycle bottom scheduled for late September this year.

The HILMO chart featured in the latest newsletter shows that the forces of upward and downward momentum across the interim time frames are rather evenly balanced, which explains the stock market's lateral trading bias of the last several weeks. My reading of the short-term HILMO index (discussed in a recent newsletter) is that market short-term forward momentum should be strong enough to counteract the downward bias of two of the momentum indicators shown in the HILMO chart below.

Gold and the precious metal mining stocks always reflect the heightened volatility characteristic of 4-year cycle bottom years and this year has proven to be no exception. The historical pattern is for gold and silver stocks to rally in August and sometimes into September when coming off a correction low, as occurred in 1982, 1986, 1990, 1994 and 2002 during previous 4-year cycle bottoms. The reason for this is that as the actual 4-year cycle low approaches, the increase in uncertainty it breeds in financial markets typically translates into a flight to the perceived safety of gold and mining equities which reaches an apex just before the final "hard down" phase of the 4-year cycle causes a decline in asset prices across the board. The chart of the XAU from 2002 is a typical pattern of the 4-year cycle volatility action in the gold stocks.

Technical Analysis

Technical analysis is one of the most important and powerful tools for capturing gains in the stock market. When applied properly it can simplify the stock picking procedure, making it easier to identify the stocks that have the biggest potential for capital appreciation. Technical analysis is also of tremendous benefit in capital preservation as it enables the investor to identify the best price levels for setting stop-loss or exit points as well as identifying the best entry points for initiating a trading position.

Technical analysis is also helpful to investors in their search for the stocks and industry groups with the highest potential for achieving gains. By learning to properly read the charts and technical indicators of actively traded stocks, an investor who relies mainly on fundamental analysis will be able to more efficiently focus his time in researching the most promising company's stocks while eliminating those which lack appreciation potential. In this regard, technical analysis is a most remarkable tool to use in conjunction with conventional fundamental research.

Several years ago I decided to write a book which distilled technical analysis to its essence. The book explains in easy-to-understand language the basics of chart reading. It also explains in simplified terms how to use the most useful of the technical indicators when analyzing stock charts. The aptly titled book, "Technical Analysis Simplified," is still in print and has helped many traders and investors improve their performance in the stock market.

The book is now available for sale at: http://www.clifdroke.com/books/book03.mgi