Summary of Index Daily Closings for Week Ending July 30, 2004

| Date | DJIA | Transports | S&P | NASDAQ | Jun 30 Yr Treas Bonds |

| July 26 | 9961.92 | 3048.60 | 1084.07 | 1839.02 | 108^06 |

| July 27 | 10085.14 | 3063.51 | 1094.83 | 1869.10 | 106^23 |

| July 28 | 10117.07 | 3086.33 | 1095.42 | 1858.26 | 106^26 |

| July 29 | 10129.24 | 3129.64 | 1100.43 | 1881.06 | 106^31 |

| July 30 | 10139.71 | 3111.64 | 1101.71 | 1887.33 | 108^07 |

| SHORT TERM FORECAST (Next Two Weeks) | ||||

| TREND | PROBABILITY | Legend | ||

| Substantial Rise | Low | |||

| Market Rise | High | Very High | 80% | |

| Sideways | Medium | High | 60% | |

| Market Decline | Medium | Medium | 40% | |

| Substantial Decline | Medium | Low | 20% | |

| Very Low Under | 20% | |||

| INTERMEDIATE TERM FORECAST (Next 12 Weeks) | ||||

| TREND | PROBABILITY | Substantial | 800 points+ (DJIA) | |

| Substantial Rise | Low | Market Move | 200 to 800 points (DJIA) | |

| Market Rise | Medium | Sideways | Up or Down 200 (DJIA) | |

| Sideways | Medium | |||

| Market Decline | High | |||

| Substantial Decline | High | |||

This week the Dow Jones Industrial Average closed up 177.48 after falling to 9,913.92 on Monday, the low for the move since June 25th's intraday top. This looks like the start of a rally that should work off oversold conditions in most major equity markets over the next week or two before turning down again in earnest. We expect the pattern of declining tops and bottoms to continue.

Trannies bounced off the upper boundary of their short-term downward sloping trend-channel, and look to be forming a Bearish Head & Shoulder Top pattern. They sit above their rising 50 and 200 day moving averages and remain within their intermediate-term rising trend-channel. The chart appears on page 6.

Small caps, the Russell 2000, are oversold, but the long-term pattern is an ominous Rounded Bearish Top. Like the Dow Industrials, their 50 day and 200 day moving averages have converged, with prices below but headed back toward them. The convergence point should provide formidable resistance, but a small non-decisive upside break is not out of the question - prices will rise enough to get the averages into overbought territory. This chart is also on page 6.

| Equities Markets Technical Indicator Index (TII) ™ | ||||

| Week Ended | Short Term Index | Intermediate Term Index | ||

| Mar 26, 2004 | 73.00 | (38.35) | Scale | |

| Apr 2, 2004 | (3.00) | (35.61) | ||

| Apr 16, 2004 | (43.00) | (29.90) | (100) to +100 | |

| Apr 23, 2004 | 94.00 | (22.69) | ||

| Apr 30, 2004 | (33.25) | (34.88) | (Negative) Bearish | |

| May 7, 2004 | (28.75) | (47.75) | Positive Bullish | |

| May 14, 2004 | (25.75) | (66.45) | ||

| May 21, 2004 | 22.00 | (67.23) | ||

| May 28, 2004 | ( 3.50) | (48.48) | ||

| June 4, 2004 | (55.75) | (34.07) | ||

| June 11, 2004 | (77.75) | (25.92) | ||

| June 18, 2004 | (40.25) | (31.17) | ||

| June 25, 2004 | (34.00) | (26.10) | ||

| July 2, 2004 | (41.50) | (27.64) | ||

| July 9, 2004 | (32.50) | (30.21) | ||

| July 16, 2004 | (33.75) | (41.99) | ||

| July 23, 2004 | (59.00) | (49.98) | ||

| July 30, 2004 | 46.25 | (52.18) | ||

This week the Short-term Technical Indicator Index comes in at positive 46.25, indicating markets should rise. This indicator is a useful predictor of equity market moves over the next two weeks, both as to direction and to a lesser extent strength of move. For example, readings near zero indicate narrow sideways moves are probable. Readings closer to +/-100 indicate with a higher degree of confidence that an impulsive move up or down is likely over the short run. Market conditions can change on a dime, as unforeseen disasters can occur, or the Plunge Protection Team can come in and temporarily stop market slides, so it may be unwise to trade off this weekly measured indicator.

The Intermediate-term Technical Indicator Index is useful for monitoring what's over the horizon - over the next twelve weeks. It serves as an early warning system for unforeseen trend changes of considerable magnitude. This week the Intermediate-term TII comes in at negative (52.18).

On the next page we present Analogs of prior crashes versus the current price pattern, updated as of July 29, 2004. The first chart compares the 2000 to 2004 Bear Market with the average of the first seven years of the past two secular Bear Markets, 1929 through 1936, and 1968 through 1975. The correlation is pretty strong, at times almost tick for tick. The timing of ups and downs is very close, only the extent of moves differing a bit. But for the most part, when the past's prices fell, the current period's prices declined and when the past rallied, the current's prices kicked higher. Turning points are remarkably similar. If this analog holds up, a crash is imminent, has perhaps already started, with fullthrottle deceleration due next.

The second Analog compares the topping pattern of 2002's pre-crash price pattern with today's. They are remarkably similar. Both patterns hit some sort of high or low on January 28th (+/- 1 day) and again on May 17th. 2002's crash started on June 18th, while June 23rd 2004 was the top of truncated wave 5 up of C up of primary degree 2 up in Elliott Wave parlance. Should this analog hold up, keep in mind that 2002's crash was over 2000 points and lasted two months. It contained a few minor rallies - short covering events that served the Bearish purpose of working off deeply oversold conditions (like we face this week) - but the fall was essentially vertical. Analogs are fun to consider, but sooner or later they all break apart. Still, what they do capture is a common investor herd psychology that seems to lead to similar price behavior. The ride up to today's peak took longer than 2002's, and extended from a lower initial starting point than those of the past. Therefore it is not illogical to expect that the topping pattern might stretch out a little longer than topping patterns of the past, perhaps a month or so longer since the current move is of a slightly larger scale. That would mean the start of this year's crash could occur as late as August or September and yet remain true to the basic pattern of past crashes.

We cannot lose sight of where we are as the equity markets start another rally phase. The above chart has shown remarkable accuracy in predicting significant sell-offs over the past six years. Every time the SPX/VIX ratio rose above 68.00, a Crash occurred shortly thereafter. Ratios over 68.00 indicate tops, not bases from which Bull markets can run. When the recent Bear Market rally started in March of 2003, this ratio was below 30. Today it stands at 72. The rally over the next week or two is nothing more than an oversold bounce that will lead to a significant decline. More directly, this chart is telling us that a multi-month Stock Market Crash is right around the bend. The longer this topping pattern takes, the harder this market will fall. What is uncertain is when it will start. Could be August; could be October. But it's coming.

The Dow Industrials have completed minute degree wave 1 down of a 5 wave stair-step down sequence that will become minor degree wave 1 down of primary degree wave 3 down (that could last until 2006) in Elliott Wave parlance. The move completed Monday, intraday, at 9913.92, a little sooner and shallower than our Short-term Technical Indicator Index expected this week. Since then we have seen a micro degree wave "a" move up of an a-b-c minute degree wave 2 up that should last about another week or two, three at the outside, and take prices to a max of 10,364, the 78.6 percent retrace of minute degree wave 1 down, and the point where prices would reach the upper boundary of the declining intermediate trend-channel (magenta) since February 2004. Then a sharp decline wave 3.

The rally from Tuesday has been on declining volume, adding to the evidence that it is corrective, not the start of a dramatic impulsive move higher. The Relative Strength Indicator has moved back into neutral territory rather quickly, and it shouldn't take a great deal more upside price action to reach overbought territory, which is the purpose of this rally - to set the table for the next major leg down in the Bear decline. The MACD turned up before reaching panic selling levels, also adding to the preponderance of evidence that a sustained Bull move up is not in the cards at this time. Those kind of rallies come after heavy sell-offs where supply throws in the towel. Hasn't happened.

Like the major index averages, Dow component Hewlett Packard Co. (HPQ) - shown above courtesy of www.stockcharts.com - looks ready to decline sharply once a small countertrend rally finishes over the next week or two. This stock has formed a Bearish Head & Shoulders pattern with a minimum downside price target of 13, portending a thirty-five percent decline over the intermediate- term. The rising MACD tells of the current rally. Once the RSI reaches overbought, the MACD should turn down as should prices. The next decline should be impulsive.

Coca Cola (KO) - another Dow Industrials component - may be crashing. It is down 19 percent since March 2004, and plunged sixteen percent this week. It is deeply oversold, so a bounce in this stock should help the DJIA over the short-run, but there may be more downside to come.

Alcoa Inc. (AA), also a DJIA component, is sporting a Bearish Head & Shoulders pattern that should break to the downside once the current corrective rally finishes up over the next two weeks as expected.

The Economy:

Sales of Existing Homes set a record in June according to the National Association of Realtors while Sales of New Homes fell 0.8 percent in June according to the Commerce Department.

According to the Chicago National Association of Purchasing Management, Manufacturing grew sharply in July to a 64.7 reading from 56.4 in June. According to Redbook Research, Weekly Chain Store Sales have decreased 0.3 percent in July versus June.

GDP was reported to have risen only 3.0 percent in the second quarter 2004 compared to 4.5 percent for the first quarter. Durable Goods Orders disappointed, dropping 0.4 percent in June if you exclude defense, after a revised 0.9 percent drop in May, according to the Commerce Department.

Crude Oil set an all-time record high Friday, July 30th, closing at 43.80. It rose $6.66 during the month of July.

According to the Internal Revenue Service, adjusted for inflation, Gross Income for Americans fell a whopping 9.2 percent for the two years ending in 2002. This approximate 10 percent decline is likely due to job losses and underemployment.

Jobless Claims came in at an unacceptable 345,000 for the week ended July 24th, and of course the Labor Department revised the prior week's reported initial claims to 341,000. According to www.cnnmoney.com, Continued Claims rose substantially from 2.79 million to 2.96 million. I wonder how many of these good folks voted for Dubya last time in a tight race? Will they be voting for him again? Should we be preparing for a Kerry Presidency? Time to think about this.

The Conference Board's latest Consumer Confidence reading was reported to be 106.1 in July, up sharply from 102.8 in June. Yet 26.0 percent answered that jobs are "hard to get." Wonder if this considers gasoline going to $2.50 a gallon? Crude's performance tells us it probably is.

Money Supply, the Dollar, & Gold:

M-3 is essentially flat since May 17th, up a mere $9.8 billion over that 9 week period, less than 1 percent annualized growth. Our research shows that whenever M-3 is flat or down for a period of two months or more, equities decline within one to three months thereafter.

The U.S. Dollar is ready to turn down as price action formed a key reversal Hanging Man candlestick pattern Friday, at the point of formidable resistance, the long-term declining trend-channel. The Dollar has formed a Bearish Head & Shoulders Top and a decisive break below 87 will confirm the pattern, with a minimum downside price target of 82. The RSI sits where three recent tops occurred and upside momentum looks like it has peaked. Prices should fall from current levels if for no other reason than they sit at the top of the long-term trend-channel, the place where declines are born.

It is do or die time for Gold the metal, as it is forming a Bearish Head & Shoulders Top and prices have sunk to the lower boundary of its long-term rising trend-channel. There isn't much downside room for Gold before technicals turn decisively Bearish. Should Gold drop below 375, the minimum downside target is 320. Let's all hope this doesn't happen, for if it does, it likely means massive deflation has or is about to occur. The first place this deflation would materialize would likely be in financial assets to soon be followed by real estate assets, then incomes, then goods and services. By the time it hits goods and services, we are likely in a Depression. Before that were to happen, expect the Federal Reserve to open the liquidity spigots wide. The Dollar would be sacrificed before deflation were allowed to take control. Our chart of the Dollar may be discounting this scenario. Once the Fed pumps the money faucet, Gold should recover. So there may be a terrific buying opportunity coming in Gold and precious metals. If you missed out before, you may be about to get another chance.

The above chart compares the HUI Gold Bugs with the Dow Industrials over the past two years. We see that the HUI has tracked the major equity average contemporaneously, except that since December 2003, it may actually be leading the DJIA by a couple of months. The sweet spot of the HUI's decline - a Crash - occurred as an Elliott Wave 3 down between March and May 2004. The DJIA's Wave 3 down isn't scheduled for another couple of weeks, but could resemble the HUI's price action. Gold the metal has followed a similar directional course and likely could follow stock prices lower. What we're seeing here are markets discounting asset deflation. This week the HUI appears to be in a similar countertrend rally as the DJIA but the pattern in HUI is a bit clearer, with a fourth wave triangle continuation pattern telling us prices have further to fall - likely after the HUI becomes overbought in a week or so.

Bonds & Interest Rates:

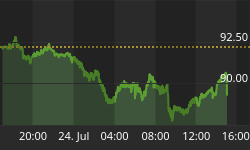

The rally in 10 Year Treasury Notes has further to run as it retraces a Fibonacci percent of the move down from March through May 2004. The minimum retrace we expect is 38.2 percent to 111.69. More likely is a rally to 112.88 (50.0%) or 114.08 is even possible (61.8%). The rally is temporary, is not the start of a Bull run, and we fully expect prices to be overbought once hitting one of these three Fib ratio levels.

The longer term pattern is decidedly Bearish as has been presented in these pages over the past weeks. The long-term chart shows a massive two year Head & Shoulders Topping pattern that will be confirmed with a price decline below 107. The minimum downside target for this pattern is the low 90's in the 10 Year U.S. Treasury Note. This is an intermediate to long-term forecast, but the decline should begin in earnest once the current rally finishes, probably over the next two to three weeks.

The asset deflation we see in Bonds could come in response to massive liquidity being injected into the system by the Fed in response to an equity market event. We shall see.

Bottom Line:

A Bear Market mini-rally has commenced that will serve the purpose of shaking out the shorts and creating overbought market conditions. Intermediate-term Bearish Topping patterns are all over the place and most major financial market index charts are discounting deflation. Complacency reigns as the SPX/VIX ratio is at 72.15 on 7/30/04 - a Crash warning level, Bullish advisors far exceed Bears, and ho-hum, Crude Oil has just set an all-time high the day we learned Consumer Confidence is busting up north. The coming worldwide collapse in financial markets looks like it is going to catch the majority by surprise. But, then again, doesn't a crisis always? Caution is warranted.

"The nations have sunk down in the pit which they have made;

In the net which they hid, their own foot has been caught.

The Lord has made Himself known;

He has executed judgment,

In the work of his own hands, the wicked is snared.

The wicked will return to Sheol,

Even all the nations who forget God."

Psalm 9: 15-17

Special Note: Be sure to register under the subscribers' section at www.technicalindicatorindex.com for e-mail notifications and password access of our new mid-week market analysis, usually available on either Tuesdays or Wednesdays. These midweek updates are only available via password access when posted on the web..

| Key Economic Statistics | ||||||||

| Date | VIX | Mar. U.S. $ | Euro | CRB | Gold | Silver | Crude Oil | 1 Week Avg. M-3 |

| 2/27/04 | 14.53 | 87.89 | 124.52 | 273.90 | 396.8 | 6.71 | 36.16 | 8962.4 b |

| 3/05/04 | 14.52 | 88.75 | 123.28 | 274.00 | 401.6 | 6.99 | 37.26 | 8974.1 b |

| 3/12/04 | 18.21 | 89.60 | 121.80 | 272.00 | 395.6 | 7.06 | 36.19 | 8964.0 b |

| 3/19/04 | 19.15 | 88.56 | 122.47 | 280.20 | 412.7 | 7.56 | 37.62 | 9005.8 b |

| 3/26/04 | 17.12 | 89.30 | 120.90 | 278.25 | 422.3 | 7.71 | 35.73 | 9015.3 b |

| 4/02/04 | 15.81 | 88.80 | 121.12 | 280.00 | 421.1 | 8.15 | 34.39 | 9071.5 b |

| 4/08/04 | 16.38 | 89.82 | 120.56 | 284.00 | 419.9 | 8.09 | 37.14 | 9060.6 b |

| 4/16/04 | 15.00 | 90.18 | 119.50 | 276.75 | 401.6 | 7.14 | 37.74 | 9115.2 b |

| 4/23/04 | 14.01 | 91.34 | 118.18 | 267.50 | 395.7 | 6.16 | 36.46 | 9122.6 b |

| 4/30/04 | 16.69 | 90.76 | 119.70 | 270.75 | 387.5 | 6.07 | 37.38 | 9171.7 b |

| 5/07/04 | 18.13 | 91.30 | 118.83 | 270.40 | 379.1 | 5.58 | 39.93 | 9230.5 b |

| 5/14/04 | 18.47 | 91.81 | 118.69 | 267.00 | 377.1 | 5.72 | 41.38 | 9232.6 b |

| 5/21/04 | 18.44 | 90.53 | 120.05 | 268.75 | 384.9 | 5.87 | 39.93 | 9278.3 b |

| 5/28/04 | 15.52 | 88.98 | 122.10 | 276.25 | 394.0 | 6.11 | 39.88 | 9251.9 b |

| 6/04/04 | 16.57 | 88.50 | 122.93 | 274.75 | 391.7 | 5.81 | 38.49 | 9255.9 b |

| 6/11/04 | 15.10 | 89.23 | 121.01 | 269.25 | 386.6 | 5.78 | 38.45 | 9266.2 b |

| 6/18/04 | 14.95 | 89.41 | 121.17 | 267.75 | 395.7 | 5.98 | 39.00 | 9306.1 b |

| 6/25/04 | 15.19 | 89.22 | 121.41 | 270.75 | 403.2 | 6.12 | 37.55 | 9296.6 b |

| 7/02/04 | 15.15 | 88.18 | 123.09 | 265.50 | 398.7 | 6.01 | 38.39 | 9327.2 b |

| 7/09/04 | 15.78 | 87.41 | 124.10 | 269.00 | 407.0 | 6.46 | 39.96 | 9272.7 b |

| 7/16/04 | 14.43 | 87.12 | 124.36 | 271.50 | 406.8 | 6.72 | 41.25 | 9267.1 b |

| 7/23/04 | 16.50 | 89.23 | 120.88 | 269.50 | 390.5 | 6.33 | 41.71 | 9288.1 b |

| 7/30/04 | 15.27 | 90.12 | 120.10 | 267.00 | 391.7 | 6.56 | 43.80 | - |

Note: VIX down, Dollar up, Crude Oil at Highest Level EVER!