Gold/Oil Ratio Against Equities

In my September 1st piece, I argued the importance of valuing Gold relative to Silver via the Gold/Silver ratio, concluding that gold will UNDERperfom silver despite its status in the limelight. Indeed, the G/S ratio has fallen 7% since the article, hitting a new 13-month low of 59.0. My case for "faster" gains in silver remain in place.

So how about Gold/Oil ratio? Readers of my book and previous articles on the topic recall that the G/O index bears a highly negative correlation with risk appetite/stocks/market sentiment. The rationale being that when G/O ratio ceases to rise and begins to pull lower, it is a case of re-emerging energy prices relative to metals, usually reflecting improved appetite/higher growth/weak-US-based gains in energy prices. The converse case applies.

The G/O ratio is especially valuable during the early stages of a rebound as it predicts deteriorating risk appetite and falling equities (2008 example) while a peak followed by an early stage decline, usually suggests rising stocks, led by higher energy prices (April example) and May example.

With the above evidence continuing to prove effective since 2007 (time of writing my book), let us integrate it into the G/O relationship of today. The chart below shows the G/O ratio in the upper panel and the S&P500 in the lower panel. The latest correlation between S&P500 and G/O ratio on a 2-month rolling basis stands at -0.63. The red lines indicate the inverse correlation of the overall trend. Note how G/O ratio began drifting lower (due to faster oil appreciation relative to gold last week), which has been accompanied with a clear increase in the S&P500 (and other stocks). The break out of the S&P500 above 1,150, could mean further decline in G/O ratio -- potentially towards the 6-month trend line support of 15.20.

And if the above dynamics continue i.e. further declines in G/O ratio and higher S&P500, this could well take the form of rising oil prices revisiting the $86-87 level.

Diamond in the Energy Rough

The weekly US crude oil chart below shows a rare "diamond formation", which in technical analysis is a rare pattern. Diamonds could be either continuation patterns (bullish) or reversal patterns (bearish). In this case, the weekly chart broke above the $80.50 trend line resistance last week (falling trendline line), showing a continuation out of the multi-month pattern, whose 1st half held up during Oct 2009-May 2010. The importance of last week's break out and this week's follow-through is highlighted by the break of the all-important 200-week MA. The next test emerges through a required break above $83, which is the high from Aug 2010 (small red circle). Tuesday's closing price was at $82.82 was not enough. A Friday close above $83 would be necessary, while a close above $75-76 is required to maintain the uptrend.

In the event that $83 is broken with a weekly close (preferably), this stands the chance of extending S&P500 towards its next resistance of 1,190 (200-week MA, which was broken in June 2008) and 11,200 on the Dow Jones Industrials Index. Is this plausible? An "upbeat" US earnings season and rising confidence that US markets will be "liquefied" by Fed asset purchases could well do the trick -- for now. The implications for the USD index suggest a possible decline below the 76 trendline and into a prelim target of 74.

Bank of Japan Follows Fed into Zero, ECB Stands out as "Hero"?

Today's BoJ decision to jump back into zero interest rates along with the Fed means the ECB is left alone with 1.0% policy interest rate, a notion that is hard to resist by FX traders favouring further gains in EUR. This is especially the case as the ECB shortens the duration of available funding. Meanwhile, FRBNY pres Bill Dudley reminded us last week that additional QE is a defacto easing of fed funds rate.

Don't Confound Inadequate Liquidity with Unnecessary Liquidity

Many have wrongly stated that rising EURIBOR rates (Eurozone interbank rate) as a sign of inadequate liquidity, which is a sign of lack of confidence. But they confuse rising EUR interbank rates -- resulting from inadequate liquidity due to lack of lending & trust among banks, with rising EURIBOR -- usually associated with lack of need of funds (the case today after Eurozone banks demanded less loans from ECB). Last week, Eurozone banks demanded EUR 104 bln from the ECB's 3-month liquidity operation, well below the expected EUR 150 bln. JC Trichet has expressed this as sign of less need for funding. But the unexpectedly low demand could further drive up EONIA as excess liquidity declines by an estimated EUR 80 bln. EUR 3-month LIBOR is now at hit a 15-month high of 0.89%, extending the spread over its US counterpart to 0.58 bps, the highest since Feb 2009. As long as the ECB and Eurozne banks are content with shorter marturity loan facilities and any event-risk is averted with regards to the P-I-I-G-S, euro shall remain supported at $1.33. But with my $1.3850 target been hit (see prev IMTs and tweets on twitter.com/alaidi), I need a new fundamental catalyst for a break above $1.3940.

BoJ Easing Will Not be Enough

The decision by the Bank of Japan to purchase everything in sight except for stocks reflects the desperate situation of the central bank. The BoJ slashed its policy rate from 0.1% to between 0% and 0.1%, while creating a temporary fund of about 35 trillion yen to buy various financial assets (government bonds, corporate bonds, and commercial paper). Will the BoJ buy stocks as it did 2 trillion yen worth of bank shares in 2002-3? For those who were around in 2002, remember, the BoJ included stocks in its shopping list well into mid 2003, until.. you guessed it.. it resorted to pure yen-selling intervention into March 2004. The BoJ's measures may be sufficient to prevent yen strength vs. commodity and European currencies but are unlikely to reverse the USDJPY beyond the 85 yen level.

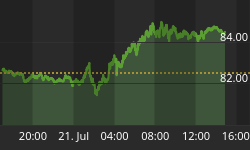

My QE is Bigger than your QE

And if you think the 35 trillion yen announced from the BoJ is large, it is only the equivalent of about $420 billion, which is less than half the anticipated +$1.0 trillion in treasury purchases expected from the Fed. As the Fed's QE2 is set to overwhelm the easing measures of the BoJ, any rebound in USDJPY will be short-lived -- just as short-lived as today's bounce in USDJPY to 84.00 before falling back to 82.97. Can the BoJ ultimately resort to fresh wave of yen-selling intervention? Perhaps, but its case is increasingly untenable considering i) yen is in fact weakening vs most of other currencies; ii) interventions are politically incorrect as they were frowned upon by EU and US officials. I expect gradual selling momentum to re-emerge, triggering 81, with 79.70 an increasing likelihood before year end.

For more frequent forex & Commodity calls & analysis, join our +7400 followers on Twitter