The following is part of Pivotal Events that was published for our subscribers November 11, 2010.

SIGNS OF THE TIMES:

"Personal Debt Ballooning"

"The Best Way to Rob a Bank is to Own One"

- William Black, former FDIC official,

and quoted in the Financial Post on October 21, 2010He also added that the FDIC is intentionally keeping foreclosures down because it does not have enough funds to pay off depositors who are insured by the FDIC.

"If the Democrats are intending to put me out of business, I'm going to put them out of business first."

- Wall Street Journal, October 28, 2010

This was from a small businessman. So far, so good.

"Fed chief Plosser says understanding financial crisis may take 50 years"

- Bloomberg, November 1, 2010

This seems optimistic. Interventionist economists still think the post-1929 crisis was caused by the Fed being tight. And that was eighty years ago!

With all the noise nowadays about "QE2", the second huge effort to destroy the Fed's balance sheet, it is appropriate to review Barron's July 11, 1932 editorial comments on a previous magnificent attempt to reflate the economy.

"The Federal Reserve policy of cheapening credit through the purchase of government bonds has been unable to make a dent in the conservatism of borrower or bank lender, in short, every anti-deflationary effort has yet to provide positive results. The depression is sucking more and more bonds into its vortex."

Financial history is rich with irony. Leading editorials in 1873 boasted that with the Treasury's infinite powers to buy bonds out of the market there was no need to worry about a severe crisis.

In 1884 senior economists began to call that post-bubble contraction as the "Great Depression". It lasted until the recession bottom of 1895 and was still being analyzed as "The Great Depression" as late as 1940.

That "puzzlement" lasted for almost seventy years when another Great Depression became an endless focus of benighted debate.

Are there any leading economists today still trying to determine the cause of the Great Depression that started 137 years ago?

Philadelphia Fed President Charles Plosser please copy.

* * * * *

ALL ONE MARKET

(AOM)

Usually our first section covers the stock market, but recent volatility emphasizes that the swings in most aspects of the financial markets are tied to the US dollar.

A critical part of this is that the Fed's ability to depreciate the dollar needs rising asset prices. Otherwise, it is the old "pushing on a string" story. A more detailed explanation by The Pragmatic Capitalist "A Deep Dive Into The Mechanics Of A QE Transaction" seems plausible.

http://www.businessinsider.com/a-deep-dive-into-the-mechanics-of-a-qe-transaction-2010-11

QE2, of course, is the second phase of "stimulus" - this time by the Fed directly buying treasuries out of the market.

When was this done before?

In late 1999 and into early 2000, the Rubin-Summers Treasury was belligerently buying bonds out of market. By belligerent we mean that the program was loudly broadcast and ambitiously exercised during the last few months of a legendary stock bubble. Despite the arbitrary fuel that boom climaxed with the usual reversal in strained credit markets.

There is evidence of the Treasury buying bonds to impose arbitrary policy in the 1800s when the U.S. was between central banks. As we enjoy noting, at the height of the 1873 bubble, the leading NY newspaper editorialized that nothing could go wrong. The Treasury Secretary was highly regarded and the Treasury was widely considered to be superior to a central bank at rescue operations. Not being on a gold standard would enable the Treasury to buy "endless" amounts of bonds out of the market. Unfortunately, this was not proof against another post-bubble contraction.

As noted above, that Great Depression lasted from 1873 to 1895.

Tuesday's New York session recorded some outside reversals - dollar up, others down.

Downside reversals were clocked by the precious metals, including platinum, the gold/silver ratio, crude oil, wheat, corn and the senior stock indexes. Cotton did the reversal on Wednesday.

Altogether, the reversals are noteworthy. Outside reversals do not necessarily end a trend, but they can be part of the process - either up or down. In this instance it was a striking example of AOM.

CURRENCIES

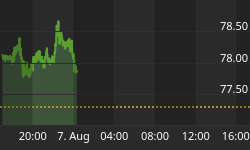

The DX registered a Downside Capitulation in early October which suggested a possible low by the middle of the month. However, this was not accompanied by the Sequential Buy pattern and the bottoming process had to wait until that was registered on Friday. Bearish sentiment became extreme.

The low close last week was 75.8 and that compares to the 76.5 on October 14. Today's continuation of the rebound to 78.3 is impressive and going through 78.5 would set the next uptrend.

Fundamentally, news about fresh disasters in sovereign bonds is supportive, as are the check backs in hot commodities.

On the near term, Democrats can still be dangerous during the "lame duck" session, but this opportunity for mischief will end in late December.

On the longer term, Senator Ron Paul will head up the Ways and Means Committee and he is the most libertarian politician in North America. He will provide some constraint to reckless policy, which will reduce the abuse of the dollar.

Driven by soaring commodities, the Canadian dollar is again at par. For opposite reasons it is vulnerable to around 93.

INTEREST RATES

Modest steepening since early October has recently become outstanding. This has been prompted by the street buying the ten-year in anticipation of aggressive Fed buying. The success of this in boosting the economy is doubtful and should be considered as helping out Wall Street as well as the forces of big government. Also, it should be considered as a desperate attempt to prove that interventionist theories and practice really work.

On the near term, the hype is exaggerating a speculative rise in stocks commodities and corporate bonds.

Mother Nature and Mister Margin are preparing to provide impartial adjudication.

On the rebound to early October our view was that there was support for the long bond at the 130 level, but if that did not hold the decline could reach the 125 level. While this is still possible if suddenly weakening commodities prevail into next week the bond could briefly rally.

There could be some politics in the decision, but the downgrade of US Treasury debt by a ratings agency in China is appropriate. Sometimes it takes an outsider to be bold enough to provide realistic comment.

A sudden change to steepening in May 2007 signaled the start of the "train wreck" in credit markets. This was followed in June with the reversal to widening credit spreads, which confirmed that liquidity was disappearing.

As noted a few weeks ago, there were not technical signals on the trend in the corporate market. The rally with narrowing spreads continued until yesterday when junk spreads widened a little.

In the money market, the TED has widened a little since late September but the chart has yet to break out.

Sovereign debt prices and spreads are again under pressure. Yields for Irish bonds are at a record high.

The risk market has been again enjoying reckless enthusiasm and is eligible for a significant setback.

STOCK MARKETS

The rally since late August has been outstanding and was essentially discounting the electoral set back to crazed Democrats and looking forward to the equally crazed QE2. The S&P gained 18% as the Nasdaq gained 23%.

The RSI reached 80, which is the level that ended the rally to April. As of this week the AAII sentiment reading reached the most bullish for the move.

Tuesday's big reversal on the All One Market suggest a correction has started. This could be reinforced if policymakers, or their lackeys, lose the ability to accomplish the phony rally into the close. It is worth noting that even on the old and notorious Vancouver Stock Exchange promoters were not allowed phony up-ticks going into the close.

Taking out S&P 1204, which provided support yesterday and today, will turn the market down. It could be an intermediate decline.

Link to November 12, 2010 'Bob and Phil Show' on Howestreet.com: http://www.howestreet.com/index.php?pl=/goldradio/index.php/mediaplayer/1837