Blam! Blam! The EU fires and the T-1000 Terminator is blown to bits. Or...is it? There was the ECB's liquidity provisions of 2009, but Greece happened anyway. The EU responded to the Greek crisis with a "shock and awe" package, but in only a few months the T-1000 pulled itself together and kept coming. Now the Union is trying to build a firebreak after Ireland, a line in the sand, and finish off the crisis for good.

It doesn't look hopeful at this point. Although the bleeding among periphery bond markets slowed today, with Portugal and Ireland rallying 16 and 6bps, respectively, and Greece, Italy, and Spain selling off a mere 3-4bps, the Euro itself continued to take a beating and is now back at mid-September levels, down from $1.42 less than a month ago to $1.30 now. And there have been some tentative signs of pressures in the funding markets: front Eurodollar contracts were down 2-4bps while red and green packs were up around 6bps today. Front March is down 15bps over the last week. Since it seems very unlikely that the Fed is going to be tightening any time soon - and indeed, the Fed Funds strip hasn't moved - this seems to be a miniature version of what we saw at times during the 2008-2009 financial crisis. The state of interbank lending needs to be carefully monitored, and surely the ECB and Federal Reserve will be more proactive this time around. But it is a still a sign that all is not well.

The concern all along was that the next financial blow would come before the global economy was fully healed and it appears this concern may be validated by events. Output isn't in the sorry state it was in the middle of the Lehman debacle, but it can hardly be described as robust and healthy. The Case-Shiller Home Price Index has flattened out, and underperformed expectations today. This is not necessarily a bad thing, if properties that were formerly stranded (because their owners wanted to wait for higher prices) are trickling onto the market, but it is a reminder that we are still unwinding the last bubble. The Chicago Purchasing Managers' Report (62.5 vs expectations for 59.9) and Consumer Confidence (54.1 vs expectations for 53.0) were both incrementally stronger-than-expected, but neither has left the range of the last year. Moreover, the Jobs Hard To Get subindex of the Consumer Confidence survey actually rose slightly to 46.5.

None of this spells a collapsing economy (we might also say that it doesn't describe an economy that, on that evidence, needs a central bank to print money), but it also doesn't give the impression of obdurate Schwartzeneggerian implacability. So who's going to face the T-1000? Ben Bernanke? Jean-Claude Trichet? Jean-Claude Van Damme, maybe. Perhaps we're going about this crisis thing all wrong. Muscles from Brussels, indeed.

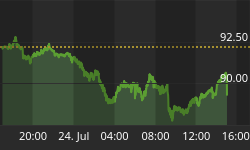

In the absence of Van Damme, investors are seeking protection in dollars, to a lesser extent in commodities - note that in the chart below, the dollar and the SP-GSCI over the last week have both been gaining although they typically mirror each other - and in options.

Commodities and the dollar - recently moving together, though this is hardly without precedent.

Interestingly, and perhaps because the threat is to sovereign issuers, U.S. Treasuries haven't been doing decidedly well. 10-year yields remain 40bps off the lows set at 2.40% in October. Inflation-linked bonds have also been going nowhere fast, although weakening a smidge at the margin. We know the story about equities: somehow treading water and bouncing again today off the 1174-75 level in the S&P. But the VIX is back to levels last seen in early October, although a far cry from the crisis spikes of 2001, 2002, 2007, 2008, and 2010 (May).

Between the VIX and the whiff of LIBOR funding pressures, I suspect that equities might be vulnerable since the momentum of last month has now firmly evaporated. It is courageous to sell stocks into year-end these days, but if the S&P breaks below that 1174ish level there is a good deal of space on the downside before useful support.

Bulls will cross their fingers for the few days leading up to Employment. Tomorrow, the ADP (Consensus: +70k vs +43k last) provides an early snapshot. The ADP report isn't a great look at Employment, especially when the government is taking a very heavy role in hiring, but it is the best indicator we have. And yet, over the last year the Payrolls number has run 876k higher in aggregate than the ADP figure. Coming into 2010, the 5-year average of rolling 12-month periods was about 96k per year, so a very large gap has opened up between Payrolls and ADP. Except for periods when Census firings were dampening Payrolls, ADP hasn't been above Payrolls for a year. Consensus estimates are institutionalizing this expectation, with economists looking for +70k on ADP versus +145 for Payrolls.

I think it is reasonable to suppose that either ADP needs to start catching up to Payrolls, or Payrolls needs to start sagging towards ADP. I suppose I think the latter is slightly more likely since the surveys of consumer attitudes suggests a weaker Employment picture rather than a stronger one, but from a trading standpoint the more relevant observation is that ADP has upside risk and Payrolls downside risk as long as economists forecast - reflexively, it seems to me - the wide spread to continue.

December 1st also brings the final revisions to Q3 Productivity and Unit Labor Costs data, and (more importantly) the ISM Manufacturing report (Consensus: 56.5 from 56.9). The Beige Book is also due out tomorrow afternoon, and car sales throughout the day.