While preparing final copy of December issue of The Agri-Food Value View last week we thought that most of the relevant weather news had been covered. Then from down under came news of too much rain. Australia is not somewhere from which we expect to get such news. More often lack of rain is reported. That rain came as some Australian farmers were attempting to harvest the wheat crop. Yes, Australia is on a different weather cycle from Kansas City.

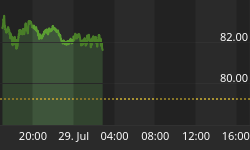

Our Agri-Food Price Index had seemed settled down for a long North American Winter nap. Then rose such a clatter in the pits as all turned to the Australian matter. As can be observed in the chart, the index promptly went to a new high on worries over Australian wheat harvest.

Weather of 2010 has just not been cooperative. Russia, Brazil, Midwestern U.S., Canada, etc. have experienced weather other than that needed or expected. In some, too little rain. In others, too much rain. Russian situation seems so dire that rather than export feed grains, the nation may need to import 3 million tons of feed grains. In any event, no Agri-Grain exports are expected from Russia till the second half of 2011.

Weather is important for one very good reason. Agri-Grains are not produced in a factory. Agri-Grain are produced in dirt, most of which must be watered by rains at the correct times of the year. Further, if part of the Australian wheat harvest, for example, has been lost this year, it will not be replaced till this time in 2011.

Weather has been an issue with Agri-Foods since the first berries were plucked from bushes, or nuts harvested and stored in a cave. Just cannot get around it. Plants require dirt, water, nutrients, and the Sun. They are little solar powered producers of Agri-Food.

Is weather the real issue? Or, is some other factor contributing to the importance of ever fluctuating weather? In a world awash in Agri-Grains, aberrations in the weather might have little impact. Unfortunately, the world is not awash in Agri-Grains.

Above graph may help us uncover the answer to the above question. From the USDA forecasts of global grain supplies in storage at the end of the coming crop year for the Big Four, corn, soybeans, wheat, and rice, is subtracted estimated minimum pipeline needs. Water will not come out of a pipe unless entire pipe has water in it, and a similar concept applies to the Agri-Grain supply chain.

That remainder of useable stored grains was then compared to total global consumption and the 2007-8 lows for inventory/consumption ratios. Vertical axis is number of days of consumption in storage above those 2007-8 lows that led to high prices of 2008. We use days now as the global Agri-Grain supply system is in such short supply that measuring in months has little meaning.

Usable global corn inventories represent only 4 days more of consumption than was the case during the 2007-8 period when prices spiked upward. Wheat is the good news. World has 22 days more of consumption in storage than at the lows that led to the last major price rise. Let us put those numbers into perspective. Any Agri-Grain producing region does so about every 365 days.

Weather in 2010 probably was only part of the recent move in Agri-Grain prices. If the above portrayed inventories were truly adequate, the weather issues with this year's production would have been a non event. However, the global Agri-Grain situation is approaching inadequate, making non optimal weather in any producing region critically important. In this type environment, Agri-Grain prices can do almost anything, and just might.

A consequence that follows from higher grain prices is portrayed in the above chart. In it is plotted the USDA index for beef prices, both hanging and boxed. Not shown in the graph is that beef prices did slide dramatically as a result of the global financial crisis. Since then, beef producers have been reducing herds. First round effect of that is lower price as beeves are sold into the market to avoid the costs of feeding them. Once herds are sufficiently culled, prices rise.

As is readily apparent, beef price are near a 90-week high. Prices initially did react to tightening of Chinese monetary policy and recent move to higher grain prices. However, the smaller size of the global herd has meant the price reaction was, one, muted, and, two, short lived. And now we read from Commodity News for Tomorrow, 6 Dec 2010, in "Beef Prices Soar ... for Now,"

"In the past week, prices reached levels not seen since the autumn of 2008, as the global appetite for beef grows and U.S. ranchers stung by the recession scale back their herds."

"The futures contract for live cattle -- animals finished at the feedlot and headed to slaughter -- closed Monday at more than $1.06 pound on the Chicago Mercantile Exchange. Futures on younger cattle, or feeders, which still need to be fattened, hit all-time highs last week."

"Supplies do remain tight. The number of cows[in U.S.], defined as females that have successfully produced at least one calf, is the lowest since 1963. As of July, the latest month for which data are available, the U.S. calf count was estimated at 35.4 million head -- 1.2% lower than the total a year earlier." [Emphasis added.]

"Domestic[U.S,] beef demand has recovered as the U.S. slowly exits the recession and new markets develop in Southeast Asia, Russia and other regions. The U.S. Meat Export Federation, a trade association, projects that beef and beef byproduct exports are heading toward levels not seen since 2003, a record year."

Given the lower animal head counts and pressure from higher grain prices to keep them low, beef prices will continue to rise over time. Yes, there will be bumps and grinds along the way. But, what we are observing here is a global phenomenon, a trend toward higher meat prices. Recently, the UN FAO's index of global meat prices hit an all time high. Your Gold needs to rise in price, otherwise you might not be able to afford to eat beef in the future.

Finally, we must report that a rumor is false. No shortage of Lexus cars has developed at dealers in Iowa this Winter. Seems most of the potential buyers, flush with cash from their corn harvest, are in the warmer regions, enjoying the bargain rents in empty condominiums. Dealers do expect brisk Spring sales when they return.

AGRI-FOOD THOUGHTS is from Ned W. Schmidt,CFA,CEBS, publisher of The Agri-Food Value View, a monthly exploration of the Agri-Food grand cycle being created by China, India, and Eco-energy. To receive this publication, use this link: http://home.att.net/~nwschmidt/Order_AgriValue.html