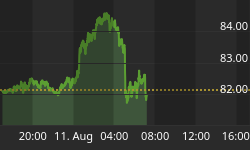

Stocks ended flat on the day, but bonds ended higher for a change. The catalyst, interestingly, was a court decision.

Bonds had been lower overnight, and stocks higher as has become the norm over the last couple of weeks. Around 11:00ET, however, a District judge ruled that part of Obamacare is unconstitutional. Specifically, according to the judge (who is of course not the last word, but it's getting closer) the federal government cannot compel citizens to maintain minimum health coverage.

This is a big blow to Obamacare, because the large costs of the plan are only as small as they are because the law forces healthy people to buy insurance that is overpriced for them. This is a frequent problem with insurance. Why should a good driver pay $1,000 per year for insurance? Because that good driver is subsidizing the legally-capped rates on the really bad drivers. Insurance companies would lose money hand over fist if they were forced to insure bad drivers at rates limited by the insurance board, unless they also have a bunch of good drivers overpaying for the same coverage. If this part of Obamacare is thrown out, then a re-assessment of the program's costs should find a dramatically higher price tag. The implication is that the law is much more likely to be repealed now, and this implies smaller future deficits. So bonds rally, for at least an hour or two!

Tomorrow, the data deluge for this week begins. Of some interest will be the November Retail Sales (Consensus: +0.6%, +0.6% ex-auto). Of somewhat less interest is the PPI (Consensus: +0.6%, +0.2% ex-food-and-energy). Of least interest...probably...is the outcome from the FOMC meeting.

I have to couch that as "probably" because the rotation of FOMC membership in 2011 will change the composition of the Board significantly. Gone will be hawkish gadfly Hoenig, but also moderate Pianalto and doves Bullard and Rosengren; in will come Chicago Fed President Evans (hawk), Philadelphia Fed President Plosser (generally a hawk), Dallas Fed President Fisher (hawk, but also relies a lot on the signals from gold), and Minneapolis Fed President Kocherlakota (confused dove; earlier this year he advocated raising rates to cause inflation expectations to rise. It is hard to imagine what we'll get out of an FOMC member who is that squishy on economic fundamentals). This chart makes the balance of power move pretty obvious, although of course the positions of the particular officials on the scale can be debated.

This means that if the Chairman has any desire to extend the QE2 program, his opposition will be lighter if he does it this month. One might even speculate that it would be more tactically adroit to be extra-dovish this month so that next month, when the new Congress and new Fed Overseer Ron Paul take their seats, the Committee has room to appear more hawkish. In some sense, this will be the last time it will be easy to be easy.

I don't really expect any major changes to come out of the FOMC meeting when the results are announced tomorrow. However, the Committee could extend the duration of QE2. I doubt that will happen, because it would set up expectations (which would be easy to dash, but the Fed hates to dash expectations rather than to set the up correctly in the first place) that the end of QE2 will be signaled no less than 4-5 months in advance, when at some point the Fed decides not to extend the maturity date of the bond buying. To reiterate, I do not expect this change, but it is possible. On the other hand, it is very unlikely that they would foreshorten the plan already, especially since there will be pressure to do just that in 2011.

I suspect that the most likely outcome is a fairly innocuous statement with no significant change in policy. Employers certainly "remain reluctant to add to payrolls," and Housing starts "continue to be depressed."

However, one topic that will be getting increasing attention in 2011, I expect, is the question of whether the central bank should adopt a price level target, even informally, rather than the informal inflation target it currently has (1.5%-2.0% on core PCE, 1.75%-2.25% on core CPI is how it's usually perceived). Under a price-level target, the central bank declares that if the price level today is 100, then it seeks to establish the price level in (for example) 10 years as 121.9 (that is, 2% compounded inflation). The difference is simple: under an inflation target, past misses are forgotten while under a price-level target the bank attempts to make up for past misses - lower-than-optimal inflation is made up for by a later period of higher-than-optimal inflation.

Chairman Bernanke broached the subject in his August speech at Jackson Hole, saying:

"A rather different type of policy option, which has been proposed by a number of economists, would have the Committee increase its medium-term inflation goals above levels consistent with price stability. I see no support for this option on the FOMC. Conceivably, such a step might make sense in a situation in which a prolonged period of deflation had greatly weakened the confidence of the public in the ability of the central bank to achieve price stability, so that drastic measures were required to shift expectations. Also, in such a situation, higher inflation for a time, by compensating for the prior period of deflation, could help return the price level to what was expected by people who signed long-term contracts, such as debt contracts, before the deflation began."

He then downplayed the value of this strategy:

"However, such a strategy is inappropriate for the United States in current circumstances. Inflation expectations appear reasonably well-anchored, and both inflation expectations and actual inflation remain within a range consistent with price stability. In this context, raising the inflation objective would likely entail much greater costs than benefits. Inflation would be higher and probably more volatile under such a policy, undermining confidence and the ability of firms and households to make longer-term plans, while squandering the Fed's hard-won inflation credibility. Inflation expectations would also likely become significantly less stable, and risk premiums in asset markets--including inflation risk premiums--would rise. The combination of increased uncertainty for households and businesses, higher risk premiums in financial markets, and the potential for destabilizing movements in commodity and currency markets would likely overwhelm any benefits arising from this strategy."

But it is worth reflecting on that dismissal, because the arguments he gives against are pretty poor - they're not even the best arguments against, as I'll show in a moment. "Inflation would be higher and probably more volatile under such a policy," he says, but this is presumably the point. In the short run, inflation would be more volatile because it would no longer be a crucial policy variable. Over the target horizon, though, the volatility would diminish as the time to the target reduced. Ideally, the volatility of the price index 10 years in the future would be zero. If that is the case, then the fact that the 1-year volatility is higher is not terribly important. The Fed would be trying to make inflation considerations irrelevant for long-term investments and contracts. Indeed, if the market believed that such a policy was credible, then we would see a big change in the implied volatility curve in inflation options. Short-dated vols may rise, but longer-term vols around the target tenor would decline; beyond the target date, vols would increase again.

Think of volatility being the scatter of bullets being fired by a cowboy on a bucking bronco at a stationary target. If the cowboy is a decent shot, then the bullets might leave the pistol from anywhere - way up there, way down here, way off to one side - but will all go through the target. On the other side of the target, they'll spread out again. The vol curve in short would be "squished" in the middle.

If the Fed were able to achieve this feat, why would it be squandering its hard-won inflation credibility? It would seem to me to enhance it if Bronco Ben were able to hit the target. He sure is missing the target at the moment.

I think the Chairman was setting up a straw man on purpose, so that as the debate continues he can look like the sage wise man who carefully considered both sides of the story. But the available evidence is that he has made up his own mind on the subject. For example, see the book he wrote in 2001 with Laubach, Mishkin, and Posen.

I expect that it will be difficult for the Fed to adopt such a policy. Kansas City Fed economist George A. Kahn pointed out some of the reasons why the Federal Reserve is unlikely to pursue it in a good, readable paper published in 2009. He writes:

"While price-level targeting offers a number of potential benefits relative to inflation targeting, the benefits may be relatively small and uncertain. In addition, price-level targeting is untested in practice...;and would present challenges for policymakers in communicating with the public regarding the objectives and direction of policy over the medium run. As a result, price-level targeting will not likely be adopted by central bankers without considerable further research or a dramatic deterioration in economic performance that leads policymakers to fundamentally reconsider how they conduct monetary policy."

But I think the best argument against the Fed taking such a step is this from Kahn:

"Another reason central banks may not be willing to embrace price-level targeting is that they have no modern practical experience with such targets. All of the arguments supporting price-level targets come from economic theory and past empirical relationships. The economic theory is a highly stylized representation of the actual economy that abstracts from many real world considerations...;while some policymakers may find price-level targets appealing, no central bank may be willing to be the first to implement them. Every central bank may be waiting to learn from the experience of another central bank."

Now, I am not really a fan of price-level targeting, because I don't think the central bank has anything like the amount of control that is necessary to plausibly zero in on such a goal. It does make a lot more sense than pursuing a one-year target, which is essentially what they are doing now, but in general I think the Fed ought to focus on simply avoiding big policy errors, something it hasn't been able to do in the last couple of decades.

I think Kahn makes very good arguments against implementing a price-level target any time reasonably soon. But we have not factored in the fact that Chairman Bernanke, while often wrong, is rarely in doubt. I fear his overconfidence in these models. They remind me of the time my employer was a bank stuffed with quants. I had been there a few weeks when my boss thrust a paper in front of me that had pages and pages of mathematics asserting an abstruse phenomenon about inflation derivatives. "What about this?" he challenged, apparently assuming I had been unaware of this theory. "What I know," I said, "is that the effect is small, it is in our favor, and the market values it at zero." He stomped off and set our quants to work on it. After three months of work, we had math to prove that the effect was small, and in our favor, and it was a simple matter then to prove the market valued it at zero. So I was right, but the important thing was that now we had a mathematical model. That bank, more than any one I have ever been at, was willing to take ridiculous risks as long as there was some mathematical model that supported the pricing. Bernanke seems to me to be cut from the same cloth. "Let's do it," I can hear him saying authoritatively. "The math works."

Now, again - I don't know if this is on the agenda for tomorrow, and even if it is I rather doubt that it would be implemented at the meeting. But looking into 2011 I expect we will hear an increasing number of speeches on this topic.

{kind=link}