ONIONS! Will the onion shortage in India bring down another government, as was the case in 1998? Onions in India are much like garlic in Italy, an essential part of the good life. In India, onion demand is exceeding the ability of the nation to supply onions. Price of onions has doubled(AFP, 22 December 2010). Spice prices, of which India produces half of the world's supply, have had a similar surge(Financial Times, 31 December 2010). Onions and sugar are ominous omens of the Agri-Food world of tomorrow.

Agri-Food Value View

While onion prices are not included in our Agri-Food Price Index, they were not necessary to move the index to a new high. Around the world rising global demand along with constrained supply slammed into the weather, most of which was bad. From drought in Russia to flooding in Australia, that which could go wrong has gone wrong. If the world had adequate reserves of Agri-Food such developments would not matter, but it does not.

Regrettably, the world does not have bountiful Agri-Food reserves. U.S. Department of Agriculture(USDA) forecasts that in this coming year the world will have only 41 days of corn in reserves. Rice reserves will be only 61 days. Wheat is a guess as no one knows yet how much will come out of Russia, if any, or the U.S. As an indication of the wheat situation, U.S. export sales, made but not completed, are up more than 100% from a year ago.

Onions, sugar, and cotton, about which we talked last time, are important indicators of the global Agri-Food situation. Why? Some of them are not absolutely necessary, onions and sugar, or necessary in overly bountiful quantity, cotton. Most of us could live with a few less T-shirts per year. Their production, though, must compete with real foods, those necessary to sustain people. In the world of tomorrow, onions, sugar, and cotton must compete with corn and soybeans for productive acreage. Sugar at one time was a food only available to the aristocracy, and that may happen again.

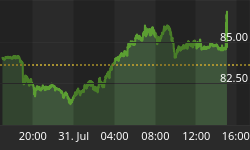

Other signs of stress are apparent in the global Agri-Food system. Palm oil price is portrayed in the chart below. Palm oil is the most consumed vegetable oil in the world. China and India are both the largest consumers and importers of vegetable oils. With domestic consumption of edible oils in those two nations exceeding production, growing demand on global edible oil supplies is likely to continue. As is apparent in the chart, palm oil prices have moved dramatically higher.

Vegetable oils are essential to the cooking process. Every meal we eat either includes vegetable oil or another Agri-Food that must compete for the supply of oil seed grains. Edible oils are derived from oil palm fruit and the crushing of soybeans, corn, canola, sesame, etc. Cooking in vegetable oils rather than animal fats may not appease the food gestapo, but it may become necessary. Necessary does not, however, mean cheaper.

Agri-Food Value View

The extraordinary weather related price gains will likely fade sometime this year. Weather is a classic case of a system that tends to regress to the mean. Bad weather becomes normal, and good weather gets worse.

Those strong Agri-Food price gains of 2010 supported dramatic price action in many of the Agri-Equities. Should weather become more normal, those equity prices might be forced to normalize. Between now and then, investors have an opportunity to research those Agri-Equities. If one's portfolio was void of Agri-Equities in 2010, that is, as they say, water under the bridge. One would not want to make the same mistake when looking back from 2012.

Finally, we have no further information on rumor that the Lexus might become the state bird of Iowa.

Our 4th Agri-Food Commodities: An Investment Alternative, January 2011 has recently been released. This analysis, though statistical, dry, and boring, is rapidly becoming the standard for reporting the returns produced by Agri-Food commodity prices. It thoroughly documents the superiority of returns produced by Agri-Food commodity prices, which ultimately drive the returns on Agri-Investments. This report can be previewed at our web site or at www.scribd.com

AGRI-FOOD THOUGHTS is from Ned W. Schmidt,CFA,CEBS, publisher of The Agri-Food Value View, a monthly exploration of the Agri-Food grand cycle being created by China, India, and Agri-Energy. To contract Ned or to learn more, use this link: www.agrifoodvalueview.com