Markets recently have been reversing Mackay's classic observation that "Men...think in herds; it will be seen that they go mad in herds, while they only recover their senses slowly, and one by one." Instead, the slow march of stocks higher has meant that people have been going mad one by one, and joining the crowd. Does the maxim hold true in reverse? Will they recover their senses in herds?

This would be a bad thing, and I am relieved to observe that while the 1% decline in equities today was the largest single-day selloff since November 23rd, the volume was not appreciably different from yesterday's volume. A bear might growl that this shows how much lower even a little selling might push prices, but classic technical analysis would expect to see a swelling of volume to confirm a trend change.

My suspicion, techies or no, is that this is more than a one-day respite in a relentless march. The wors The negative earnings surprises and/or downbeat announcements from Goldman, Wells Fargo, Northern Trust, Citigroup, and American Express (cutting 550 jobs) helped drive the NASDAQ Bank Index down 2.6%. Barclays just laid off a number of people, many of them very senior, with essentially no warning. Anecdotally, I can report friends at other dealers who are starting to size up their options/escape hatch as well. This is all very strange if you read the economic headlines, or even the earnings reports which, while downbeat, weren't exactly the big losses of 2008-09. Is there some signal here about the economy, or is the financial reform bill just damaging prospects for financial institutions? Or am I reading too much into narrow anecdotal evidence. I will just say the state of the banking sector just feels less bumptious than it did just a couple of months ago.

Homebuilders were also down, some 3.5% as measured by the S&P 500 Homebuilding Index. Surely this cannot be simply a reaction to the weak New Home Sales number (529k vs 550k expected). After all, the inventory of new homes (which isn't in the Housing Starts report, but is relevant here) is at the lowest level since 1968 (see Chart), and adjusted for population it is probably at the lowest level ever.

Inventory of New Homes. Yes, they compete with the high inventories of EXISTING homes, but this picture is reasonably upbeat for the home building industry in the long-term.

Both banking and homebuilding, of course, were sectors that cratered and were bailed out in the housing crisis. Could they be canaries in the coal mine now? I doubt it on the homebuilder side, but I have long held that the mega-bank is going to be an expensive use of capital now that the social costs of being big have resulted in legislation that will have the effect of lower volumes, lower margins, and lower leverage. All three legs of the ROE formula, in other words, will be under pressure; the future should belong to the boutiques and partnerships...just as the past once belonged to Merrill, Lynch, Pierce, Fenner, and Smith instead of Merrill/BOA.

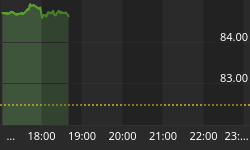

The tiny tremor in stocks today - which, granted, feels like a massive earthquake since it has been so long since the last tiny tremor - is only a warning. But it is a warning echoed in the breakdown of the dollar below its trading range for the last two months (see Chart).

Dollar is looking soggy again.

None of these little hints and wiggles would matter much in the normal course of events. They're not big news. The problem is that there are a lot of people waiting for a Sign to Get Out. Several of these things could be construed to be enough of a warning for a nervous investor to flee. The question is whether these investors regain their senses one by one, or in herds.

It is far too early to make this suggestion, but I think a reasonably gentle 2.5% further selloff to 1250 on the S&P would be welcomed by many. A more-rapid decline, say if today's 1% turns into tomorrow's 1.5% and Friday's 2%, would cause more concern and widen the range of possible outcomes thereafter. In this circumstance I think it isn't whether you wake up the giant, or when you wake up the giant, but how you wake him up, and jumping on his chest is unlikely to produce the results you would like.

I am not sure that economic data will have anything to do with the unfolding retreat, but if Initial Claims (Consensus: 420k from 445k) fails to drop back onto the improving trend or if Existing Home Sales (Consensus: 4.87mm versus 4.68mm last) goes down instead of up, those will be additional irritants for the investing public. Tomorrow also brings the Philly Fed Index (Consensus: 20.8, unchanged), which is expected to stay near the 2010 highs. There is plenty of scope for disappointment, in my view.

By the way, I am not terribly sanguine about bonds, either. Yields are very low, and although weak economic data is typically good for bonds I think that is less clear when the government plainly needs growth in order to be able to redeem those bonds some day (at least, in the absence of debt monetization). Given that we are still struggling with the deficit from the 2008-09 crisis, is it good for bonds if we enter another recession or even a period of choppy near-zero growth? I think the answer there is unclear. Commodity indices for me still look like the best medium-term bet although they have certainly come far themselves in the last few months.

However, the Treasury is going to issue $13bln of a new 10y TIPS bond tomorrow, with a real yield that will be near 1%. That is pretty uninteresting unless your alternative is the 10y nominal note at 3.33%. I am not fond of the duration, even in real bonds, but I suspect the auction will go fine. The TIPS market continues to be in a zero-net-supply situation with the Fed essentially providing all the new cash that the Treasury raises through the TIPS auctions. It is hard to be bearish on auction results in that situation.