Website - http://www.authenticmoney.com with other services & prices

NEW SERVICES! See details below!

• Special Offer!: -Do you want to receive your own copy of "Gold - The Weekly Global Perspective" directto you? -

Send e-mail address to: gold-authenticmoney@iafrica.com

That was the week that was!

The "churning" of the markets continued this week, with the gold price doing its best to go up, then its best to go down, but not making it convincingly either way. Don't you get that feeling of being 'squeezed' by the narrowing trading range of the gold price. Like two boxers no longer dancing around the ring they slug it out in the centre of the ring, until one is down. We've said it before and we'll say it again, when this narrowing occurs, get ready for it to spring, with vigour, one way or another! New York dominated the action again.

Gold remains related to the Euro, but no longer shadowing it. We do believe that the $/Euro play is prime, but other factors, like oil, like, general instability, like uncertainty, are impacting on gold at times taking it in a different direction to the Euro. The author was treated to a micro-light flight this week and learned just what those feelings are like, when they threaten to take over. The feeling that you are about to panic and want to get off the plane [sorry, no ground under your feet], when you are flying next to cliff threatens you, as you find this tiny seat underneath you and only air everywhere else. We are not there yet, but those feelings are on the horizon. After the elections perhaps....?

The Euro price has gone over the 330 level, only to fall back to the 326 level and then back up over the 330 level again. The Euro itself fell back a cent and has not been able to recover, so far. The market shrugged off record deficits and also shrugged off data reassurances that the recovery was on the up. So where now?

Short term prospects for the price:

Short term prospects for the price:

Will we have more of the same as last week, or will we come to a break out point? The week revealed some strong fundamental news as we mention below and yet the gold price has not reacted. The "churning" belies many major flows of the tides and currents, which has to break surface at some stage. But when? Gold seems to have established its own levels against both the Euro and the $, so expect that to continue!

Most market players and observers are still waiting for something to take the lead for them. The vigour of the market move may well catch people off guard and with the feeling they have missed the bus. We are helping our Subscribers to be in position, whichever way it goes, before these moves. But must the gold price go lower first or will it spring up from this position, before you act?

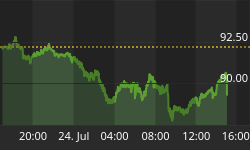

At the time of writing gold stood at $403.45 and Euros 332.39. The Euro itself is worth $1.2138.

Large Scale Speculators.

A drop of 58 ½ tonnes in the speculative long position in gold cleaned up the capricious holders of gold on this front. We have seen the funds back in on the long side, nibbling at around current levels. Even now with inflation data showing it is at low levels they are there, positive on gold.

Italy and Holland state their position in the 2004 C.B.G.A.

After the Chinese Central Bank Governor made it crystal clear he wants the Chinese citizens to buy gold and will do all he can to make it easier to do so and after Argentina demonstrated the value of gold in its reserves by buying it, the stage was set for more news on the 2004 Central Bank Gold Agreement due to begin on the 27th September. It is clear that more than one Central Bank will declare its intent at the I.M.F. meeting held in October. Holland's Central Banker Nout Wellink confirmed the already known position that it would continue to sell its gold under this agreement. It has 50 tonnes left over from the previous "Washington Agreement" and intends to sell a further 100 tonnes within the life of the next agreement. But he added a twist, by removing any specific timing to the sales.

Italy will have something more to say then, than the terse statement that "The Bank of Italy ... has not spoken of this matter, nor does any plan of this type exist." What does this mean for the price of gold? New Subscribers to Gold - Authentic Money will receive the latest article it produced on this plus our expectations for the market and rice of gold.

India - The interest arbitrage continues! Gold cheaper to importers than buyer on the market. Gold demand rising!

Consumption of gold in India increased by 10% to 343 tonnes during the first half of 2004, against 312 tonnes same period last year, according to the World Gold Council. Will this mean a topping of 800 tonnes for the year? in the internal interest rates and the rate at which they finance their imports to gain their extra profit, so lowering the effective price at which they buy gold. An example referred to importers or exporters getting sale proceeds within, for example, 30 to 45 days against Letters of Credit opened by Indian banks. The proceeds are then deposited with banks as Fixed Deposits for opening further Letters of Credit - a cycle that has resulted in huge fixed deposits and huge outstanding Letters of Credit. The turnover of the entity in some cases jumped more than ten times within a short period. Are they real transactions, or is this a new version of futures/derivatives trading?

With their gold season opening up now, having had a reasonably good monsoon all expect a good demand for the last quarter of this year from the 300,000 gold retailers supplying the [wise] gold loving Indians. Note please that their demand is not affected by the state of the U.S. economy, per se!

The U.S. Recovery? Features on 15th September 2004. - Tony Henfrey

Most U.S. citizens have the bulk of their assets invested in their homes, with their pensions invested in equities. An article in the New York times of 5th of September commented that the rise in debt incurred by consumers, business and government "has bulged like the belly of a contestant at a hot-dog eating contest at Coney Island." They pointed out that total debt has "more than doubled since 1994." Chart 1, at the left shows the total of all loans and leases by US commercial banks since 1975 has risen from $525 billion to $4677.3 billion at the end of July. In January 1994 the total was $2200.4 billion, which is an increase of 112%. So bulging it certainly is and there's no stopping it!  One aspect of this debt is that business debt is now $879.3 billion compared to $594.7 billion in January 1994 (only 48% higher) but it is down from its peak of $1097 billion in January 2001. So business is not the culprit. In fact corporate profits and cash flow have been healthy this year. But business hasn't been hiring, hasn't increased wages and has not added productive capacity. Where have these profits gone? Data for July shows corporate stock buyback totalled $38.7 billion (the largest total in 20 years) and four times the typical monthly amount during the past year. So business hasn't been borrowing (no need to because business is not growing) but has been buying their own equity. Remaining shareholders are delighted, but is there an element of support for share prices here?

One aspect of this debt is that business debt is now $879.3 billion compared to $594.7 billion in January 1994 (only 48% higher) but it is down from its peak of $1097 billion in January 2001. So business is not the culprit. In fact corporate profits and cash flow have been healthy this year. But business hasn't been hiring, hasn't increased wages and has not added productive capacity. Where have these profits gone? Data for July shows corporate stock buyback totalled $38.7 billion (the largest total in 20 years) and four times the typical monthly amount during the past year. So business hasn't been borrowing (no need to because business is not growing) but has been buying their own equity. Remaining shareholders are delighted, but is there an element of support for share prices here?

Chart 2 shows just where the borrowing is coming from. Buyers of property. This chart shows that real estate loans at all US commercial banks as a percentage of total loans is now 51.4%. So more than half of U.S. debt is secured by property. Real estate loans have increased from $946.2 billion in January 1994 to $2,405.9 billion in July 2004 which is an increase of 154%. Interesting too that the rise from the 1972 low has moved up in an obvious Elliott 5 waves pattern and when that happens, when 5 waves have terminated? The following comment from the 8th of September Wall Street Journal is worth pondering: "The red-hot housing market is showing its first signs of cooling, as sales of existing homes fell 2.9% in July." If property and equity prices start falling together, when there is so much debt outstanding, what next?

Chart 2 shows just where the borrowing is coming from. Buyers of property. This chart shows that real estate loans at all US commercial banks as a percentage of total loans is now 51.4%. So more than half of U.S. debt is secured by property. Real estate loans have increased from $946.2 billion in January 1994 to $2,405.9 billion in July 2004 which is an increase of 154%. Interesting too that the rise from the 1972 low has moved up in an obvious Elliott 5 waves pattern and when that happens, when 5 waves have terminated? The following comment from the 8th of September Wall Street Journal is worth pondering: "The red-hot housing market is showing its first signs of cooling, as sales of existing homes fell 2.9% in July." If property and equity prices start falling together, when there is so much debt outstanding, what next?

President Thabo Mbeki vs Anglo American.

In a series of interchanges an issue that will spread across the globe has been a matter of contention between the President of South Africa and the leading mining conglomerate, Anglo American. The concept of "political risk" as seen by the two entities, government and capitalism, has taken centre stage. A government should, as President Mbeki states, care for the welfare of its people, but a company with a profit motive must maximise profits. The two principles are set for a head-on collision, not only in South Africa, but across the world, as capital flows and production moves to the cheapest and most productive countries such as China, from the higher cost producers, [including South Africa] such as Europe and the States. This osmotic process is irresistible when the profit motive takes top priority. Taxes reduce profitability and South African taxes and Royalties are set to rise. Costs in the developed world are far higher than those, where there are 300 million poorly paid farm workers waiting to move to the cities for a little more money. The pressure from profits have made companies mobile!

Governments will at some stage soon, object to this, the only way they know how - controls, whether they be on capital, [capital controls, called exchange controls exist in South Africa and have done so for nearly twenty years.] borrowing to invest overseas, etc, etc, the day will come when it starts in earnest! Protectionism is what its called.

Mugabe says Zimbabweans want 50% of the mines

It was irresistible! In the '80's Mugabe confiscated the foreign shareholdings of Zimbabweans, exchanging them for 4% government bonds [now worth 0.15% of their original value in U.S.$]. In the last few years, he authorised the confiscation of white owned land and a handing over of this land to "War" veterans. Now there is starvation in the Bulawayo region, with hundred dying growing to thousands dying soon, with no forex reserves with which to import food. He has just announced that 'Zimbabwe' is to take 50% of the mining shares in local mining operations. What will he pay for these shares, if anything? Which Zimbabweans will own the shares? It does not take a deep analysis to see that projects like Anglo Platinum's new $700 million investment in the country look extremely dubious, to say the least? For the benefit of those who analyse shares, please take into account the scurrilous system of 'black market' exchange rates for imports and ridiculously overpriced exchange rates that apply to the repatriation of export proceeds, in Zimbabwe. And if that doesn't do the trick they can legislate other means of draining cash flow. - 'Hamba Gashle' [Be careful]!

G.F.M.S. figures.

The well respected firm of G.F.M.S. has just released the gold supply/demand figures for the fist half of this year. They are extremely conservative in their approach with their forecasts concluding that there will be a modest price rise through the rest of this year with a better performance seen for next year. Many of the supply and demand fundamentals will turn generally supportive over the second half of the year. G.F.M.S. sees investor activity as somewhat sidelined for much of the second half of 2004, though they do caution an investor-led up-tick in prices is possible in the tail end of the year. Investors seem to be biding their time, waiting to see the results of the US presidential elections. The dramatic activity of the large scale speculators hoping for a burst upwards in the gold price, with them investing in (a residual that approximates to western investment) 444 tonnes in the second half of last year, turning round to dis-invest 143 tonnes in the first six months of this year. The remaining investment highlights that the bulk of 300 tonnes still remains invested in gold. This is because the longs built up by the more fundamentally driven investor remained largely intact.

On the supply side, mine production [down 84 tonnes or 7%] and official sector sales [down to 200 tonnes total] fell (the latter substantially), while on the demand side, bar hoarding [up 66% to 133 tonnes] (a measure of non-western investment) and producer de-hedging [at 200 tonnes] were up substantially, compared to the second half of last year. G.F.M.S. Managing Director, Mr Philip Klapwijk pointed out something we have said for so long now, "....but it's also a good indicator of general market sentiment - you don't slash hedge cover if you think the price is going to slump."

We are delighted at this report as it confirms our projections and conclusion we came to in the series of 4 articles, "What's driving the gold Price", published in Gold - Authentic Money earlier this year. We will be re-issuing one part of these, onto this site in the next day, for you to see.

However, we must point out a feature of the gold market, not so intricately involved in other markets, that of the synergy that gold market factors can have on each other. The old saying "he who sows the wind, reaps the whirlwind" describes an effect that can be seen in the gold market. We will be expanding on this further in our publications below as there is not enough space to give this concept justice here.

Silver $6.26

Having bounced off $6.08, Silver recovered to $6.26 at the moment. Still not looking good, the price's bounce, whilst a relief for the Silver Bulls, is not yet convincing enough to have us believe that the fall is complete, despite signs that base building features are appearing? Let's see what happens. Silver longs liquidated 49 million ounces of position up to the 7th August, the last figures disclosed last Friday. This seems to have dried up to a large extent now.

Platinum $840

Even Platinum saw a drop in speculative positions of 46,000 ounces up to the 7th September. Like Silver Platinum looks for gold to take the lead on the price front!

The London Gold Fix

16th September a.m. $404.40 E 333.04 16th September p.m. $404.45 E 331.897

New Services:

• For one of any of these new services our Subscription price is ... $169 p. a.

• For two of these new services our price willbe another... $126 p.a. [total $295 p.a.]

• For three of these new services our price willbe another$100 ... $100 p.a. [total $395 p.a.]

Weekly

1. "Changing Tack - The Metals Gold & Silver" - Short term Technicals on: Gold & Silver + Gold/Silver Ratio

2. "Changing Tack - Indices" - Short term Technicals on the Gold Indices: HUI - XAU - JSE

3. "Changing Tack - Ratios" - Short term Technicals on: Gold/ Dow Jones Ind. Ratio Gold/ $ Ratio & Gold / Silver Ratio.

Approximately Bi Monthly

4. "Gold - Authentic Money - Gold & Silver" with The Gold Market report in full + Medium/Long term Technicals on Gold [in $ & Euros] & Silver - Gold Silver Ratio + main article on gold market facets.

5. "Gold - Authentic Money - Gold's Macro Economic scene" - Market Perspectives Medium/Long term Technicals on Dow Jones - Gold/Dow Jones I.A Ratio - Gold / U.S.$ Index Ratio + main article on gold market facets.

6. "Gold - Authentic Money - Indices" - Gold Market report in full + Medium/Long term Technicals on XAU - XAU / Gold Ratio - J.S.E. in $ J.S.E. / Gold price Ratio

For Online Subscriptions go to:- www.authenticmoney.com

Contact us direct at: goldauthenticmoney@iafrica.com