A "Macro" Trend: Energy (yes, we're jumping on that bandwagon too, sorry contrarians)

Will it stay that way? Right now it's tough to say if we have become parochial or nearsighted and have fixated on the China demand story. (Solutions like uranium pellet bed technology, a mid-20th Century atomic energy solution waylaid by people like Admiral Rickover when atomic submarines were being rolled out, is still under R&D here and in China and hopefully will be rolled out to meet the growth in energy demand, but it won't happen anytime soon.). We note that the market faded OPEC's recent announcements of boosting production, and have observed the impact on the markets from worry over the recent terrifying hurricanes smashing the Caribbean and parts north (several "black swans" in succession as someone around here would put it). Markets were freaked over what Mother Nature would do to the energy complex in Louisiana (which is responsible for so much of our production and supply). We think the big, longer-term picture is that some parts of the world will keep growing, albeit with occasional painful market corrections, in the developing emerging markets. "The facts are that as you look to the future nearly every developed country will be a significant importer of petroleum, fossil fuels, oil and gas," to quote remarks from the chief executive of ExxonMobil, Lee Raymond, at an OPEC sponsored conference in Vienna. While not exactly a disinterested party to the issue, it seems that way to us too. (Those who are more interested in our sister publication, Rooster Research Contrarian Note no doubt chortle at our stance.)

We don't think the longer term demand for energy and energy related services and technology is driven by just the current loose regional credit regime in China (being tightened in the name of " soft landing"), and we also believe that we should be concerned about the structural limits of the developed world's productive capacity (raw material exploration and production, storage and processed/finished goods transportation), which overshadows the strains of the recent uptick in the (non-financial part of the) US economy. With this bias in mind, we're going to suggest just two ideas to start with in energy, for the long haul.

The recent hyperactivity in trading energy, such as in speculation in energy futures, the re-entry of Wall Street in energy trading and finance, and in the concern over the "tax" of higher energy costs and inflation, gives us pause. The recent up-tick in economic activity included a boost in travel, and in the subsequent travel demand for more lighter crude (e.g. jet fuel) than the thicker/higher sulfur "sour" variety (e.g. power plants). The seasonal summer's end, producer announcements and refinery maintenance shutdowns (and the recent horrible hurricanes) also were market news used by traders. We suspect there could be more to come, fitfully, and will end some time in the future, when Wall Street starts issuing research reports, with the weight and size of telephone phone directory books, about this sector, at the expense of coverage of other industries (with the exception of China and nanotech. A tongue-in-cheek assertion yes, but you never know.) We'll be blunt and indicate our buy and hold bias in this area. We're probably wrong near-term for trading purposes, but that doubtfulness is in our editorial nature and we invite you to be skeptical too and join in the fun.

Suncor Energy (SU), seems like an attractive choice to us, and despite oil's run up to $50 and then a reversal to the mid 40s, we think the argument for the long term is both apparent, but also compelling. Our resident contrarians say watch out, especially if China takes a breather, but we don't know if a return to $25-30 oil is as likely as the contrarians think could happen, at least in the near term. Julian Simon, countered the resource doomsayers of a generation ago, i.e. " Council of Rome", screaming about running out of oil, but we say the secular rise in the cost of energy is less about scarcity doom and more about recent imbalance between capacity and upcoming demand. Demand is only going to grow in the younger, growing segments of the world, notwithstanding hiccups in China as Hu Jintao and his coterie assume the reins completely after Jiang Zemin's step-down from his final post as head of the Chinese military and focus on maintaining growth sustainably. Alternative future sources of energy, such as the nuclear pebble-bed technology we mentioned, fuel cells and hybrid cars (and the wild idea of mining off-shore continental shelf deep-sea hydrate deposits) notwithstanding, we think the demand for black gold, and its fellow hydrocarbons will just keep growing.

A 25-year old company based in Alberta, Suncor's claim to fame lies within its Suncor Energy Marketing Inc. (SEMI) subsidiary. SU gets, develops and sells hydrocarbons, trades it, resells it for others, but the reason most people stand up and take notice right now is its oil sands business. Here bitumen, the low grade energy product extracted from Albertan oil sands are drawn out as the sand is mined, crushed and then converted into this slightly higher grade hydrocarbon. It has taken decades for the development of process just to get the cost of making a barrel down to $10. While its cheaper and easier to get a barrel in Saudi Arabia, the counter-argument is this tough as heck to extract energy is from a still friendly neighbor sitting on a reputed equivalent of a trillion barrels of oil. (It takes quite a few tons of oil sand to make one barrel, but it can be done.) Recently SU has been buying bitumen from others via its Firebag operations for processing too.

We read that Suncor's reserves are carried at about $20+ a barrel on the books and that sounds " cheap" given that recent oil prices hover around $45+ or so. No matter how sludgy the sand is in Alberta, it comes from a country that is been America's neighbor and closest trading partner. Let's show these guys respect and stop calling them the "51st state". The problem is everyone knows this and we may end up writing about the contrarian possibilities of shorting the sector, and we're not trying to have our cake and eat it too, (or is that barrel of oil and burn it too), but we focus on both ideas and application, like it or not. The Baltic Dry Index, the tool which we used to guide our caution about tanker stocks, which afterwards reversed strongly to our regret, points in this direction recently. Perhaps we'll get this "wrong" too, as we did when we anticipated a downturn in those shares, and the Baltic index will promptly dip and then drop.

Source: www.maxmart.com.tw

Given the activity of late, we are disquieted but our observation in a mid-May 2004 issue of our Market Note, of Felix Zulauf's speculation that $60 oil was possible by decade's end, while sounding amazing, has sounded less amazing in recent months and may occur sooner than later.

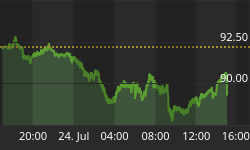

A quick chart of SU, a company we plan to explore for deeper drilling, is offered.

Alberta, CN

| Market Cap: | 13B+ | Operating Margin: | 20%+ |

| Trailing P/E: | 18 | Net Profit Margin: | 14%+ |

| Price/Sales: | 2.3 | ROA: | 9.9%+ |

| Price/Book: | 4 | ROE: | 26%+ |

| EV/Sales: | 2.7 | Debt: | 1.9B+ |

| EV/EBITDA: | 8.6 | Debt/Equity: | 0.6 |

| 52 Wk H | 30.00 | Aug-04 | |

| 52 Wk L | 18.30 | Sep-03 | |

| Shares Outstanding / Float | 452.9M / 448.4M | ||

The demand for energy points to demand for other things as well, like the means to turn the juice into "juice". The destination for much of the thicker crude will be power plants, and that with global trends including a demand for more of these facilities, which means more construction. We can think of many ideas, but we'll just pick one and run with it for a little while. Again it is just an idea, among many, and it's just an example ABB (Asea Brown Boveri). Yes, that's right. Last year this might have made the contrarian note list, but now that the debt and asbestos issues sort of recede for now, to our point of view, we see the prospects for the moneymaking aspects of this idea for a long. There are likely better ideas, but this is the one we've "anchored" to, as a behavioral economist/trader might say.

ABB Limited describes itself as a player in power technologies that help utility and industry institutions raise performance with improved environmental impact. A little over 18 months ago, ABB reorganized its operations along two lines, Power Technologies and Automation Technologies, with the former selling to utilities and industrial clients and the latter selling products and services for improving production processes. It all boils down to selling pick-axes and shovels to the miners. Clients of ABB's have included GE, Honeywell, Siemens, Altstom, among others involved in power systems. Let's take a look at a chart for ABB, another company we plan to keep plugged into. Yeah, we're crazy, and maybe it will only get a popup from the recent overall rise in shares since the bounce from July/August 2004, nevertheless we can't help but notice the potential of these shares, so lets use our equity risk controls in place and consider the trade. In closing, we also have noticed recent noises made by the company to make it-self better known in the markets, in a recent September 17, 2004 press release, to make itself better known in the US business and consumer market with a print and broadcast advertising campaign.

Zurich, Switzerland

| Market Cap: | 12.5B | Operating Margin: | 4.9%+ |

| Trailing P/E: | 33+ | Net Profit Margin: | 2%+ |

| Price/Sales: | 0.66 | ROA: | 1.4%+ |

| Price/Book: | 4 | ROE: | 13.5%+ |

| EV/Sales: | 0.8 | Debt: | 6.1B |

| EV/EBITDA: | 15.5 | Debt/Equity: | 2 |

| 52 Wk H | 6.50 | Feb-04 | |

| 52 Wk L | 4.60 | Dec-03 | |

| Shares Outstanding / Float | 2.06B/1.69B | ||

Brief caveats about our energy trend stance - which is in keeping with our "Often in doubt, but sometimes right" bias. An opposing view from another chief exec, Lord Browne, of BP, which we noticed in a recent Financial Times, was that "there isn't really a supply crunch at the moment. We have the perception of risk of a supply interruption, but that's all we've got." Addressing the sovereign risk implications of new sources, Lord Browne told the FT, "I think oil is coming from places [people] don't understand. They take the view that, 'they are not regimes like us." We take from this that the point is that Lord Browne's assertion is there will be sources that will come on line and change the market's perception of supply. In addition we read that while it seems speculators and hedge funds have taken cover and closed some long positions, they may have merely obscured their involvement, hence lowering reported CFTC open positions - this may or may not be true. The runaway train that is Chinese demand, one of the two engines that drive global demand, may indeed be under the brake, as central authorities continue to rein in regional and banking agents unaccustomed to adhering to credit risk management practices. If the prospects of recovery for US and developed economies, the second engine of global demand, is more under-whelming than hoped for, then not only is the outlook for the markets in 2005 less brilliant, such would indeed be the case for intermediate and longerterm profits from energy speculation. These broad strokes cover dangers of our long stance. We close this Trend Note, with our usual apologies and small print disclaimers. Until next issue.