A Dog: Yellow Lab, Most registered 2009 AKC, per wikipedia.com

To the right is a picture of a dog. In order to simplify this discussion in such a way those even Silver momentum traders might understand it, we have placed a circle around the approximate location of the dog's brain and a rectangle around the tail. At this point, we should all be together.

Control center for dog is the brain, see circle. An appendage named tail, see rectangle, is controlled by the dog's brain, see circle. Control mechanism runs, see arrow, in one direction, from circle to rectangle. It does not run other way. The tail does not wag the dog. Even though these times are widely claimed to be different, a bright man once reminded us that God, your choice, does not allow randomness to operate brain-tail function of a dog.

Silver coins were created to fill a void left by Gold coins. Imagine a world with only one issue of currency, a $1,390 bill. How well might that work at the local food store? What if one only needed a carton of milk? One would have to buy $1,390 worth of milk or pay $1,390 for one container of milk. Such a situation illustrates the utility of a Silver coin worth much less. It is the Gold coin, however, that gave the Silver coin both utility and value. Silver coins were the "poor man's coins". Gold in this case, the provider of utility and value, is the dog. Silver is the tail.

Spurred on by spurious stories of Silver shortages by Silver conspiracists, Silver moved above the most recent highs. While not yet sure if this is a breakout or a triple top, the Silver market, the tail, moved higher. After Silver added an irrational 3% in one day, Gold, the dog, followed the tail higher.

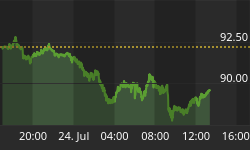

Above chart is of the approximate market prices for Silver futures(17 Feb) going from spot out to December of next year. As is fairly evident in that chart, the price pattern has a negative slope. Silver for delivery tomorrow is cheaper than Silver for delivery today. This set of price relationships is referred to as backwardation. It represents normal market conditions.

No shortage of supply is necessarily indicated by this price pattern. That today's price is higher than tomorrow's price might mean that demand is especially strong today or that supplies tomorrow will be more than adequate. It does not necessarily mean that shortage exists. Markets relationships show no indication of shortage tomorrow for Silver.

More important perhaps than this particular set of Silver pricing relationships might be how it got this shape. The Financial Times has been reporting( 9 February & 15 February) on the massive sales of Silver into forward markets by non primary Silver producers. Their estimate is that roughly 100mm ounces have been sold forward. Relative to estimates of the historical size of the Silver hedge book this would make today's forward sales at or near a record.

Given the wisdom of selling Silver production forward at current prices, we should reasonably expect that non primary Silver producers will continue forward sales. The Silver market seems willing to digest such sales today largely due to the mania level of speculative activity. How those holders of contracts for future delivery react in the coming year as that Silver is delivered is likely to be interesting. Are they ready for the trucks to back up and start unloading?

| US$GOLD & US$SILVER VALUATION Source: www.valueviewgoldreport.com | ||||

| US$ Gold | US$ Gold % | US$ Silver | US$ Silver % | |

| Current | $1,392 | $32.84 | ||

| Long-Term Target | $1,810 | 30% | $32.75 | 0% |

| Over Valued | $1,108 | -20% | $20.04 | -39% |

| Fair Value | $852 | -39% | $15.42 | -53% |

| Sell Target | $1,970 | 42% | $35.50 | 8% |

Our current summary of Gold and Silver valuation is provided in the above table. While valuations are indeed somewhat more alchemy than science, they do force a discipline onto the investment process lacking in many approaches. Further, over or under valuation does not say a market will rise or fall. However, over valuation has been regularly shown to be a precursor of market adjustments to prices when price is too far out of proper relation to fundamentals.

As is readily evident in that table, Silver is over valued and approaching price levels where a reduction in exposure might be warranted. In particular, given the relative valuations, a swap of Silver into either Gold, or possibly Rhodium, is probably appropriate. Naturally such a move should be in part dependent on the size of Silver holdings relative to an investor's total portfolio. Those over weighted in Silver are most at risk, and should begin shifting their portfolio.

In short, one question arises. Are you going to manage your precious metals, or is the dog's tail?