If you like trading, as opposed to investing, then these are markets for you. Commodities markets dropped sharply last week, recovered, and then a number of them dropped again today. NYMEX Crude, which had been flirting with $105 yesterday, pierced through $98 today before closing at $99. NYMEX Unleaded had recovered almost all of its loss from last week before plunging nearly25 cents today.

Attempts to explain these moves as the natural product of any rational process are bound to be frustrated. Of course, we try. Bloomberg tried by stating (early in the day) that "Commodities fell for the first time in three days, led by gasoline and silver...as reports on inflation from London to Beijing boosted expectations for higher interest rates." While there was definitely discussion of the i-word in both of those capitols, it is a bit of a leap to suggest that commodities markets are starting to price hawkish central bank policy when the very interest rate markets are not. I guess you gotta write something! After the weekly inventory numbers came out, showing a higher-than-expected build for Crude and Gasoline (but a draw for Distillates), the stories changedto attribute the plunge to the "surprising rise in supplies."

A 7% move in Gasoline doesn't happen because of a surprising weekly build. It's a weekly number and it bounces around some, like Initial Claims. More importantly, this hypothesis doesn't explain why Silver dropped 8.4% again today, or why Sugar was off 4.25%. And it doesn't explain why stocks dropped1.1%, or 10y notes rallied 5-6bps (to 3.16%).

Blame it, if you wish, on a sudden "risk-off" trade. At least that is consistent with the movement in the markets (although I always wonder why TIPS are considered "risky" instruments since they are considerably safer than Treasuries if held to maturity). But now we have just pushed the explanation back one layer. What has triggered the "risk-off" trade? Bombing in Libya? The fact that Greece is in trouble? The rising temperature of unrest in Syria? Hey, I can agree that all of these things make me nervous, but none of them is particularly new. Besides, as of this morning the Wall Street Journal was running a piece saying that anew deal for Greece is expected...by Greece...by June.

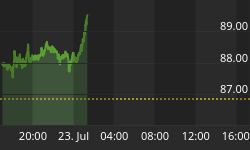

The dollar rallied today, to its highest level in a month. It isn't clear to me if this is effect (another 'risk-off' reaction) or cause. You can make a plausible argument that it is the latter. Perhaps traders are covering short-dollar bets because the Fed is nearing an end of QE2 and, whether they now start selling out the portfolio or not, the transition to at least not buyingis effectively a tightening of policy and arguably could strengthen the dollar. This would tend to weaken commodities, and to the extent that monies are coming back into dollars it would tend to support fixed-income. If this is really the root cause, then it's probably mostly out of gas...unless the buck breaks above big resistance at 76 on the dollar index (see Chart below).

Nice dollar bounce, but the going is about to get tough.

If that happens, then there may be more near-term downside to commodities and stocks and upside to bonds. I don't expect it, but the recent volatility sure makes it seem a dicier proposition than I thought it was a couple of days ago. Several commodities are at supports, the 10y Treasury note is back testing its recent highs, and stocks are re-testing the February and April highs, which they pierced through late last month. The proximity of so many critical points makes the situation inherently less stable. And yet...the VIX is still way down at 17. The MOVE is still near multi-year lows (see Chart below). Protection is quite cheap.

MOVE index of fixed-income volatility is near multi-year lows as well.

But inflation protection is still not cheap. While 10y TIPS sold off to 0.72% today, that remains a very expensive level. How then does one protect against inflation in this environment?

I continue to be a fan of commodity indices, but institutional investors should consider high-strike payer swaptions here. Some readers will remark that this is not a fresh idea, since that has been the default strategy for many institutions for a while. So let me be clear: while that has been a default strategy for a while, it hasn't been the right strategy for a while. Here's why. When you buy an interest rate option (for the uninitiated, a 'payer' swaption gives you the right to pay a fixed rate on a swap at some point in the future, so it is analogous to a bond put), you're paying for protection against increasesin both real rates and in inflation. Remember, Fisher told us that

Nominal rates ≈ Real rates + expected inflation (+ risk premium)

So when you buy an option that pays off if nominal rates rise, you win if real rates rise, if inflation compensation rises, or if they both rise. Andyou're paying for all of those possibilities.

But when this strategy was first being proposed, in mid-2009, real rates were much higher (especially on a forward basis). So nominal rates were not very likely to rise because real rates were rising; they were going to rise, if at all, because expected inflation rose. But you were paying for both pieces of that option. In the event, expected inflation rose and real rates plunged, so you're further out-of-the-money now than you were then. Moreover, impliedvolatilities were very high.

Now, by contrast, implied volatilities are very low and so are real yields. It is unlikely that, if inflation starts to rise, real yields will fall much further than the 0.72% where they already sit. So you're paying less, and getting more. Now, even if what you want is protection from inflation and not from nominal rates, at least you're more likely to have the movingpieces going in your favor, rather than against you.

The same reasoning applies if you are a retail investor, except that there are not many options for the retail investor who wants to buy a long-term option on inflation, or nominal rates, or almost anything for that matter.

.

On Thursday, we get another volatile weekly supply number. This one is the supply of new jobless, also known as Initial Claims (Consensus: 430k). Recall that last week saw a spike to 474k, which even though it had some reasonable explanations attached to it was still shocking for many observers. If that figure doesn't drop substantially, bonds are going to go straight up and stocksand commodities straight down.

Retail Sales (Consensus: +0.6%/+0.6% ex-autos) is also an 8:30ET number. Be careful here as well. Anecdotal reports seem to suggest a chance of weakness to what has been a consistently strong number for almost a year now. Unusually, this is probably less important than Claims in the mind of the investor right now, but weakness here and in Claims is where to look for market risk tomorrow.

Also out is PPI (Consensus: +0.6%/+0.2% ex-food-and-energy). Core PPI is expected to rise to 2.1% year/year and the headline to 6.5%. PPI doesn't matter, and especially since it is sharing the 8:30ET time slot with Claims and RetailSales it will be mostly ignored.

.

Two administrative notes:

1) If you missed my column the other day on the kurtosis and skewness of commodity indices and the importance of that fact to traders in these things - it was mis-posted in one place you may have ordinarily seen it - please havea read.

2) I finally finished an inflation-related paper that I had been working on for a long time. A few years ago I submitted it through a couple of rounds to a journal and never got it cleaned up enough to be published, but it's cleaned up enough to put on SSRN. The paper is called TIPS, the Triple Duration, and the OPEB Liability: Hedging Medical Care Inflation in OPEB Plans. If you have a role in hedging medical care exposures in post-retirement liabilities, take a look and remember that Enduring Investments can behired as a consultant.