In 2009 and 2010, the Federal Reserve was able to reverse sharp declines in asset prices by pumping large amounts of printed money into the global financial system via quantitative easing. With the Fed's 2011 Jackson Hole speech set to take place on August 26, we recently reviewed the ETF winners from QE2 looking to see if the market is anticipating the launch of QE3. Like the bearish similarities to 2008, our findings below are not encouraging for the stock market bulls. A recent review of QE2 winners indicates one of two things:

- The market does not believe the Fed will announce QE3 in the coming weeks or

- The market believes the deflationary forces in the economy are so great that QE3 would have little impact on asset prices.

The Fed clearly telegraphed their intention to implement QE2 during Ben Bernanke's remarks at Jackson Hole on August 27, 2010. Our March 2011 analysis of QE2 winners showed that silver (SLV) prices responded by gaining almost 90% from August 2010 to March 2011. The table below was originally presented in March 2011.

The 2011 Jackson Hole remarks from the Fed are scheduled for August 26; last year they were given on August 27. This year the financial markets peaked in early May; last year markets were also topping out in May, which means we have similar conditions coming into this year's Jackson Hole remarks as we did in 2010.

The chart below shows silver (SLV) nine calendar days before the Fed's 2010 Jackson Hole remarks. Notice how the markets were anticipating market-friendly news, indicated by silver's higher low made prior to Jackson Hole 2010.

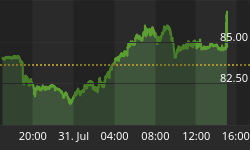

The chart below shows silver ten calendar days before Jackson Hole 2011. The chart of silver looks better today than it did last year. You might be tempted to say the markets are front-running the Fed anticipating another Jackson Hole miracle for asset prices. Unfortunately for the bulls and the global economy, the rest of the QE2 investment winners do not support another QE miracle save from the Fed.

The price of oil is obviously economically sensitive. In a world where central banks have their printing presses working overtime churning out paper currencies, oil also serves as a de facto currency (similar to gold). Last year, nine calendar days before Jackson Hole, with the financial markets teetering on a fine bull/bear line, oil equipment & services stocks (below) were showing some signs of life, which indicated hope for better economic outcomes and an anticipation of QE2.

In 2011, ten calendar days before Jackson Hole, oil equipment and services stocks look significantly weaker sending concerning signals about the economy and the possible effectiveness of any further quantitative easing (QE3).

The entire energy sector (XLE) had clearly made a higher low and higher high prior to Jackson Hole 2010, which aligned with a more optimistic outlook for asset prices and the economy.

Heading into Jackson Hole 2011, energy stocks seem to be favoring weak economic outcomes, which is another reason to have cash, precious metals (GLD), and bonds (TLT) on hand.

Coal stocks (KOL) were firming up in 2010 as the Fed put its finishing touches on their planned Jackson Hole remarks.

At a similar point in 2011, coal stocks, a big QE2 winner, look decidedly weak.

Traders, anticipating the possible impact of QE2, piled into metals and mining stocks (XME) nine days before Jackson Hole 2010.

In 2011, traders seem to be avoiding metals and mining stocks, suggesting they do not anticipate a lasting impact from any Jackson Hole remarks.

Natural gas stocks (FCG) gained almost 50% after Jackson Hole 2010. Nine days before the 2010 conference, signs of a new uptrend were appearing in the sector.

Today, a firm downtrend remains in place in natural gas-related stocks, which seems to question favorable economic forecasts.

Some Fed front running in natural resource stocks (IGE) appeared to take place in August of 2010.

Few signs of front running appear on the current chart of natural resource stocks.

Agricultural commodities (RJA) were anticipating future inflation in 2010, which indicates traders had faith the Fed's printing press could reverse deflationary trends.

The prices for agricultural commodities look very deflationary today; they show little faith in the Fed's ability to re-inflate in the second half of 2011.

The Russell 2000 Growth Shares ETF (IWO) gained over 40% after Chairman Ben Bernanke's 2010 Jackson Hole speech. Traders began building positions ten days prior to Ben's remarks.

Whatever the Russell 2000 is currently anticipating, it does not appear to be bullish or asset-price friendly.

The ever-volatile semiconductor sector (SMH) also painted a picture of some hope heading into Jackson Hole 2010.

Ten days before Jackson Hole 2010, semiconductor stocks seemed concerned about consumers opening their wallets in the coming months.

Like the vast majority of QE2 beneficiaries, the private equity ETF (PSP) was firming up nicely in the summer of 2010.

Today, private equity's chart has that decidedly waterfall-like look of so many charts.

In the summer of 2010, global financial markets were sitting on a fine bull/bear demarcation line as we outlined in this August 15 video. The Fed's August 2010 Jackson Hole speech telegraphed the central bank's intention of launching QE2. The impact on asset prices was dramatic in 2010. Even if QE3 is announced, the impact may be much more muted in 2011. Our 2011 Jackson Hole strategy is to review the Fed's remarks with an open mind. We will also review the market's response with an open mind, but as of this writing, our bias heading into the Fed's annual summer conference will remain defensive and bearish.