I start today with a couple of simple news items that I think speak volumes. However, in my normal fashion I will then write further volumes.

-

"India Plans to Sell Inflation-Linked Bonds, RBI's Subbarao Says" - India last sold inflation-linked bonds (ILBs) in 1997 - a 5-year issue. India hasn't decided when they will start selling the bonds, but RBI Governor Subbarao said "We will think through this but we will certainly reintroduce them."

-

"Germany Suspends Inflation Bond Sales on Better Budget Outlook" - Germany, which has about €52bln in ILBs outstanding (about half of what Italy has), is going to put its regular sale "on hold" this quarter. The German Federal Finance Agency says that this is partly due to the improving budget outlook (apparently, they haven't caught on that there are a few - ahem - extra budget costs queuing up), and partly because in the words of the article "Investors' appetite for the bonds has also diminished." Obviously this is true...you can tell by the huge real yield of -0.17% that the 5y German ILB bears. The 10-year is even higher at 0.19%!! Clearly, the demand is very light for these bonds, right?

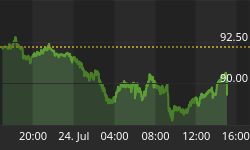

As additional commentary in the "one picture is worth a thousand words" category, see below the Indian inflation trade (in red) and the German inflation rate (in white). One of these wants to issue inflation-linked bonds; one has abruptly decided not to issue any more right now because they don't need the money and besides, no one wants them.

One of these countries evidently believes their inflation is going to go down.

One is less sure.

Hmm. I would say 'draw your own conclusions,' but let me take you one more step.

Emerging economies issue ILBs for two main reasons. One is that many emerging markets cannot access the debt markets without indexing principal, since they have a history of devaluing the currency they pay back the bonds with. The other reason is that they want to indicate a seriousness about getting inflation under control, since clearly their interest payments will be less in nominal terms if they can restrain inflation.

Developed economies can stop issuing ILBs for a number of reasons, including an outstanding budget situation with projected surpluses and lack of investor interest. But if I was in the national Treasury, watching inflation crawl higher, and realized that I wasn't in control of the money-printing process, then unless I had to raise as much money as possible (the situation the U.S. is in, by the way) I might consider whether inflation-linked bonds were the best vehicle.

.

The bond market today roughly broke even, which is a fairly weak performance considering that the stock market started the day plunging. Equities were trying to catch up with the 2-day decline in Europe, and doing a darn good job of it until the S&P hit the upward-sloping trendline off recent lows (and parallel to highs of the recent consolidation, forming what looks unfortunately like a 'flag' on daily charts) and began to rally back. The net result, a loss of only -0.7% on fairly light volume - by recent standards - of around 1bln shares, was positively heart-warming and the market continued to rally after the close.

This may be premature. The German Constitutional Court is due to rule on Wednesday (that's after I post this at http://mikeashton.wordpress.com and release it on Twitter as @inflation_guy but possibly before it appears in syndicated channels) on whether the bailouts of Ireland, Portugal, and Greece that were financed by the European Financial Stability Facility are illegal. The consensus is that the court will not declare it to be so, but the consensus appears to believe that simply because it would cause unfathomable chaos almost immediately. A bailout mechanism without Germany is not a bailout mechanism, it's a bunch of drowning people fighting over a single life preserver. But even if the consensus is correct, that doesn't mean the court will not greatly limit the prospective participation of Germany in the future, or at least limit the ability of the Chancellor to make bailout decisions essentially unilaterally.

That event is the key to tomorrow's trade, and it will be done before we wake up.

While bonds ended the day today near-unchanged, and stocks ended much closer to unchanged, TIPS got painfully smacked. The 10-year TIPS yield rose 8bps, and with unchanged nominal yields that produced an 8bp decline in 10-year breakevens. This means 10-year inflation swaps, illustrated in the chart below, are at the lowest level they've seen since the last growth scare, which not-coincidentally preceded Bernanke's Jackson Hole speech and the proposal of QE2.

10-year inflation swaps from Bloomberg.

The yield here is in basis points, so 231 is 2.31%.

This strikes me as borderline crazy, but only borderline. If the growth data continues to do what it has done, then there will be better opportunities (finally) to buy TIPS and to go long inflation at dumb levels again. The 10-year inflation swap had much more business being around 2% before QE2 was launched than 10-year inflation swaps have being around 2.30% with a US QE3 being debated, QE preparing to launch again in the UK, the Swiss National Bank pledging to sell unlimited Swissy (which is an ease unless sterilized, which it doesn't appear to be), and the ECB buying bonds (and sterilizing imperfectly at best). However, investors insist on believing that inflation is related to growth, and inflation quotations could go significantly further south if there is a debacle in Europe.

Let's hope there's not a debacle, but that we get a chance to buy TIPS and inflation swaps cheaply again!