Since the Fall of 2008, Ben Bernanke and his co-pilots at the Federal Reserve have loaded around $1.8 trillion of paper money, or its electronic equivalent, on helicopters, dirigibles and whatever other flying machines they could find. Yet despite all the monetary aviation, very few pieces of the funny green paper called Federal Reserve Notes have fluttered to the ground.

So much for hyperinflation! What went "wrong"? More importantly, what is helicopter Ben going to do about it (next)?

What went "wrong" is simply that the Federal Reserve can print all the money that it wants but it cannot make banks lend or the private sector spend. We could discuss various methods for measuring money supply or inflation but let's just cut to the chase: ![]() total credit market debt in the United States stood at $52.4 trillion at the end of 2008 compared to $52.6 trillion earlier this year. That's a stagnant credit market at best with the figures arguing against inflation regardless of how it is measured or defined.

total credit market debt in the United States stood at $52.4 trillion at the end of 2008 compared to $52.6 trillion earlier this year. That's a stagnant credit market at best with the figures arguing against inflation regardless of how it is measured or defined.

Yet we think our Fed chief still has some tricks up his sleeve. QE1 and QE2 - so-called quantitative easing that literally increases the quantity of monetary base -- consisted primarily of the Fed expanding its balance sheet by monetizing the federal deficit. These were helicopter drops, simple as that. Let us make a mental note that helicopters are slow flying machines that specialize in transporting things from place to place; the Fed uses them to transport securities from the banks' balance sheets to the Fed's balance sheet. In these transactions, the banks are essentially acting as middlemen since the Fed cannot bid directly at Treasury auctions. Excess reserves are flown back in exchange.

QE3 we suspect is going to consist of the Fed coaxing banks into expanding their own balances sheets by monetizing the federal deficit. This may also involve the Fed swapping some of its assets - for example Treasury securities maturing in 1 to 5 years - for bank assets of lower quality, thereby improving the banks' regulatory capital ratios. Then again, Standard & Poor's is rating a subprime mortgage-backed security AAA after having downgraded U.S. debt to AA+, so who the heck knows what "quality" means anymore?

In any case, the difference is subtle but important. QE1 and QE2 had the effect of increasing the quantity of money; QE3 will focus on increasing the velocity of money. The "Q" in QE3 will likely be "qualitative" instead of "quantitative".

So it turns out Helicopter Ben might no longer need those slow choppers; he'll want something instead that can make money fly fast. Thus the arrival of QE3 could usher in a new central banking legend: Fed Bennie and the Jets.

Say, Candy and Ronnie, have you seen them yet?

But they're so spaced out, Bennie and the Jets

Oh but they're weird and they're wonderful

Oh Bennie she's really keen

She's got electric boots, a mohair suit

You know I read it in a magazine

Bennie and the Jets

Some people might prefer this subtlety-free version but we think the classic is sufficiently apt: QE3 will be weird and wonderful ... just like the 1970s! What's that? You don't think Bennie's really keen? Wait until you see the wild, destabilizing swings that are in store under QE3! They could make QE1 and QE2 seem like a kindergarten re-enactment of the chase scene from Bullitt.

Specifically, during QE1 and QE2 the Fed was in full control since it could determine when and what securities to buy. Moreover, the Fed was prepared to freeze all of the excess reserves it had created. This could be accomplished simply by increasing the interest rate paid on those reserves. By contrast, QE3 will likely feature the banks deciding for themselves when and what securities to buy while the Fed tries to maintain some semblance of remote control as a sort of monetary puppet master. Or more aptly, that man behind the curtain. So it's "Fed Bennie and the Jets of Oz" then!

Seriously though, the risk with QE3 will simply be that $1.6 trillion of excess reserves are now held by the banks. These excess reserves represent the "electronic equivalent" of Federal Reserve Notes created by literally running the printing press. Excess reserves are high powered money because there are no bank liabilities associated with them and therefore they can be fully leveraged under a fractional reserve banking system. Each dollar of high powered money can generate at least 9 dollars of deposits and in some cases an infinite amount.

The expansion in bank balance sheets, however, is not by itself what should worry us. There is a limited amount of uses to which banks are likely to put excess reserves in the near term - mainly shorter-dated U.S. Treasury securities in the 2, 5 or 7 year maturities. Therefore the banks are unlikely to expand their balance sheets at a pace much faster than the U.S. Treasury Dept. will be issuing these maturities during its weekly auctions in the future. As already mentioned, the Fed can also boost the pace at which excess reserves are leveraged by the banks. Doing so would involve a qualitative easing whereby the Fed exchanges Treasury securities maturing in 1 to 5 years that it owns for various assets that the banks are (more) loath to own. Still, if credit continues to contract in the private sector, the monetary system will essentially be treading water.

The worry, rather, is about systemic stability. When high powered money goes from idle to circulating, it is impossible to control its initial velocity. Normally the majority of high powered money consists of paper currency held by the public. The public changes its savings preferences slowly over time -- for example, deciding to stuff some money under the mattress just in case. This results in gradual changes in the velocity of money in part because relatively small sums are involved - a few billion dollars here and there.

The banks, however, don't have preferences that change slowly over time when it comes to excess reserves.In fact, they have absolutely no reason to keep excess reserves on the books if they can instead buy assets that earn a superior yield and still are sufficiently liquid and safe. So while the amount of assets that are appropriate for banks to buy with excess reserves might be in limited supply, the nature of excess reserves once un-moored from frozen idleness is very much that of a hot potato - nobody wants to hold on to it but somebody has to. Indeed, it is the hot potato effect that allows even a small temporary addition or draining of reserves (a mere few billion dollars) to have a large effect on bank lending and money markets during normal times.

But clearly we are not in normal times with $1.6 trillion of excess reserves sitting on the banks' books. If only a few billion dollars of these reserves were to become "hot potatoes", the Fed would need to scramble in a very expeditious manner to prevent collateral damage in the money markets or elsewhere. What would the Fed need to do if the hot potato was a cool $100 billion? $1 trillion? One limited course of action would be for the Fed to drain its own balance sheet in order to sterilize hot potato reserves - for example by trading away the aforementioned Treasury Notes maturing in 1 to 5 years. But that can only go so far (specifically as far as the Fed owns the right assets to be traded away). If the banks refuse to buy whatever the Fed decides to hock after exhausting its supply of the good stuff, what then? We don't know, and we don't want to find out.

Importantly, we believe the initial preparations for a round of "jetting around in Oz" have already been made by Bennie under the pretext of extending zero short-term interest rates indefinitely (or at least until mid-2013). The crucial result of this monetary accommodation is the elimination of duration risk from most short- to medium-term debt. Duration risk is simply the risk that the market value of a bond yielding a fixed rate of interest falls as interest rates rise. With short-term rates already near zero and the yield curve at historic lows, duration risk is one of the key considerations for managing bank balance sheets. In no uncertain terms, duration risk was a key reason why the banks sold assets in the first place to the Fed under QE1 and QE2 in exchange for excess reserves. Eliminating duration risk could therefore start to thaw some of the currently-frozen excess reserves, even if just at the margin.

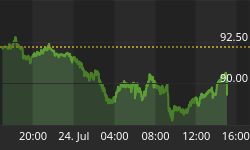

Indeed, we need only point to the massive $100 billion (roughly 16% in one week or 830% annualized) jump in demand deposits between July 25 and August 1 as a proof of concept for our "Fed Bennie and the Jets of Oz" hypothesis. Along with recent wild moves in the Treasury markets that have made even Bill Gross of Pimco blush, this is precisely the type of action we expect to regularly see going forward as excess reserves thaw out and enter circulation in dribbles from a dead stop to terminal velocity in a matter of moments. Several days of raw volatility will then be followed by weeks of relative calm as the monetary shifts and imbalances resulting from banks passing the hot potato are gradually sorted out. And then, bam! It happens again. And again.

Other things we expect, or at least wouldn't be surprised, to see as QE3 unfolds:

-

Extreme volatility with an upside bias in the gold market and to a lesser extent in silver, commodities, emerging markets, hard currencies and hard assets;

-

Large daily or weekly (5 to 10 full points) moves in Treasury prices followed by long periods of chart consolidation as the banks monetize the federal deficit in fits and starts while the Fed desperately attempts to assert some control from behind the curtain using the repo market and other levers at its disposal;

-

A liquidity trap or two requiring emergency action as the payment system freezes up during wild swings in Treasury and money markets, during which periods we may see short episodes of "all-market selloffs" similar to, but not nearly as severe as, late 2008;

-

Inflationary pressures to start building by the end of this year or early next; at first slowly and then accelerating as it becomes obvious to the market what the Fed is up to (we note that economists at JP Morgan and other investment houses have probably figured it out already, leading to their bullish calls for $2,500 gold);

-

No hyperinflation as overall growth in credit and economic activity remain anemic, resulting instead in stagflation similar to the 1970s;

-

The U.S. dollar remaining in its multi-year trading range as credit contraction places demands on its legal tender status for settling all debts, public and private;

-

A tough go for equities in general with a few bright spots especially in the resource, technology and alternative energy sectors.

We'll have much more to say on this topic in the future including a look into several other factors to watch out for as well as what reports and indicators we are monitoring to assess the progress of QE3. Meanwhile subscribers will receive exclusive insights such as ideas for gold stock investing and speculative plays such as the call options that we recently parlayed into 2000% to 5000% gains.