China doesn't really have all the money in the world. It just seems like they do.

From what I can tell, the Chinese - at least, if the rumors are to be believed - are supporting the dollar, supporting the stock market, and supporting the Italian bond market. The notion that China, despite the awesome size of its foreign reserves, can meaningfully affect every financial variable that someone needs to go up, is implausible. China enjoys some $3.2 trillion of foreign exchange reserves, according to this article on Wikipedia, but it is thought that about half of that is in U.S. securities and there has certainly been no sign that the PRC has been selling bonds and dollars! If we assume that half of the balance is in Europe and half in the rest of the world, that brings us to $800bln of Italian bonds that they could buy if they spent every Euro on Italian bonds. This seems grossly unlikely, since they would need to sell lots of other Euro bonds in order to do so. What is a 'large purchase' that doesn't involve them selling lots of other bonds? $50bln? While that is a huge sum, Italy has around $1.6 trillion outstanding according to Bloomberg (do BTPS 2 06/01/13<CORP>DDIS<GO>, and be sure you're picking the top-level issuer), and I suspect that there are easily $50bln in sellers. So, while that news was good for a 2% rally in the S&P over the last half-hour of trading, I wouldn't think that sellers of BTPs will suddenly decide to hang on because the Chinese are bankrolling the Coliseum....even if it turns out to be true.

I also wonder at the fact that the focus seems to have shifted to Italy now. Does that mean everyone has given up on Greece, Portugal, and Ireland? Surely no one thinks those problems have gone away, and the collapse of the banking system in Europe is definitely not 'priced in.' China can't buy everything. (Frankly, if I was China I'd keep my powder dry to buy, combine, and recapitalize Euro banks into a Sino-European Bank, although it isn't like China's track record with banking systems is very good given the state their own is in).

Maybe stocks have one more bounce in them before we plumb new depths, but somehow I don't think so - because Greece doesn't seem to have any bounces left. As a summation of the current situation I can't do better than what my friend Pete Tchir wrote today so I'll simply quote it verbatim:

"You know the first time someone plays poker they are afraid to bluff. The second time they decide bluffing is great. By the third time they are so confused about who is bluffing and when that they might as well just hand their chips to the best player at the table and save everyone the time and effort or taking the chips. I think the central bankers and governments have gotten so confused they are bluffing with a few low off suit cards and don't even realize the cards are face up. A few polite people are choosing to ignore the cards. The governments and central bankers may still win but it will all come down to the luck of the draw since the odds are stacked against them."

I concur. And I think we're in the final round of betting.

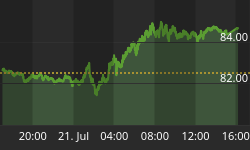

And that probably means also that US rates have more downside (remarkably) and the dollar may have more upside after breaking out of a 5-month-long consolidation zone. As you can see from the chart below, such a 'breakout' is by itself not a significant event in the context of the volatility of the last few years. However, it does have the effect of postponing the worst of the possible idiosyncratically inflationary outcomes for the US. The translation of foreign exchange movements to core inflation is very slow (as in, more than a year or two), but the worst outcomes for domestic inflation involve a sharply lower greenback.

The breakout is micro-important but not macro-important except to defer the downside.

Eventually, I would expect the dollar to respond to the increased supply of dollars relative to other currencies over the last few years and the relative dovishness of the Federal Reserve compared to other central banks. But right now, the probability of a sharp increase in the supply of other currencies such as Sterling, Swiss, and Euro is growing. Now, here's the rub for inflation. If the dollar is performing because our money-printers are being caught up to by foreign money-printers, then our idiosyncratic inflation (think of it as US inflation minus global inflation) will be lower, but global inflation will be higher. Unless, that is, the supply of money has nothing to do with the global price level. The "good inflation" outcome happens if all central banks are hawkish together. That will happen someday...hopefully before I retire in a quarter-century or so.

And here's the rub for China - when the world's central banks print more currency, it has an effect like the effect on current shareholders of a company issuing new shares. Spreading the same GDP over more units of currency represents a "dilution" of the value of the foreign currency China holds. So, while they may seem today to have all the money in the world, China in fact stands to lose more than any single investor in terms of purchasing power. I guess they may as well spend it, but in doing so they are enabling the money printing. Like large investors anywhere, they probably prefer the status quo to the risk that a change in the status quo is even less agreeable.