All you really need to know about what's important right now can be summed up in one chart.

Well, this doesn't look good. Italian 10-year yields.

That's the 10-year Italian government bond. While Greece still simmers with her problems nowhere near "solved," we may come to look with nostalgia on the days when we "only" had to worry about Greece. There are real-life market consequences associated with gratuitous "punishment" meted out to buyers of insurance. The gutting of the value of a CDS contract means that bondholders who might otherwise buy some tactical protection instead make strategic sales.

Of course, the evaporation of a bid for Italian bonds recently isn't merely due to selling pressure created when politicians arbitrarily took money from the insured (some of which are dirty, rotten hedge funds!) and handed it to the insurers. The Berlusconi government, which has almost always been better for entertainment value than for fiscal governance, is toppling. And yet, this itself isn't news. Berlusconi has been shaky for a month or two at least. The scary part is that it's not clear what happens if the situation in the market for Italian bonds doesn't improve.

They can't put together a very useful summit to assemble a financing package for Italy. That's the largest issuer of debt in Europe, and the third-largest economy. Oh, and should probably mention is has about €82bln of inflation-linked bonds outstanding, about 28% of the sovereign inflation-linked bond market in Europe. Investors on the Continent who want inflation-linked protection are about to start considering the non-Euro market more seriously.

The equity markets loved the fact that European governments are falling. I'm not sure why that is, but the S&P rallied 1.2%...and the Euro Stoxx index also rose 1.2%. It certainly can't be because of growth indicators in Europe, which continue to weaken, nor those of the U.S. which continue to bump along sideways ungracefully. It may again be due to the notion that stocks are inflation-protected assets (they're not, in any time frame that matters to most investors); the options for the central banks are narrowing and in the U.S. the "Evans Plan" of intentionally trying to inflate 'a little' is actually getting a serious hearing from otherwise rational people. It's great for an inflation specialist, but I'm not so sure it's good for the rest of you since there's no reason to think that more inflation would help people find jobs.

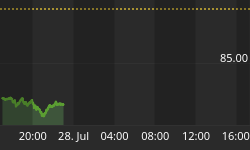

Commodities in this context have been rising, but rather tepidly if I do say so. Crude Oil is rising strongly, with NYMEX crude up from $75 a month ago to $97 today. That rise, at least some of which is due to the more-animated saber rattling between Israel and Iran, has not yet found its way into gasoline prices, but when it does...well, if nothing else it will reinvigorate the candidacy of Ron Paul. Whether that's a good thing or not I will leave up to you. Actually, I'm a little surprised that inflation markets are not better bid. The 10-year inflation swap, which had been as low as 2.15% early last month, is back up to 2.45%. This summer, though, it was pushing 3% (see Chart).

10-year inflation swaps, in basis points.

It seems like the year-end lethargy is already setting in. The equity market volume on Monday was the lowest since late July, and today only slightly higher. True, there were no economic releases, but can we really be shrugging off the Italian and Israeli/Iranian situations? Or has everyone already fully battened down the hatches? It doesn't seem likely that an Italian death spiral is fully discounted, but if it is then that's certainly bullish! Meanwhile, I am adding to my so-far ill-fated shorts in the Treasury market. At least I am getting good placement, so that I haven't lost money on balance since I started nibbling around a month ago (by buying TBF). But I'd like to see higher yields happen soon if they're going to happen. You can get a violent move in either direction when year-end conditions get thin, and I don't care to be on the wrong side of it!