It seems that, over the weekend, some investors had a case of indigestion after the cookie exchange late last week. Moody's did, and announced a review of EU sovereign debt ratings. Fitch followed later in the morning on Monday, so now all three major rating agencies are in agreement that the Euro summit was significantly less than decisive (at least, less than decisively positive). It is now quite probable that at least a few sovereigns will have ratings cut. Intrade (www.intrade.com) has a market on whether France will lose its AAA rating by June 2012; as of this writing, the last trade is at $7.70 (meaning the market sees a 77% chance). In other markets, Intrade participants put a 69% chance on Greece being rated as in default by Dec 31, 2012, with a 28% for Italy and a 20% chance for Spain. These numbers would surely be higher except for the technicality that we have all recently discovered, that a country could be effectively in default and not rated in default due to arcane rules that are carefully managed around by politicians.

And all of that assumes that the summit deal at least limps towards ratification by the main players. This is obviously far from assured for many of the countries involved, but even France's participation is less than clear. Grand-Plan Architect (and French President) Sarkozy is up for election in April (and May, as there are two rounds), and the candidate he is comfortably trailing in the polls said on Monday that if elected he would seek to rework the deal or simply not ratify it at all.

The partial thaw of last week's optimism trimmed around 3% from European stock markets, and sent the S&P down -1.5%. The dollar, not surprisingly, shot higher, and is again not far from 1-year highs. Commodities, which these days mindlessly follow equities, fell about -1.6%. Precious metals were the worst performers, which is especially odd when you consider their reputation as safe havens in banking crises.

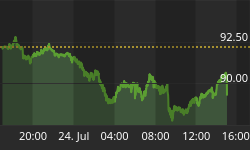

The odds of a full-fledged banking crisis rose, along with bond yields in Italy where the 10-year is again up to 6.5% (see Chart). Remember how, when the global central banks cut swap lines on November 30th, observers noted that the direct impact of the rate cut would be small since the swap lines were only lightly utilized? Well, last week the ECB took some $50.7bln on those swap lines, up from $400mm right before the swap line rates were cut.

Italian yields heading back up?

The rate is still less important than the availability of the line, and so the signaling significance is still the dominant reason to care about the concerted central bank easing - but it now appears that some of those rumors of banks having trouble accessing funding may not have been entirely spurious after all.

Long TIPS rallied despite the decline in commodities and the decline in yields, thanks to the Fed's buying of $1.378bln TIPS. Inflation swaps increased, but remain comparatively sanguine about the central bank's ability to peg inflation just about exactly where it wants it. The chart below shows the inflation swap curve at Monday's close (Source: Enduring Investments).

US Inflation Swaps

I suppose that this is consistent with the current level of yields and the generous equity market valuations (a Cyclically-Adjusted P/E at today's close around 20.3). The inflation market is pricing near-omnipotence from global central bankers. I guess if you believe that, then why shouldn't equities be valued with a thin margin for error? What is potentially most remarkable is that looking at the central banks' actual record of achievement over the last couple of decades, they still have such credibility.

Speaking of central banks, tomorrow the Fed meets. Market participants expect no major change in policy, although some observers think the Committee could indicate its new communications strategy. The stronger recent economic data could deter them from making any overt move towards QE3 until the end of January, but I would be cautious about this assumption. If the Fed wanted to move markets dramatically, a December action is much more valuable than a January action. Moreover, since the European summit fizzled it may be that the FOMC perceives a lot of risk over year-end and the next six weeks. And let's not forget that the Fed doesn't officially know who borrowed the $50bln that they swapped with the ECB, but they almost certainly know unofficially whether it is something to be worried about. In short, while a surprise Fed move on Tuesday isn't my base case, I don't think it's the long shot that many observers think it is. How do you play it? I'd consider selling the dollar into the announcement.

Also on Tuesday, we'll get November Retail Sales (Consensus: +0.6%/+0.4% ex-auto vs +0.5%/+0.7% last). Ex-auto Retail Sales have been remarkably stable for about a year now, with a little bump in the spring and a little dip in the summer. The consensus estimate actually looks slightly conservative given recent trends.