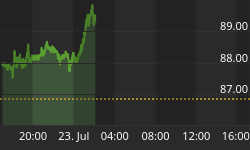

Having fought a stalwart battle above $1,700 and having seen over $1,900 this year, gold has not done as so many analysts have believed it would and risen through $2,000. Instead, here we're headed down towards $1,500 to who knows where? The stress in the financial markets has not stimulated safe-haven gold buying but has instead weakened the euro and indirectly helped drag gold lower. Prices have fallen to a point where investors with longstanding positions are liquidating some of their holdings to secure profits and momentum-driven traders are selling heavily. At the same time stresses continue to be seen in the European interbank lending market as USD funding has become even more expensive as the year closes.

The European Central Bank's USD tenders have done little to alleviate stresses in the USD funding market as was expected. Accordingly, European banks will continue the practice of acquiring USD funding through the foreign exchange forward markets, a process that is contributing to its strength. The aim of last week's European Union summit - that Eurozone governments agree to strict a fiscal pact in return for the E.C.B. buying government bonds -- has not materialized.

Yes, the E.C.B. did agree to lend money on easier conditions to European banks, but this is not as free a condition as was thought, as the load remains on politician's shoulders not on the E.C.B.; however, the ability of bankers to take low interest money from the E.C.B. and invest in higher yielding Eurozone government bonds is as we have said before, a form of "back door" Quantitative Easing. In time, this will be very bullish for gold as it was when the U.S. followed the Q.E. road.

Gold's Fundamentals?

Gold has so many incontestable positive fundamentals:

- Limited mine supply growth.

- Central bank demand.

- Only tiny sales from gold Exchange Traded Funds, confirming long-term holders are not selling.

- Jewelry demand recovery.

- A drop in scrap sales.

- Developed world political ineptitude on matters of finance.

Negative factors:

- A pause in emerging market demand [primarily because a weak Rupee has lifted gold price in India to record highs [They are now back to 'buyable' levels].

- Year-end book squaring and sales to secure profits.

- Reducing positions to lower margin costs as the price falls.

- Protective stop triggering of sales as well as sales triggered by the breakdown of support levels.

Please note the difference - On the bullish side these are solid long-term reasons why the gold price should rise. On the bear side, the reasons are short-term and, we feel, engineered reasons to sell gold.

Why is the price falling after London is closed and before Asia opens?

Is this forcing the price down?

One of the most suspicious facets of this last fall in the gold price is matched by the previous heavy fall from $1,900. If an investor wishes to sell his position, he will do whatever is necessary to achieve the highest price he can for his holdings. In the gold market, this is best achieved by selling in the market when he can sell the most gold at a price that is achieved on his entire sale at one time.

Best and Worst Ways to Sell Large Amounts of Gold

This is why the two daily Fixing sessions were set up in London. The AM Fix usually achieves the highest price, incorporating as it does the emerging - particularly the Indian and Chinese markets -- world. In the afternoon the Fix is usually set lower because the gold price usually falls in the U.S. After the afternoon Fix the gold price is usually at its daily weakest in a relatively 'thin' market. So sales after the afternoon Fix are almost guaranteed to achieve the lowest price and have the most detrimental impact on the gold price. And this is particularly so if the sales are heavy in a 'thin market. Certainly, unless immediate demand responds to this in Asia's day or in London's morning to the extent that they chase prices, the gold price will remain at the lower levels.

But the sales of gold - both on the fall from $1,900 and from $1,700 -- took place after both Fixes were done. Why on earth would a seller want to sell when he would achieve only the worst price? Why sell persistently to make the gold price fall further? That is unless that is precisely what he wanted to achieve? With lease rates in negative territory it appears that heavy lending has taken place encouraging just such falls. Is the motive the same as it was when central banks sold gold in the last fifteen years of the last century? It could be so! Their motive then was to ensure the dollar's dominance.

Can Central Banks Increase Their Leasings?

The Central Bank Gold Agreements since the turn of the century have been invisibly in support of the establishment of the euro. Now such establishment needs repeating for sure. But outright sales from European banks are unlikely.

In the first two Central Bank Gold Agreements clause four stated:

The signatories to this agreement have agreed not to expand their gold leasing's and their use of gold futures and options over this period.

However, the Third Agreement saw a change from this. It made no similar commitment! Although central bank activity in these fields has been very limited in recent years we have to ask, "Are we seeing it now?"

Bank Buying and Selling

Central banks are not price-chasers. More than that, they are almost unconcerned at the price, but are sharply focused on the volume offered to them. When they buy, they're aware that it's held by them for a time when their own currency may be unacceptable internationally. Therefore, they want quantity.

We're told that the dollar funding problems remain heavy, forcing banks to do what they can to raise loans, even if it means selling gold. Previously, we too, were of the opinion that commercial banks were the likely sellers of gold to raise loans and to facilitate lower interest rates. But there are certain features of the fall in the gold price that discredits this theory now. Commercial banks don't as a rule hold large amounts of gold on their balance sheets, so where could they get gold from to sell?

A glance back to last century shows a time when it was extremely profitable to borrow gold from central banks, sell if forward to achieve a market price plus the interest over the period that they could sell forward for. The interest is known as the 'Contango', which added to the price achieved, fetched far more than the gold price alone. But today the people who 'hedged' back then, were gold miners financing future production. Today, few gold miners would do that again. Why not? Because they do not have easily constructed gold project to finance. Secondly, when the gold price turned back to the upside, these hedged positions had to be unwound at a loss.

But it is the commercial banks that are doing so this time you may reason. Well, they don't have any gold with which to re-supply the bullion banks. They would have to go back to the market to re-buy the gold again, and if the gold price had turned they might be badly burned with such a gamble. Unless! If they knew they could engineer a big fall in the gold price, it would be worth a short-term gamble to be covered quickly so as not to be burned. Essentially this would be shorting the market. With lease rates in negative territory now it seems central banks are willing to make such loans and they too would need to be happy that the counterparty was able to return the gold safely back to them. Otherwise how could they face a public with a tale they had lent gold and the borrower was not able to repay or had gone bust? Such an event would prove scandalous to a central banker and badly damage confidence in the bank!

We, mere mortals will never be made party to such information any way. The conclusion that appears most reasonable is that such august institutions would ensure that the gold was returnable and in the absence of a gold miner supplying them from future production, would have to insist that the exercise was very short-term!

ETF Sales of Gold

Since the beginning of December the SPDR, States based gold Exchange Traded Fund has sold only 2.5 tonnes of gold. This amount is insufficient to force the gold price down over a hundred and more dollars in a few days. So we cannot accept this as a source of gold sales. Some say they were the lenders. The same restraints would apply to them as apply to the commercial banks. We feel that this would rule them out too. The same would apply to investors in those funds.

Gold Price Euro Linked?

Some analysts have now said that there is a link between the euro and the gold price. We struggle to find the smallest common denominator for that story. Oh, some may say that the gold price rose because of fears for the existence of the euro. Such speculation was not present when gold was at $1,900! As for fears about the euro now dissipating - nothing could be further from the truth. Fears remain heightened and the fear of a major bank crisis has grown even more as they remain so stressed.

Member's Only

Where is the Gold Price Headed?

Get the rest of the report. Subscribe @

www.GoldForecaster.com / www.SilverForecaster.com