Summary of Index Daily Closings for Week Ending December 22, 2004

| Date | DJIA | Transports | S&P | NASDAQ | Jun 30 Yr Treas Bonds |

| Dec 20 | 10661.60 | 3730.88 | 1194.66 | 2127.85 | 112^15 |

| Dec 21 | 10759.43 | 3792.09 | 1205.43 | 2150.91 | 112^28 |

| Dec 22 | 10815.89 | 3790.62 | 1209.57 | 2157.03 | 112^15 |

| SHORT TERM FORECAST (Next Two Weeks) | ||||

| TREND | PROBABILITY | Legend | ||

| Substantial Rise | Low | |||

| Market Rise | Medium | Very High | 80% | |

| Sideways | Medium | High | 60% | |

| Market Decline | Medium | Medium | 40% | |

| Substantial Decline | Medium | Low | 20% | |

| Very Low Under | 20% | |||

| INTERMEDIATE TERM FORECAST (Next 12 Weeks) | ||||

| TREND | PROBABILITY | Substantial | 800 points+ (DJIA) | |

| Substantial Rise | Low | Market Move | 200 to 800 points (DJIA) | |

| Market Rise | Medium | Sideways | Up or Down 200 (DJIA) | |

| Sideways | Medium | |||

| Market Decline | High | |||

| Substantial Decline | High | |||

Holiday Schedule: This week's Midweek and Weekend issues are being combined herein. The next issue after this will be as of Wednesday, January 5th, 2005. We wish all our subscribers and readers a very Merry Christmas, Happy Hanukkah, and prosperous New Year!

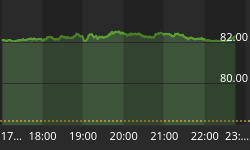

This is a very slow developing top, with seasonals pushing indices higher in spite of technical conditions that would normally produce at least a short-term correction by now. So your choices are to chase the last 5 to 10 percent out of an Election/Santa Claus rally, or take to the sidelines as the tide turns. So far this week, the Dow Jones Industrial Average closed up165.97 points, in spite of the risks noted from last week's Short-term TII reading of negative (37.00). Hedgies have found a trend they like.

Trannies finally hit an all-time high this week. The Dow Industrials did not. Major Nonconfirmation - the sort you'd expect at a Big-time top.

Coming Soon, in 2005, "Trader's Corner," a special feature for traders.

| Equities Markets Technical Indicator Index (TII) ™ | ||||

| Week Ended | Short Term Index | Intermediate Term Index | ||

| Sep 3, 2004 | (39.25) | (40.06) | Scale | |

| Sep 10, 2004 | (49.25) | (45.78) | ||

| Sep 17, 2004 | (69.00) | (44.73) | (100) to +100 | |

| Sep 24, 2004 | (52.25) | (42.02) | ||

| Oct 1, 2004 | 25.50 | (37.23) | (Negative) Bearish | |

| Oct 8, 2004 | (58.50) | (35.56) | Positive Bullish | |

| Oct 15, 2004 | (24.50) | (35.48) | ||

| Oct 22, 2004 | (15.00) | (36.93) | ||

| Oct 29, 2004 | 39.50 | (40.06) | ||

| Nov 5, 2004 | 5.50 | (35.28) | ||

| Nov 12, 2004 | (6.50) | (27.63) | ||

| Nov 19, 2004 | (50.00) | (23.18) | ||

| Nov 26, 2004 | (54.25) | (26.88) | ||

| Dec 3, 2004 | (56.25) | (30.50) | ||

| Dec 10, 2004 | (88.25) | (42.42) | ||

| Dec 17, 2004 | (37.00) | (44.25) | ||

| Dec 22, 2004 | 26.25 | (46.17) | ||

This week the Short-term Technical Indicator Index comes in at positive 26.25, indicating a sideways to up move is probable. This indicator is a useful predictor of equity market moves over the next two weeks, both as to direction and to a lesser extent strength of move. For example, readings near zero indicate narrow sideways moves are probable. Readings closer to +/-100 indicate with a higher degree of confidence that an impulsive move up or down is likely over the short run. Market conditions can change on a dime, or the Plunge Protection Team can come in and temporarily stop market slides, so it may be unwise to trade off this weekly measured indicator.

The Intermediate-term Technical Indicator Index is useful for monitoring what's over the horizon - over the next twelve weeks. It serves as an early warning system for unforeseen trend changes of considerable magnitude. This week the Intermediate-term TII comes in at negative (46.17).

An Analog that we have not shown before appears on the next page, this one comparing the calendar year 1972 with 2004 - closing, tick for tick - and depicting what happened after this uncanny similitude in 1973. During the first 85 percent of 1972 and 2004, the Dow Industrials followed similar sideways choppy paths until the reelection of a Republican president caused nearly identical Election rallies that picked up further steam from a Santa Claus rally - like a tropical storm that gathers strength from the ocean. The rallies from November into December were both sharp. Then on January 11th, 1973, what looked like the start of a glorious Bull run suddenly, unexpectedly reversed course and a yearlong 25 percent crash followed, stamped forever in the annals of history by the abrupt August resignation of Richard Millhouse "Tricky Dick" Nixon. We ask the question, could history repeat itself? Could 2005 bring an abrupt unexpected reversal of a glorious Bull run? Could the DJIA come crashing down in a year ending with the number "5"?

It is instructive to note that the post-election rally we are witnessing is almost the exact same price move as occurred the first time G.W. Bush was elected - both about 1,000 points starting around election day and running deep into December. Note that after 2000's euphoria petered out, the first of two stock market crashes to occur in 2001 began, in February 2001. A second, monster crash occurred a few months later. Again, we ask the question, could history repeat itself?

A third Analog which we have been tracking for some time now is shown above. This compares the great Bear market in Japan from 1985 through 1998 with the Dow Industrials from 1996 through 2004. This analog is remarkably correlated and is telling us that the same psyche that guided investors across an eight year Bear market span is occurring again in the U.S. markets. If this analog is to hold up, then the DJIA should soon come plummeting down from a 2004 double top pattern just as Japan's Tokyo Nikkei did from its same-stage double top.

For those whose hard earned money is pouring back into stocks - with or without your blessing - fueling this 2004 end-of-year rally, pause and take a hard look at these analogs. Your buying actions were predicted. Selling should be next.

The SPX/VIX ratio on the next page has hit an all-time record high as the VIX component has fallen to a nine year low. The pattern looks like what we saw from 1998 through 2000 as equities built a major top. The length of time this ratio has sat above 68 without a sharp equity decline warns us that something else is happening here than we've seen in four years - another huge top - a warning that a precipitous decline is on its way. We believe that decline will be the devastating Elliott Wave primary degree (3) down. This SPX/VIX chart may just be the Ghost of Christmas Future for equities.

The 10 day Average Call/Put Ratio is on a sell signal since this contrary sentiment indicator rose above 1.40, then crossed underneath and now sits at 1.32. Put Option buying has increased sharply the past 3 sessions, indicating the market could be close to topping, with selling nearby.

The Dow Industrials have retraced an almost exact Fibonacci .786 of the primary degree Elliott Wave (1) down from January 14, 2000's 11,749.97 intraday top to October 10th, 2002's 7,197.49 intraday low. This would make for a terrific top for primary degree corrective wave (2) - and as of Friday it looked like we were there. We had a nice five-wave upswing from October 25th's minor degree wave 4 bottom, and it looked like we had a nice textbook truncated fifth, intermediate degree C of an A-B-C top from October 2002.

However, the 168 point impulsive rally this week changed all that, turning the impulse rally from October 25th into a three-wave up-down-up. Since impulse waves must be five waves, not three, and there is nothing for the rally from October 25th to correct (thanks to the DJIA passing the February 11, 2004 10,746.88 intraday high for the rally from October 2002, we must expect the DJIA to rally further and complete a five-wave sequence. How high this goes before stopping also becomes a significant issue for the proper long-term and short-term Elliott Wave count. It must not exceed January 14th, 2000's all-time high of 11,749.97, or else the entire decline from January 14th, 2000 to October 10th, 2002 was only a corrective primary degree wave (4) inside a five wave grand cycle degree rally. It would mean the rally since October 2002 is really primary degree wave (5) of the grand cycle and that we are about to top at grand cycle degree {V}. How awful would this be? It would mean that after the top, then the real Bear market would finally begin. It would mean that the decline from January 2000 to October 2002 was child's play. All-time high Bullish contrary sentiment indicators such as the extraordinary high in the SPX/VIX ratio (it has blown away the 2000 high by a mile) could be warning of this. Above is a chart (courtesy of www.stockcharts.com) of this revised long-term EW count possibility.

We do not believe this will happen. We are of the belief that the top to this impulse from October 25th, 2004 will complete under 11,749.97 because of the rules required under the count on the preceding page of the DJIA. Under Elliott's rules, the third wave of an impulse cannot be the shortest. Minor degree wave 1 of intermediate degree C exceeds minor degree wave 3. Therefore, minor degree wave 5 must complete with a point rise less than minor degree 3's, less than 1,750 points. 1,750 from October 25th's 9,708 low would take us to around 11,458 as a maximum allowable top. This means minuette degree wave i of minor degree 5 has extended. That means iii must exceed v, which leaves very little room for the DJIA to rise for the rest of this Election/Santa impulse sequence.

Any way this plays out, it looks like the Dow Industrials are likely to rise a bit more, but in any case they are wrapping up an extraordinary top with huge Bearish implications.

We see Bearish directional divergences between an overbought RSI and price, and an overbought MACD and price. That implies any final thrust from this Santa Claus rally is limited - maybe another 6 percent tops. Friday's volume was humongous on a down day, showing just how fragile this market is. Any real fear is going to set off a steep, high-momentum decline. Simply put, the DJIA is a china doll.

The chart above shows Secondary divergences between the Dow Industrials and the Dow Transportation Average since 1999. In each instance, both indices experienced stock market crashes shortly thereafter.

This week a Primary divergence occurred whereby the Dow Transportation Average closed at an all-time high of 3,792.09 whereas the Dow Industrials did not (bright blue arrows). In fact, the Dow Industrials remain a whopping 907 points from setting an all-time closing high, eight percent below that mark. It is fascinating that such a significant divergence under Dow Theory is occurring at this time, when so many Analogs are calling for a crash, when record contrary sentiment indicators are calling for a crash, when insiders are dumping like there is no tomorrow, when the Elliott Wave count is calling for a major reversal down.

The Dow Transportation Average has risen 830 points, 28 percent, since August 2004 without a correction - which meets the criteria for a Parabolic Spike. The PE for this index is over 90x. What we have here is a manic bubble. Parabolic Spikes do not have soft landings. Once the air comes out of this balloon, this index is going to crash and burn. It's been a nice ride for the trend-seeking hedge funds, but both the Elliott Wave count and the Rising Bearish Wedge pattern also indicate the party is about over. Every Parabolic Spike since 1996 has been resolved with a Crash. We are not quite ready to declare the Parabolic Spike blow-off rally over, with two more subwaves likely, but the air is getting thin. The RSI and MACD have diverged against price, warning a top is near.

There is another major divergence going on, and that is the S&P 500's refusal to come even close to its all-time high of 1,553 back on March 24th, 2000. As it stands now, the S&P 500 is at 1,209.57, 22 percent under that pinnacle. Compared to other major indices, it is light years away. This is the sort of major divergence one would expect at a significant top. Contrast this with the NYSE and S&P Small Cap 600 Index which both hit all-time highs this week.

The S&P 500 is closing in on its minimum upside target for its Bullish Head & Shoulders pattern - 1,220, hitting 1,211 Wednesday. That also happens to be .786 of the all-time high of 1,553. It looks like a major top is in the books or very close. Another possible target for a top is 1,256, the .618 retrace of primary degree (1) down. That is more likely if the DJIA decides it wants to approach the 11,450 area. The Elliott Wave count looks complete, as prices wrap up a final minuette degree wave v that looks to be in the midst of micro degree 3 up of 5 up. We also see Broadening "Megaphone" and Rising Bearish Wedge top patterns in place, and Bearish divergences between the RSI's direction and prices, and the MACD's direction and prices. Down-day volume is up.

At this point, it is simply a seasonal momentum play. When the mania stops is anyone's guess, but when it does, it is going to be ugly. As an investor, one can chase the final 5 percent here, but one is buying stocks that insiders are dumping, at PEs over 20, during overbought conditions, when the Fed is tightening. Not my cup of tea.

The QQQQs - a proxy for the NASDAQ 100 - have formed a major topping pattern, Broadening Top "Megaphone" that is about a year old in formation. The RSI is declining from extreme overbought levels and has a Bearish divergence against the direction of price. The MACD is rolling over and is also Bearishly diverging in direction against price.

The Elliott Wave count which we believe to be most accurate at this time shows that the QQQQs are very close to completing primary degree wave (2), wrapping up a minuette degree wave v of minor degree 5 of intermediate degree wave C up. Since the final minor degree wave 5 up began in August of 2004, time and price bear reasonable proportionality to the other minor degree waves since early 2003, arguing for a major intermediate-term top in this index at this time.

The NASDAQ 100 Index is another major average that remains light years away from its alltime top, which was 4,816.35 on March 24th, 2000. Wednesday the $NDX closed at 1,613.57, a mere 3,202.78 points shy of the mark, still down 66 percent four and three-quarters years later. Again, when major averages diverge like we are seeing now, a Big League top is arriving.

The Economy:

According to a story by Parija Bhatnagar at www.cnnmoney.com on Monday, combined Retail Sales for this past weekend fell 3.3 percent versus the same two-day period a year ago - which wasn't so great back then. Sales for the week ended December 18th fell 5.9 percent from a year earlier. According to Redbook Research, Chain Store Sales fell for the third week in a row, and are down 0.7 percent in December versus November 2004. Deep discounts are generating sales, but risking profits. Wal- Mart and Target are hurting, and it may be they have lost their competitive edge as all stores now are buying their inventory from the same low-cost source - China. This statistic doesn't mean as much as it used to now that most manufacturing is occurring overseas. We borrow, we spend, they earn.

Leading Economic Indicators rose 0.2 percent in November - the first rise in six months - while October's figure was revised down to a decline of 0.4 percent. Equity price increases helped the November figure.

GDP was revised up to show a 4 percent annual growth rate the third quarter 2004, according to the Commerce Department. They also reported that Corporate Profits fell 4.2 percent in the third quarter.

Another FDA warning on a drug being widely sold, this time Aleve. Homeopathic remedies anyone? And lo and behold, the president's Council of Economic Advisors (CEA) cut its forecast for new jobs next year by 1.5 million. Gee, what a shock. We need to create 150,000 new jobs to keep up with population growth and they are projecting 175,000 per month. There ought to be a new statistic - family- supporting new jobs. That's where real problems are occurring.

Money Supply, the Dollar, & Gold:

M-3 figures come out Thursday afternoon.

The trade-weighted U.S. Dollar (shown on the next page) is in a minor degree wave 4 up correction. Minuette degree waves a and b appear to be over, with c left to complete. Proportionality suggests this wave c of 4 has perhaps another two weeks to finish before the final minor degree wave 5 takes the U.S. Dollar to a bottom for a while. That low would also be intermediate degree wave 5 down of primary degree wave (1) down - the culmination of a multi-year long-term decline. A major reversal should then unfold - an A-B-C corrective primary degree wave (2) up that could take the better part of 2005 to complete. That rally should retrace a Fibonacci percentage of the wave (1) decline. Following that would come a calamitous decline - primary degree wave (3) that should take the U.S. Dollar to new all-time lows and push Gold to all-time highs. That would also likely hurt Bonds and Equities.

The RSI has rebounded from deep oversold levels and the MACD has turned up, however both are flattening - typical wave four action.

We've seen a lot of volatility in Gold over the past two years and we now see two patterns that suggest quite a bit more volatility over the next six months. The short-term pattern is a Bearish Flag, an upside down Flag, where the choppy back and forth price action (the flag) angles away from the primary direction of the flagpole - which was down. These patterns are continuation patterns, and resolve in the same direction as the move that created the flagpole - so we can expect a breakout down. That decline should fulfill minor degree Elliott Wave 4 down, to be followed by a strong final thrust Elliott Wave 5 of 5 of (1) up. The Ascending Bullish Triangle suggests the thrust higher could hit 500 over the next six months. Note that the patterns allow for all targeted price action to take place inside Gold's long-term rising trend-channel.

The Gold Bugs Index ($HUI) charted on the next page has followed the path we expected from its mid-November top as outlined back in issue no. 97, November 5th, 2004, declining 40.41 points (16.2 percent) from its 248.18 high on November 17th to December 8th's micro degree wave 3 intraday low of 207.77. The HUI is in the last leg of an Elliott Wave minor degree consolidation - wave C that should take prices down below 180 over the next several months before turning back up in earnest. So far the HUI is finishing up a minuette degree wave i of v down. The RSI has predictably plummeted from a rare Head & Shoulders top formation to oversold levels, the place where minuette degree wave ii up can grab the baton for the next short-term path. The MACD also fell sharply from a Head & Shoulders top formation and momentum is now clearly down. Neither the RSI nor the MACD are anywhere near the levels seen at the last significant bottom, back in May 2004.

Silver has a Bearish Flag continuation pattern and should decline in the short-run.

I received quite a few e-mails last week asking how the Gold chart could have such as Bullish pattern as the Ascending Triangle with a projected upside target of 500, whereas Silver could have a reliable Bearish pattern such as the Bearish Flag at the same time? The point raised was that Gold and Silver are both precious metals and thus should move in sync. How can one go up while the other goes down?

Well, the above 14-year chart (courtesy of www.stockcharts.com) demonstrates that the price relationship between Gold and Silver does vary quite a bit. In 1998, Gold only sold at about 40 times Silver. In 2003, it sold at over 80 times Silver. This is because Silver and Gold have some key differences. Silver has industrial use whereas Gold largely does not. Gold has superior monetary importance to Silver. One of the gifts from the magi who worshiped the Child Jesus was gold, not silver. More to the point for Gold and Silver right now, it would appear that the Bearish Flag pattern in Silver is more short-term and Gold's Ascending Triangle is more intermediate term. Silver is correcting off of a Parabolic Spike whereas Gold is correcting off a steady stair-step rally trend. As this Bearish Flag has unfolded, the Gold/Silver ratio has climbed from 56 to 66 very quickly. Both, we believe, are in long-term rising trends. But as noted earlier, Gold has a small Bearish Flag pattern also, so the two metals may move in sync.

Bonds and Interest Rates:

The above chart shows the Long Bond since 1990. We see a stair-step path of rising prices (falling yields) until a peak in 2003. This stair-step rise in prices has formed a Rising Bearish Wedge pattern which supports the Bearish Head & Shoulders pattern that has formed since 2000. A decisive break below the neckline, below 102, would confirm the Head & Shoulders pattern and point toward a minimum downside target - an eventual move - of 81. Any decline like that would likely also be stair-step fashion, following the Elliott Wave impulse pattern of 1-down, 2-up, 3-down, 4-up, and 5- down.

It looks as though Bonds have traced intermediate degree waves 1 down and 2 up. However, the chart on the next page argues a Bullish intermediate-term scenario, so wave 2 may be tracing out something more complex with an upside target above 115. Whether Bonds rally or decline sharply from here, both scenarios are bad for equities. Rising Bonds portend deflation and likely recession. Declining Bonds mean rising interest rates - a slowdown in mortgage financing, the likely bust of the housing bubble, and higher borrowing costs - a slowdown in spending and corporate profits.

One scenario we may see is a rise in long-term prices (decline in yields) over the near-term as recession approaches. Then, Federal Reserve reactionary, massive liquidity infusions follow to help the economy, but drive bond prices lower, the dollar resuming its long-term decline after a corrective rise.

The above chart essentially tracks the Yield Curve over the past 14 years. It is a ratio comparing the 10 Year (long-term) yield with the 3 Month Treasury Yield. Whenever this ratio approaches the value 1.0, the yield curve is flat. We saw this from 1996 through 2000. Whenever it falls below 1.0, we have an inverted yield curve. We had this in late 2000 into early 2001. Whenever the ratio rises above 1.25-ish, we have an upward sloping yield curve. The long end's movements forecast the economy. As the long end's yield approaches the short end's, as this ratio falls toward 1.0, we can look forward to an economic slowdown. An inverted curve usually accompanies a recession or major slowdown. The Fed's policy of tightening - of raising short-term interest rates - usually does not initially cause a flattening yield curve. The flattening usually develops after a series of rising short-term interest rate bumps. The above chart shows that since the Fed started tightening last summer, the curve has been flattening. We just busted below the ratio 2.0. We should keep a watchful eye on this indicator because as this ratio gets down to 1.0, we can expect a recession to follow. By the time it inverts, we are probably already in one.

Note the speed of the descent since summer. The yield curve is making a beeline toward the flat area. Our take on this is that should it continue, long-term interest rates are telling us a recession is near, perhaps closer than anyone buying stocks during this post-election/Santa mania realizes. Why? Because during recessions, equities generally decline an average of 43 percent, according to John Mauldin's excellent research, as noted in his piece The Canary in the Coal Mine, December 18th, 2004 at www.safehaven.com. John is also the author of the must-read Bulls Eye Investing, John Wiley & Sons, Inc., 2004.

"Now it came about in those days that a decree went out

from Caesar Augustus, that a census be taken of all the inhabited earth.

This was the first census taken while Quirinius was governor

of Syria. And all were proceeding to register for the census,

everyone to his own city.

And Joseph also went up from Galilee, from the city of Nazareth,

to Judea, to the city of David, which is called Bethlehem,

because he was of the house and family of David,

in order to register, along with Mary, who was engaged

to him and was with child.

And it came about that while they were there,

the days were completed for her to give birth.

And she gave birth to her first-born son;

and she wrapped Him in cloths, and laid Him in a feeding trough,

because there was no room for them in the inn.

And in the same region there were some shepherds

staying out in the fields, and keeping watch over their flock by night.

And an angel of the Lord suddenly stood before them,

and the glory of the Lord shone around them,

and they were terribly frightened.

And the angel said to them, "Do not be afraid; for behold,

I bring you good news of a great joy which shall be for all the people;

For today in the city of David there has been born

for you a Savior, who is Christ the Lord.

And this will be a sign for you; you will find a baby

wrapped in cloths, and lying in a feeding trough.

And suddenly there appeared with the angel a multitude

of heavenly host praising God, and saying,

"Glory to God in the highest, and on earth peace

among men with whom He is pleased."

And they came in haste and found their way to Mary

and Joseph, and the baby as He lay in a feeding trough.

"And when eight days were completed before His circumcision,

His name was then called Jesus, the name given by the angel

before He was conceived in the womb."

"Now after Jesus was born in Bethlehem of Judea

in the days of Herod the king, behold, magi from the east

arrived in Jerusalem, saying,

"Where is He who has been born King of the Jews?

For we saw His star in the east, and have come to worship Him."

And when Herod the king heard it, he was troubled,

and all Jerusalem with him.

And gathering together all the chief priests and scribes of the people,

he began to inquire of them where the Christ was to be born.

And they said to him, "In Bethlehem of Judea,

for so it has been written by the prophet,

And you, Bethlehem, Land of Judah,

are by no means least among the leaders of Judah;

For out of you shall come forth a Ruler,

who will shepherd my people Israel."

Then Herod secretly called the magi, and ascertained

from the time the star appeared.

And he sent them to Bethlehem, and said, "Go and make careful

search for the Child; and when you have found Him,

report to me, that I too may come and worship Him."

And having heard the king, they went their way;

and lo, the star, which they had seen in the east, went on before

them, until it came and stood over where the Child was.

And when they saw the star, they rejoiced exceedingly

with great joy. And they came into the house and saw

the Child with Mary His mother; and they fell down and worshipped

Him; and opening their treasures they presented

to Him gifts of gold and frankincense and myrrh.

And having been warned by God in a dream not to return to Herod,

they departed for their own country by another way."

Luke 2: 1-14, 16, 21, Matthew 2: 1-12

| Key Economic Statistics | ||||||||

| Date | VIX | Dec. U.S. $ | Euro | CRB | Gold | Silver | Crude Oil | 1 Week Avg. M-3 |

| 6/18/04 | 14.95 | 89.41 | 121.17 | 267.75 | 395.7 | 5.98 | 39.00 | 9305.7 b |

| 6/25/04 | 15.19 | 89.22 | 121.41 | 270.75 | 403.2 | 6.12 | 37.55 | 9296.2 b |

| 7/02/04 | 15.15 | 88.18 | 123.09 | 265.50 | 398.7 | 6.01 | 38.39 | 9327.7 b |

| 7/09/04 | 15.78 | 87.41 | 124.10 | 269.00 | 407.0 | 6.46 | 39.96 | 9273.9 b |

| 7/16/04 | 14.43 | 87.12 | 124.36 | 271.50 | 406.8 | 6.72 | 41.25 | 9238.8 b |

| 7/23/04 | 16.50 | 89.23 | 120.88 | 269.50 | 390.5 | 6.33 | 41.71 | 9259.9 b |

| 7/30/04 | 15.27 | 90.12 | 120.10 | 267.00 | 391.7 | 6.56 | 43.80 | 9272.3 b |

| 8/06/04 | 19.34 | 88.45 | 122.69 | 268.25 | 399.8 | 6.77 | 43.95 | 9267.9 b |

| 8/13/04 | 17.98 | 87.97 | 123.68 | 269.19 | 401.2 | 6.62 | 46.58 | 9250.2 b |

| 8/20/04 | 16.00 | 88.22 | 123.03 | 279.50 | 415.5 | 6.87 | 46.72 | 9261.9 b |

| 8/27/04 | 14.74 | 89.80 | 120.20 | 275.00 | 405.4 | 6.58 | 43.18 | 9298.6 b |

| 9/03/04 | 14.28 | 89.56 | 120.66 | 275.25 | 402.5 | 6.59 | 43.99 | 9288.7 b |

| 9/10/04 | 13.75 | 88.60 | 122.61 | 272.50 | 403.8 | 6.16 | 42.81 | 9281.1 b |

| 9/17/04 | 14.03 | 88.10 | 121.76 | 275.75 | 407.6 | 6.28 | 45.59 | 9305.8 b |

| 9/24/04 | 14.28 | 88.59 | 122.57 | 278.50 | 409.7 | 6.42 | 48.08 | 9351.3 b |

| 10/01/04 | 12.75 | 87.77 | 124.07 | 284.75 | 421.2 | 6.94 | 50.12 | 9367.8 b |

| 10/08/04 | 15.08 | 87.55 | 124.13 | 287.60 | 424.5 | 7.29 | 53.31 | 9327.9 b |

| 10/15/04 | 15.04 | 87.20 | 124.73 | 286.45 | 420.1 | 7.11 | 54.93 | 9292.6 b |

| 10/22/04 | 15.28 | 85.97 | 126.46 | 287.00 | 425.6 | 7.33 | 55.17 | 9314.3 b |

| 10/29/04 | 16.27 | 84.98 | 128.85 | 284.75 | 429.4 | 7.30 | 51.76 | 9331.6 b |

| 11/05/04 | 13.84 | 83.89 | 129.46 | 283.00 | 434.3 | 7.50 | 49.61 | 9336.3 b |

| 11/12/04 | 13.33 | 83.71 | 129.85 | 283.50 | 438.8 | 7.62 | 47.32 | 9334.2 b |

| 11/19/04 | 13.50 | 83.32 | 130.13 | 287.25 | 447.0 | 7.60 | 48.44 | 9325.1 b |

| 11/26/04 | 12.78 | 81.81 | 132.93 | 288.75 | 449.5 | 7.59 | 49.44 | 9339.3 b |

| 12/03/04 | 12.96 | 80.98 | 134.53 | 284.75 | 456.0 | 7.99 | 42.54 | 9355.1 b |

| 12/10/04 | 12.66 | 82.59 | 132.36 | 276.25 | 435.4 | 6.74 | 40.71 | 9354.1 b |

| 12/17/04 | 11.95 | 82.20 | 132.90 | 285.25 | 442.9 | 6.80 | 46.28 | - |

| 12/22/04 | 11.45 | 82.01 | 134.06 | 282.50 | 441.4 | 6.93 | 44.24 | - |

Note: VIX at a new 9 year low, everything else flat.