Gold and silver mining stocks will be the dot-coms of the second half of this decade. Yet most of the people who bet on them will lose money because they ignore the first rule of speculative sectors, which is that no matter how well the sector does, most of its constituent companies will fail.

This rule applies wherever hot money is chasing untested concepts, but it's uniquely valid for mining, where reserves are uncertain until actually dug up, mines can cave in without warning, local laws can change in unfavorable ways, and managements frequently make dumb acquisitions. These risks make even the most attractive mine something of a crapshoot. Two recent examples:

Hecla's Hangover

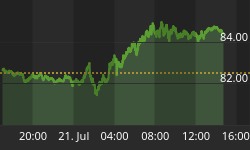

January 11, 201. Hecla already had a headache, but now it's suffering from a full-blown hangover.The series of unfortunate incidents that plagued Hecla Mining's (NYSE: HL ) mile-deep Lucky Friday mine during 2011 attracted the scrutiny of the Mine Safety and Health Administration, which has now ordered the mine's primary shaft closed until it can be cleared of debris that has accumulated over the years. Hecla estimates that the maintenance work will keep the mine shut through early 2013, leaving embattled silver investors to wonder whether someone spiked their holiday eggnog.

Hecla shares plummeted by more than 26% this morning, essentially mirroring a 26% reduction in the miner's 2012 production outlook from 9.5 million ounces to 7 million ounces. Despite a strong price environment that saw the average price of silver in 2011 surge by 74% over the prior-year average, Hecla's stock has lost some 54% of its value over the past 12 months. Though shareholders may wish to avert their eyes, the following image captures the devastation:

Kinross in Play After Paying Too Much for African Gold

Jan. 20 (Bloomberg) -- By paying too much for acquisitions in western Africa, Kinross Gold Corp. is now turning itself into the cheapest gold-mining target in the world.Kinross, Canada's third-largest gold producer, fell the most in almost two decades after saying this week it will write down the value of its Tasiast mine in Mauritania. The company sold for 76 cents per dollar of net assets yesterday, versus the industry median of 2.5 times, according to data compiled by Bloomberg. Writing off the excess $4.6 billion it spent on Tasiast would still leave Kinross at a 50 percent discount to its competitors, the data show.

Hecla and Kinross are big companies which have been around forever, and they still hit common speed bumps. They'll both survive, though, which is more than can be said for some junior miners with similar problems. Without money in the bank or other projects to share the load, an operating or cash flow problem can be fatal for a junior.

So why bother with mining stocks when you can just buy the metals? Because in the aggregate mining stocks will probably outperform the underlying metals (the fact that they haven't lately just means they'll outperform by an even bigger margin in the future), and the best miners will do two or three times as well as the metals.

So consider them, but show them some respect. Don't buy just one, no matter how much of sure thing your broker or brother-in-law says it is. Instead, buy five or eight or ten, even if it means owning just a few shares of each. Or buy a mutual fund or ETF and let them do the diversifying for you. GDX holds a basket of major gold miners, GDXJ a basket of junior gold miners, and SIL most of the silver miners. One transaction and you own the sector.

The sector, of course, contains winners and losers, so the real prize goes to whoever has more of the former than latter. As mining guru Rick Rule likes to say, most junior miners aren't viable, so all the gains in that sector come from the remaining 10 or 20 percent. So if you really want to be part of the coming mania you have to be a stock picker.

One low-stress way to do this is to piggy-back on the work of established analysts. They're not always right but they do spend their days trying to separate solid properties from holes in the ground guarded by liars. Their best ideas go first to subscribers and/or investors, but they can't keep everything to themselves. In media interviews, mining experts like Sprott's John Embry frequently name a few of their favorites, and the funds managed by people like Tocqueville's John Hathaway are required to report what they're buying and selling. Once that information is public, it's fair game.

Last but not least, keep some free cash available for opportunities like Kinross and Hecla, which are now takeover candidates.