Gold & Silver Investments Weekly Newsletter (Week Ending 23-01-05)

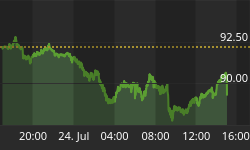

Gold was up 1.01% for the week, going from $423 to $426.90. Following last weeks 0.86% increase in price.

Silver (March contract) was up 3.3% for the week, surging 3.9% on Friday alone. The March contract rose 25.4 cents to close at $6.81 an ounce,

continuing from last weeks 2.65% increase.

Platinum was up 1.6% for the week.

Commodities, represented by the Reuters CRB Index (basic components include hard tangible assets such as Metals, Textiles and Fibers, Livestock and Products, Fats and Oils, Raw Industrials, Foodstuffs) was up 0.5 percent at 284.17 points. For the week: Palladium was up 4.3% for the week; Copper was up 2.5% to $1.4345 and very close to it's multi year, all time high.

Oil (NYMEX March crude) settled at $48.53 to close largely unchanged for the week following from last weeks 6.73% surge. Crude futures are well below the October peak above $55 a barrel, but prices are about 40 per cent higher than a year ago due to strong global demand, temporary output snags and fears that geopolitical strife could further threaten supplies.

Oil is up some 400% in the last six years. A surge in the cost of gasoline and other energy products pushed U.S. consumer prices up by 3.3 per cent in 2004, the biggest jump in four years.Price pressures last year were dominated by a 16.6 per cent surge in fuel bills, the biggest jump in 14 years, as gasoline prices jumped by 26.1 per cent, natural gas was up 16.4 per cent and home heating oil rose by 39.5 per cent. Those hefty price increases, reflecting turmoil in global oil markets, caused a major slowdown in economic activity in the late spring as consumers, struggling to pay higher energy bills, suddenly stopped spending on other items.

The Reuters CRB index has been trading since 1956. It tracks 17 component commodities ranging from key economic indicators like gold and oil to other important commodities such as cocoa, coffee and orange juice. The CRB can be divided into six categories of components which include energy, grains, industrials, livestock, precious metals, and what are termed soft commodities.

The Reuters CRB index has been trading since 1956. It tracks 17 component commodities ranging from key economic indicators like gold and oil to other important commodities such as cocoa, coffee and orange juice. The CRB can be divided into six categories of components which include energy, grains, industrials, livestock, precious metals, and what are termed soft commodities.

One of the CRB index's greatest strengths is the fact that there is an equal weighting of all of its 17 components. This weighting assures that no price increase in any single commodity, like oil, can significantly skew the entire index. Significant moves in the CRB are only possible when the majority of its component commodities are moving in unison with a particular primary trend. The most important commodities - gold, oil, and silver only account for 3/17th of the entire index. Commodities have been moving higher since its massive double bottom in early 1999 and late 2001. It has marched from a low near 183 in October 2001 to a recent bull market high of 290. This sterling 63% gain over three and a half years means that the CRB is likely in a secular bull market or a major new long-term trend likely to run higher for a decade or so. It is worth noting that if the Reuters CRB Index all time high of 338 in 1980 is adjusted to real dollar terms or adjusted fro the considerable inflation of the last thirty years it gives a price of 754 in November 1980 or 962 in early 1974.

"The dollar's failure to extend its gains recently, despite a flurry of news and economic numbers in its favour, eroded the market's support for the currency," said Brien Lundin, editor of Gold Newsletter. "In traders' views, if the greenback can't rise, then it's destined to fall," meaning that "if you're going to bet on a fall in the dollar, you also want to bet on a rise in gold," he said. The metal has also found support from the "ongoing, extremely strong level of physical demand from Asia and the Middle East," he said. This physical demand shows "no sign of abating and, contrary to historical experience, appears to be investment-related," Lundin noted. Overall, "the buyers have shown little price resistance, and their appetites for gold seem to increase along with the price," he said. This soaring physical demand from the Middle East, Asia including India and China and other regions is probably the most important factor determining the gold price. More so than even the movements of the dollar. This is summed up very well by UBS as reported in the John Brimelow report in Bill Murphy's Midas Commentary in Le MetroPole Cafe:"UBS notes that physical demand for gold remains very strong, particularly from India and other Asia although European demand is steady. Kilo bar premiums have increased sharply and there is good demand for metal in Switzerland, indicating that the Swiss refineries are working hard. The strength of physical demand is underpinning the gold price ..."

Gold's outlook remains positive for the longer term, with the "return of a weaker dollar the likely catalyst," said James Moore, an analyst at TheBullionDesk.com. Investors will continue to watch action in oil prices and the "broader geopolitical picture" as well, he said. In Friday dealings, the dollar turned lower, losing ground against the major global currencies.

Gold, silver, oil and the commodity complex in general seem to be continuing their consolidation at these levels before attempting to take out their recent highs. However, their may be further short term weakness before their long term trends reassert themselves. It looks the low inflation, high growth of the 1990's may soon be replaced by a period more akin to the low growth, high inflation 1970's or stagflation. This period witnessed gold's bull market when it went from $35 an ounce in 1971 and nine years later briefly hit 890% for a 30 fold or a 3000% increase in 9 years.

The US$, Currency, Stock and Bond Markets

The euro climbed 0.6% to $1.3042 late in New York, its first advance against the dollar in seven trading days. It climbed as high as $1.3067 at one stage. Despite the US$'s rally during the week it still only ended up 0.47% higher than the euro for the week.

The Dow Jones industrial average slid 78.48 points, or 0.75 percent, and closed below the important psychological level of 10,400 at 10,392.99. The Standard & Poor's 500 Index slipped 7.54 points, or 0.64 percent, to finish at 1,167.87. The Nasdaq Composite Index dropped 11.61 points, or 0.57 percent, to close at 2,034.27. For the week, the Dow ended down 1.6 percent, the S&P 500 was off 1.4 percent and the Nasdaq fell 2.6 percent. The Nasdaq closed at its lowest in 11 weeks, while the Dow and the S&P 500 closed at their lowest in 10 weeks.

U.S. stocks fell on Friday on a softer-than-expected consumer confidence report with the University of Michigan's consumer confidence index slipping to 95.8 from 97.1 in December and the oil price rising over a $1 a barrel. Stock indexes carved out fresh lows for the year. It was the first time since 1982 -- the year that the 1980s bull market started -- that the Dow and the Nasdaq fell for the first three weeks of a year. "It's more of the same -- economic concerns, worries about higher rates and earnings being in line at best," said David Memmott, head of listed block trading at Morgan Stanley. "Oil is still a concern, it's inching back up to $50, while new money coming to the marketplace is very light." The stock indices ended at their lowest levels of the week and lowest levels of the year so far and the technicals have become quite bearish. A weak January could set the tone for the months ahead, said Robert Drust, managing director of listed trading at regional investment bank Wedbush Morgan. "It seems to me that it sets the tone for how people will position themselves for the coming months," he said.

U.S. Treasury debt prices rose slightly, bolstered by a surprising drop in consumer sentiment. The benchmark 10-year U.S. Treasury note rose 7/32 to 100-26/32, yielding 4.17 percent, essentially unchanged on the day. The two-year note inched up 2/32 to 99-23/32 for a yield of 3.16 percent, down from Thursday's 3.20 percent.The sanguineness of the bond market and the bond market vigilantes failure to sell bonds due to the burgeoning inflationary pressures has some seasoned market observers puzzled. But most are in agreement that as Bill Gross of PIMCO has put the 'salad days' are over for the bond market and the we are at the bottom of the interest rate curve.

Essential Quotes from the Week

"If January can't mount a gain, any further advance we expected for 2005 is probably dead in the water."

Jeffrey Hirsch, Editor of the Stock Trader's Almanac

"2005 will probably mark the start of a more difficult period for the UK economy. The biggest hit of all is set to come from the housing market which has already embarked on a major slowdown. Whereas the main driver of the economy in recent years has been robust household spending growth, this is likely to suffer as the housing market slowdown gathers pace. Although 2005 may not be the year when things go completely wrong, it will probably mark the start of a more difficult period for the UK economy."

Roger Bootle, Chief Economic Advisor, Deloitte

"Long-term saving just doesn't seem to be registering as a priority in the British psyche, but it's never been more critical. If faced with a financial crisis, most people would turn to a 'white knight' to help them, rather than take responsibility themselves. More than a fifth (22%) would turn to their family for help, 21% would go cap in hand to the bank. Only 19% think they would have adequate personal savings to copeThere will soon be too many pensioners for the state to support in any meaningful sense, so people need to take control of their financial future as soon as they can."

David Elms, Chief Executive, Independent Financial Advice

"Once in a while a trend takes hold that's so powerful, it transforms the entire global economy: the Industrial Revolution of the 18th century, the Modern Industrial Nation in the 19th century, and the emergence of cheap computing and communications in the 20th century. The latest megatrend? It's the rise of the BRICs. That's shorthand for the four dynamic developing nations with large populations - Brazil, Russia, India and China...collectively they could be larger than the G6 [the world's six leading economies] in just four decades." (Editor's Note - There are obvious implications for global demand for commodites and precious metals.)

Four Countries You Must Own, Business Week

"Since the late 1990's, I've become increasingly concerned about the exceptional rise in consumer, corporate, and government debt relative to this country's ability to service this debt through lagging income and revenue growth. The various ratios of debt to income in the past have been reliable indicators in determining where our economy was at within the business cycle. Today, we as a nation and as investors are at risk as never before. I am not alone in this pessimistic assessment of our economy, some of the best known and wealthiest investors on the planet are saying the same thing in their own way. It's a time for doing homework and strategic planning." <"I told you once before that there were two times for making big money, one in the upbuilding of a country, the other in its destruction. Slow money on the upbuilding, fast money in the crack up. Remember my words. Perhaps they may be of use to you someday." - Rhett Butler to Scarlet O'Hara, Gone With the Wind.>

Hal Swanson, Commodities, Futures & Options Service.

"It is generally assumed that increases in credit stimulate aggregate demand. In the short run that is always true. But in the long run it need not be true. The expansion of credit is an increase in debt. When debt levels are low, a credit expansion which increases debt does not leave a legacy which later suffocates demand, since the resulting still low level of debt is not yet a problem. But when debt levels are very high, the increases in debt created by credit expansion soon act as a burden on demand. It follows from the above that, as the level of debt relative to income rises, it should take larger expansions of credit to achieve any given percentage increase in demand, since the now high, and climbing, debt burden acts as a countervailing force to depress demand."

Auerback, Prudent Bear

"Fifty years ago most people, remembering 1929, were afraid of the stock market. As a result, those who did buy stocks got to buy them cheap: on average, the value of a company's stock was only about 13 times that company's profits. Because stocks were cheap, they yielded high returns in dividends and capital gains. But high returns always get competed away, once people know about them: stocks are no longer cheap. Today, the value of a typical company's stock is more than 20 times its profits. The more you pay for an asset, the lower the rate of return you can expect to earn. That's why even Jeremy Siegel, whose "Stocks for the Long Run" is often cited by those who favor stocks over bonds, has conceded that "returns on stocks over bonds won't be as large as in the past." But a very high return on stocks over bonds is essential in privatization schemes; otherwise private accounts created with borrowed money won't earn enough to compensate for their risks. And if we take into account realistic estimates of the fees that mutual funds will charge - remember, in Britain those fees reduce workers' nest eggs by 20 to 30 percent - privatization turns into a lose-lose proposition. "Sometimes I do find myself puzzled: why don't privatizers understand that their schemes rest on the peculiar belief that there is a giant free lunch there for the taking? But then I remember what Upton Sinclair wrote: "It is difficult to get a man to understand something when his salary depends on his not understanding it."

Paul Krugman, New York Times

"All Uncle Sam's debt, including private household consumer credit-card, mortgage etc. debt of about $10 trillion, plus corporate and financial, with options, derivatives and the like, and state and local government debt comes to an unvisualisable, indeed unimaginable, $37 trillion, which is nearly four times Uncle Sam's GDP [gross domestic product]."

Andre Gunder Frank, Economist, University of Amsterdam

"I think, over time, unless we have a major change in trade policies, I don't see how the dollar avoids going down," Buffett, the world's second-richest manl told CNBC television. "I don't know when it happens. I don't have any idea whether it will be this month or this year or next year, but we are force-feeding dollars on to the rest of the world at the rate of close to a couple billion dollars a day, and that's going to weigh on the dollar. I'm having a hard time finding things to buy, if that says anything about the market," he said

Warren Buffet, Berkshire Hathaway

Rare coins are starting to attract investors more at home with stock brokers than coin dealers. The interest in coins comes as sophisticated investors are increasingly looking for assets outside of the U.S. stock market, which many market observers expect to post only modest gains during the coming year. In buying rare coins, individuals not only acquire a collectible asset, but they are also getting exposure to precious metals. The prices of gold and silver, from which many popular U.S. coins are made, are both rising smartly ... Of course, you don't have to be rich to invest in coins. In fact, the lower end of the market is booming, too.

Jeff D. Opdyke, 'Investors Flock to Coins Amid Rising Metal Prices', Wall Street Journal

Gold is undervalued, under-owned and under-appreciated. It is most assuredly not well understood by most investors. At the beginning of the 1970's, when gold was about to undertake its historic move from U.S. $35 per oz to over U.S. $800 per oz in the succeeding 10 years, the same observations would have been valid. The only difference this time is that the fundamentals for gold are actually better.

John Embry, Sprott Asset Management

Some of the sharpest minds on Wall Street are betting that you'll make more money in metals than Microsoft the next few years. The new bull market is in stuff, not stocks, they say. We're talking about land and oil and gold, the commodities that once made John Jacob Astor, John D. Rockefeller and the Hunt brothers very rich men.

John Waggoner, 'Real assets create real riches', USA Today

"But danger could lurk on the horizon. An economy that has been boosted by an unprecedented amount of fiscal and monetary stimulus could come back to reality with a thud."

Martin Wolk, Chief Economic Correspondent, MSNBC

Conclusion

The week was dominated by the beginning of President Bush's second four year term. In his inauguration speech, Bush called for freedom everywhere, "the urgent requirement of our nation's security and the calling of our time." He promised to expand freedom around the world saying his policy was to "seek and support the growth of democratic movements and institutions in every nation." Bush thus clearly signalled a continuation of what his supporters see as a genuinely noble, sincere and moral desire of spreading freedom around the world and defending the western world from the evil of terrorism. Realpolitik critics of the recent hawkish US foreign policy however are worried by these interventionist policies which they consider naively radical, utopian, messianic. These traditional allies of the US and supporters of US foreign and economic policies believe such policies will destabilise the Middle East and the world with the attendant higher oil prices and war taking it's toll on the global economy. They do not believe that freedom can be achieved out of the barrel of a gun and indeed believe that the over reliance on militarism rather than diplomacy and economic incentives (using the stick rather than the carrot) will be counterproductive in the long term in the cause of freedom both for the 'liberated' peoples of the world and for the civil liberties and freedoms of citizens in free democratic societies.

The geopolitical situation (whether one is "with" President Bush and the 'War on Terror', "against" him and the 'War on Terror') is accepted by nearly all commentators to be the most unstable since the falling of the Berlin Wall and the end of the Cold War. As is obvious from President Bush's inauguration speech and Vice President Cheney's remarks that "Iran was right at the top" of the administration's list of world trouble spots and that Washington was "concerned that Israel might strike Iran" in an attempt to halt its nuclear programme. This instability is likely to intensify and thus what financial analysts call the 'terror premium' or 'war premium' is likely to act as strong underlying support of oil and precious metal prices. In this environment, precious metals 'safe haven' status is likely to increase.

Added to this the increasing evidence of burgeoning inflation in the US economy, as evidenced by nearly all commodities being at near record highs and by the news this week that overall consumer prices rose 3.3 percent last year, up from 1.9 percent in 2003 with energy prices up 16% in one year. Some economists have even questioned the validity of these statistics positing the theory that government statisticians are low balling inflationary figures and accentuating the positive for their political masters. One way or another, the benign paradigm of low inflation and high growth looks like it will soon be replaced by a less benign low or stagnating growth and high inflation period. This will necessitate a further rise in interest rates thereby compounding the problem for the overly indebted US consumer.

David Chapman of Union Securities made a very astute observation about gold's strong performance over the long term or more than 34 years. "We are constantly amazed that just because gold and gold stocks have stalled out over the past year that suddenly we get all these experts saying things like we told you so, gold really is a barbarous relic and the gold bugs are just whacko's anyway. Let's try another set of numbers on for size. Since Gold was set freely trading when the world came off the gold standard (officially August 15, 1971), Gold has increased from $35 to today's $422 for an increase of 1106%. The Dow Jones Industrials has increased from 856 to 10,471 for an increase of 1123%. Not exactly what we would call an overwhelming lead for the stock market. Yet over $50 trillion of assets are in paper assets (stocks, bonds etc) and barely $2.5 trillion is in gold." So gold has performed as well as the Dow Jones over a 30 year plus period however it's detractors are always selective by choosing gold's peak and the end of it's last bull market in 1980 at $890 and then extrapulating that it has not been as good an investment as stocks over the long term. Beware of gold's detractors. In the immortal words of Benjamin Disraeli (attributed to him by the great Mark Twain): "There are three kinds of lies: lies, damned lies and statistics."

Gold and silver will perform strongly in an inflationary or stagflationary environment and are unique as an asset class as they will also protect you should an inflationary period morph into a deflationary period.

It is prudent to invest or save at least 5% of your or your family's wealth in precious metals. Precious metals are not about making massive returns although that is certainly very possible.

Rather it is about having in your possession finite, debt free hard tangible assets which have been money and stores of value for thousands of years and are the ultimate safe haven assets and financial insurance. At least a small portion's of one's wealth should thus be saved in or invested in gold and silver in order both for the good possibility of capital appreciation and gain but even more importantly in order to preserve one's or one's families capital or wealth.