Be careful here. The most dangerous market climates occur when the news and/or the economy is in transition. When things are great, everyone knows they're great; the market may get overvalued but there's not a catalyst for a drop. When times are awful, everyone knows they're awful; the market may get undervalued (although this has not happened in a while) but there's not a catalyst for a pop. It's when the economy is in the middle of a phase change that sharp movements can occur as we shift from euphoria to lamentation, and sometimes right back, overnight.

The key test on Thursday was the auction of 10-year Spanish bonds. Spain also sold 2-year maturities, which gave it some flexibility to sell more of those and less of the 10-year and still sell "more than the €2.5bln target." The bid:cover ratios were okay, but the 10-year got bombed after the auction, trading up 10bps in yield to 5.90%. Watch how this trades - it is very likely that some participants were arm-twisted into bidding, and those buyers will be dumping paper indiscreetly.

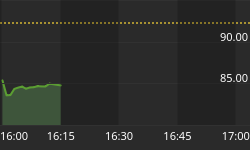

Meanwhile, in the background, Italian yields have been rising again as well. The 10-year bond is at 5.60% (see Chart, source Bloomberg). No one is worrying about Italy at the moment, because we're all too busy worrying about Spain. But the positive momentum has evaporated there, as you can see from the chart. Somewhat amazingly, investors are completely ignoring the silly talk about the trillion-dollar firebreak. Today Poland announced it would contribute $8bln to the IMF effort. With Japan and Poland leading the way to saving Europe, we have officially descended into farce.

In the U.S., the economic data was weaker-than-expected. It wasn't disastrous; the economy continues to grow, but isn't gaining strength in any measurable way. Initial Claims were 386k (with an upward revision) compared to 370k expected. Philly Fed went from 12.5 last month to 8.5 this month (vs. 12.0 expected). Philly Fed is a good current illustration: the index measures not the level of activity, but the rate of change, by asking how conditions are compared to the prior month. So low, positive numbers means that growth is limping, but limping forward a little bit every month.

Existing Home Sales have fallen back after a couple of good-weather months. On the plus side, the inventory of existing homes remains near a seven-year low, which should help support the pricing dynamic in the housing market (as will the general buoyancy of inflation generally). More on housing, below.

Five-year TIPS were auctioned, and as is normal for the 5-year it was somewhat sloppy going in and coming out. Finding natural demand for long-dated real bonds is easy. Finding natural demand for shorter-dated real bonds is always somewhat iffy. After the auction, TIPS backed up 3-4bps across the board. Unlike with Spanish bonds, however, other investors are actually willing to buy TIPS at these levels (because, while very expensive, they're still cheap relative to nominal bonds).

Tomorrow's calendar is light, and trading will probably be thin. But as I say: be careful here.

.

The housing market is obviously still suffering, and one reason that the inventory of existing homes appears so manageable is that there is a considerable 'shadow inventory' of homes that aren't on the market because the sellers are discouraged by market conditions. So it is even more surprising to me that we haven't seen a development that some observers have been long waiting for in the U.S.: the home price indexed mortgage (hereafter abbreviated HPIM).

A HPIM is a loan, secured by a home, whose principal value rises or falls with the value of home prices. The index chosen for home prices can be a national index (which would enhance the securitization of the mortgage) or a more local index (which would more-closely connect the mortgage's principal to the value of the particular home). The coupon is fixed, as with TIPS, but paid on a variable amount of principal. The principal amortizes over time as with a regular mortgage.

Various laws set up for the nominal world, and possibly taxation issues, have impaired the development of the HPIM in the U.S. But they exist in some other countries (e.g., Turkey), and theorists have spent some time examining the concept so this is not a "new" idea. But when the housing market was booming, and people saw their houses as leveraged speculative vehicles as well as places to live, borrowers also didn't want to take a loan that they saw as likely to grow rapidly in principal value. Now, however, the value is more obvious:

If you are a homebuyer, you may be willing to take your time buying a home right now, fearful that prices could fall further. But with an indexed mortgage, if the value of the home falls then so does your loan. Therefore, there's much less reason to defer a home purchase, which is one reason that HPIMs could help clear the housing market inventory. Also, while your total outlays will be similar if housing inflation actually turns out to be what is currently priced into the market when you take out your mortgage, the pattern of those outlays tends to help the homebuyer because the coupon payment would be lower than a nominal coupon, especially in the early years of the mortgage, as the inflation accrual adds to the principal.

At present, for example, 30-year mortgage yields are around 4%, so your interest payment on a $100,000 mortgage will be $333.33/month in the first month of the loan. However, the coupon on a HPIM would likely be around 1.5%, or $125/month, if long-term inflation is expected to be around 2.5%, and the principal would be expected to grow around 0.2% per month. And after one year (if no principal was paid, for simplicity) the coupon would be expected to rise to $128.12, which is 1.5% of the new principal ($100,000 * 1.025 = $102,500).

Again, in the boom years it would have been hard to persuade a homebuyer to give up his perceived upside, but notice that the "upside" depends on home prices rising faster than the nominal rate embedded in the loan. Still, a home financed with a fixed-rate loan does represent a serious inflation hedge in normal times. With an HPIM, however, the ability to participate in the upside doesn't vanish - it is just limited to the amount of equity a homeowner has. So if I own a $100,000 house and I have an $80,000 mortgage and prices double, I still 'participated' in the home price rally: my asset is now worth $200,000, my liability is now worth $160,000, and instead of $20k equity I now have $40k equity. That's not as good as if I had had a nominal loan, which is still worth $80,000 so that my equity is now $120k, but if I want more participation I can always buy more of my house back from the bank (that is, pay down the loan and build equity). In other words, with the HPIM structure a homebuyer cannot take a highly-levered speculative position in housing; however, you profit on the part of the house that your family, and not the bank, owns. This doesn't sound like a bad idea, does it?

Moreover, the idea that taking out a mortgage to buy a house is a sure-fire way to build wealth was mostly a period myth anyway. Over the long haul, residential real estate grows at a real rate of only about 0.5%, which means that without a good bit of inflation, a mortgagor paying a fixed rate of 5% or 6% or 7% is actually falling behind in real value (even with the tax deductibility of interest, although that helps). It is true that in a boom, you can make lots of money borrowing 99% of a purchase that rises 15% in value every year...whether that purchase is a home or an internet stock. The problem is that you can lose it all by being levered in a bust, and you don't do very well if prices simply stagnate.

As an investor, by the way, I'd love to be able to buy a bond backed by home-price-indexed mortgages. And the existence of such a market would allow the creation of bonds that paid inflation minus housing inflation; in other words, it would help the 'inflation basis' market germinate.

I don't see much hope that this sort of mortgage is coming soon, because while there are proponents and theorists around for the concept, it is an innovation that requires some changes in legal and tax infrastructure - and there are few evangelists out there for this sort of product. But despite that, I am still a bit surprised that we don't hear more talk about it - because it is a good idea.