In a December 2011 video, we explained how the ECB was using a "backdoor bazooka" approach allowing banks to use borrowed ECB funds to purchase newly issued Italian and Spanish debt. While acknowledging the ECB's approach could be a "short-term fix", we questioned how the unlimited loan program would address the core problem of too much debt. Four months later, the markets are beginning to realize serious problems remain in Euroland. From Thursday's Wall Street Journal:

Europe's bold program to defuse its financial crisis by injecting cash into the banking system is running out of steam. The European Central Bank's roughly €1 trillion ($1.31 trillion) of emergency loans caused interest rates of troubled euro-zone countries to plummet earlier this year, easing fears about Europe's debt crisis. But lately rates have again been marching higher.

One big reason: After months of using that cash to buy their government's debt, banks in Spain and Italy have little left, say analysts and other experts. The banks' voracious buying had helped bring down the interest rates, providing relief for troubled countries that need to issue tens of billions of euros of bonds this year. But the banks, lately the primary buyers of Spanish and Italian government bonds, no longer have much spare cash to continue such purchases.

On Friday morning, the yield on an Italian 10-year bond was approaching similar levels to summer 2011 (see arrows). The stock market did not perform well in August 2011.

We believe it is only a matter of time before the ECB and/or Fed are forced to engage in another round of massive money printing to prop up the global financial system. The big question for investors is will they take somewhat of a preemptive strike or will they wait for the next "flash crash" type event.

As we have outlined for clients, we believe the cycle of central bank-induced melt-ups and debt-induced melt-downs is not behind us. The video below, posted in Thursday's Short Takes, describes a new and "faster" market model we have designed for a melt-up/down world. For those pressed for time, a slide showing the video's contents and corresponding times appears at the 20 second mark, allowing you to skip to selected topics.

The model described in the video above, the CCM Market Risk Model, closed April 19 at 85, which means despite the market's recent weakness, 85% of the answers to the model's questions continue to come back in the bulls' favor. The model is designed to move quickly, but for now it remains far from "run for the exits" territory.

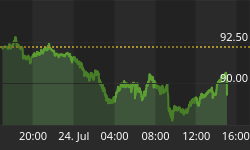

Near the close on April 19, the S&P 500 was trying to stabilize at a logical level when viewed on a sixty-minute chart (see below). As we noted earlier in the week, the 100 and 200-hour moving averages acted as resistance near the close on April 17 (see intersection of thin red and blue lines). The pink trend channel is still rising, which gives the nod to the bulls until it is violated on the downside.

The Relative Strength Index (RSI) violated similar trendlines in a bearish manner earlier this week, which can foreshadow a similar move by price. Until we see some conviction from buyers, it would not be surprising to see market weakness continue.

On weekly charts, we have numerous momentum indicators that look tired. They still have room to stabilize but not that much room. The bulls remain in control but the grip is not nearly as tight as it was two weeks ago.