Unfortunately I was sick the past few weeks and I am just now getting back into the swing of things. Similar to the demand pull that the warmer than usual spring has had on macroeconomic data, the warmer spring caused me to have an earlier than usual sinus infection as well as some horrific allergies.

I suppose I am pushing it a bit far when I am comparing my health concerns to economic data, but alas I fly my nerd flag proudly.

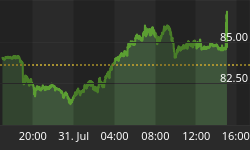

Recently I have been advising members of my service to be cautious as the market appears to be at a major crossroads. The U.S. Dollar Index is on the verge of a major breakdown. If a breakdown occurs it will be clear that the Federal Reserve will have officially stopped any potential rise in the U.S. Dollar. Over the past few months the Dollar has been producing a series of higher highs and higher lows, however the current cycle may break the pattern as can be seen below.

If the U.S. Dollar pushes down below the recent lows and we get continuation to the downside, we will break the recent bullish pattern. Furthermore, if the Dollar starts to weaken it should benefit equities and other risk assets such as oil. Higher energy prices would not be long term bullish for equity markets so there is concern if the Dollar really starts to extend lower.

However, if the Dollar finds a bottom and rallies it clearly would create a headwind for equities. We should know whether we have a major breakdown on the daily chart in the next few weeks. Until then, the Dollar could go either way and obviously the price action in the Dollar will have a major impact on risk assets and stock market returns in the near future.

From a macroeconomic viewpoint, risk assets such as the S&P 500 Index could be in trouble in the months ahead. U.S. gross domestic product (GDP) came in lower than expected with revisions likely in the near future. Unemployment claims appear to have bottomed and are rising week after week even though the major media fails to report it appropriately as it would appear that the Bureau of Labor Statistics has stumped media pundits with data revisions.

Additionally, there are two other macroeconomic data points which need to be mentioned. The Citigroup Economic Surprise Index has moved below zero and is showing a negative reading. This index is generally a leading indicator regarding equity prices and the recent decline shown below is problematic for the bullish case.

Chart Courtesy of Morgan Stanley

As can be seen above, fundamental data is starting to skew towards the downside which is likely a result of the recession that is in the process of developing over in Europe and potentially in China. Time will tell if the index can reverse, but the bulls need to see a major reversal in the near future.

The chart below illustrates the relationship between metal prices and industrial productivity. Demand for metal increases when economies are expanding and prices generally contract when economies retract. The chart below demonstrates global metal demand. The chart speaks for itself.

Chart Courtesy of Morgan Stanley

Clearly if industrial production contracts (reduction in Global Manufacturing PMI) the impact on the global economy will be felt across multiple countries' economies. The chart below illustrates the MSCI World Index compared to global manufacturing PMI. Similarly to the chart above, this chart also tells a significant story about what investors and traders should expect if the PMI numbers come in light against expectations.

Chart Courtesy of Morgan Stanley

As quoted from the zerohedge.com article entitled What do Metal Prices Tell us About the Future of the Stock Market, "In other words, for those who still believe in logical, causal relationships (even in a time of ubiquitous central planning) unless something drastically changes to push fundamental demand of metals higher, one could say the the outlook for equities is not good."

Essentially, the data shown above is certainly not bullish in the intermediate to longer term. However, it generally takes time for macroeconomic data to permeate all the way through to equity markets. For right now, the story regarding global growth is at the very least questionable based on the data illustrated above.

In the short term anything is seemingly possible. The S&P 500 Index closed above the key 1,400 price level on Friday. I would not be shocked to see prices extend up to the recent highs near 1,420. Ultimately I think we are in a long term topping formation that might require another higher high up to around 1,440 before we see a deeper correction.

The past few weeks have produced a very mild correction compared to the monster rally we have seen since October of 2011. This is a bullish signal, but we need to see prices continue higher and climb a serious "wall of worry" that is coming out of a variety of places. The European situation continues to worsen overall and we have lower than expected GDP numbers in the US paired with concerns about growth in China.

The S&P 500 has some negative headlines to deal with, but so far it has been able to shrug off poor economic data and we could see an extension higher that would shake out the shorts and run stops above the recent highs. However a move lower remains possible. The daily chart of the S&P 500 illustrates the recent correction and the 1,420 highs.

I believe that the next few weeks are going to be critical and the S&P 500 may trade in a consolidation zone between recent lows and the 1,420 highs while traders await more economic data. Fundamental data is starting to indicate that a slow down may be beginning. In contrast, the topping pattern that we appear to be carving out may require higher prices to suck in more longs before moving into a deeper correction.

In the short run, the Dollar will likely hold clues regarding the immediate future for risk assets. However, the longer term picture for equities is quite murky based on the economic data points we are seeing paired with additional concerns stemming from the European sovereign debt crisis. Right now I am looking at time decay based strategies in the near term and will likely stay away from directional biased trades. I would urge readers to be cautious regardless of which direction they favor.

Looking for a Simple ONE Trade Per Week Trading Strategy? If So Join www.OptionsTradingSignals.com today with our 14 Day Trial