"I guess I should warn you. If I turn out to be particularly clear, you've probably misunderstood what I've said," Fed chief "Easy "Al" Greenspan used to say. Recognizing the fact that financial markets place a heavy value on each of their words, former Fed chiefs Arthur Burns and Paul Volcker, were known for blowing smoke, both literally and figuratively, when appearing before Congress, in order to prevent their words from becoming self fulfilling prophesies. They developed a language called "Fed-speak," which is the use of ambiguous and cautious statements that are purposefully made to obscure the meaning of a statement. Greenspan is credited with turning Fed-speak into a "fine-art" form.

Having served for six presidents in four different jobs, Greenspan became one of the most entrenched and powerful figures in Washington. He was a shrewd political operator, a man who was handed his job by political allies in exchange for political loyalty. Greenspan used to hold his cards very tight. The secret meetings he held with presidents and the secret deals he offered them only added to his mystique. By custom, Greenspan could overrule the other Fed governors, which meant that he controlled a critical portion of the world's money supply, and he could use this leverage to influence public opinion ahead of an election.

On June 7th, Greenspan's protégé, - Fed chief Ben "Bubbles" Bernanke spoke to a congressional panel, and traders were listening carefully to his every word, trying to discern if the Fed would unleash QE-3 ahead of the upcoming elections set for Nov 6th. The Fed could pump-up the money supply, and buy more Treasury bonds and in turn, jolt the stock market sharply higher. In theory, a stock market rally could boost consumer confidence, and influence American public opinion into thinking that an economic recovery is on the horizon.

"As always, the Federal Reserve remains prepared to take action as needed to protect the US financial system and the economy in the event that financial stresses escalate," Bernanke told the Joint Economic Committee. That suggested the Fed would only unleash the nuclear option - "quantitative easing," (QE), if (1) Greece opted to leave the Euro, or (2) if European politicians failed to hook-up the zombie banks in Italy and Spain on artificial life support.

If neither of these "Black Swan" events were to occur, - then in the opinion of Global Money Trends, the Fed is expected to stay politically neutral ahead of the Nov 6th elections, and abstain from a third round of QE. Staying neutral could include a token gesture to extend the Fed's "Zero Interest Rate Policy" (ZIRP) beyond 2014. Extending "Operation Twist," in which the Fed sells short-term notes and swaps into longer-term bonds, would help keep bond yields submerged at artificially low levels. However, neither of these token gestures would materially increase the money supply, which is what Wall Street and Gold Bugs are thirsting for.

Bernanke did say to a skeptical Republican that QE-3 could inflate the value of the stock market "and therefore increase wealth effects for consumers in order to spur more spending." That's a dubious claim, since the top-10% of the richest Americans control 80% of the listed shares on the NYSE and Nasdaq. Only the wealthiest Americans benefit from QE. The rest of the US-population gets stuck with payer higher gasoline prices at the pump with QE.

However, Bernanke did pour some cold water on the simmering speculation over QE-3, "There may be some diminishing returns to further (QE) action. I'd be much more comfortable if Congress would take some of the burden from us," he said. Republicans at the hearing were quick to criticize the Fed chief, saying that QE-3 would be tantamount to spiking the punch bowl in order to help the Democrats and President Barack Obama, ahead of the upcoming Nov 6th elections. "I wish you would take QE-3 off the table," said Texas Rep. Kevin Brady, the ranking Republican on the committee. "I wish you would look the markets in the eye and say that the Fed has done too much," he added.

The month of May and the first week of June were brutal for President Barack Obama. Government apparatchiks said that the US-economy grew at a sluggish +1.9% annual rate in the first quarter of 2012. Worse yet, the US-economy which created an average of 226,000 jobs per month in the first quarter, only created an average of 73,000 in April and May. Alarmed by the ominously weak US-jobs report, the Dow Jones industrial nosedived on June 1st, plunging 275-points lower, its biggest daily loss since last November. The sudden selloff towards the 12,000-level wiped out the Dow's gains for the year. Also signaling fears of a recession, the yield on the 10-year Treasury note fell below 1.50%, a record low.

Likewise, on-line bettors at Intrade.com, lowered the odds of Obama winning his re-election bid to 53.5% on June 10th, - down from a 60% chance on May 1st. Conversely, for the Republican challenger, Mitt Romney, his odds of winning the presidency increased to 43.1%, compared with 37.4% at the beginning of May. Apparently, bettors at Intrade.com think the outcome of the Nov 6th election will hinge upon the value of the US-stock market in the months ahead. However, there's a big disconnect between the value of the US-stock market, and the health of the US-economy. The S&P-500 index has doubled from its March 2009, amid the weakest economy recovery since the Great Depression. Instead, the boom in the stock market, has only served to widen the gulf between the rich and the poor in America, where the number of food stamp recipients has doubled since 2008.

Given the political realities in Washington, - bond dealers on Wall Street that deal directly with the Fed are equally split on the likelihood of QE-3. Those betting on QE-3, think the Fed would unveil a $500-billion printing spree at its upcoming June 19th meeting. The other half thinks the Fed would stay politically neutral, and opt for extending Operation Twist. The stakes are high. Without the artificial life support of QE-3, the US-stock market could sink ahead of the upcoming election and torpedo Mr Obama's chances. On the other hand, a $500-billion printing operation could lift the Dow Industrials above the May 1st highs, and tilt public opinion in favor of the president, over his Republican challenger.

Mr Romney has already sent a public warning to the Fed, to keep its hands off the money printing press between now and Election Day. Romney told CNBC on June 1st, that the Fed's actions to boost the economic recovery have "really run their course." "QE-2 was not able to yield the economic benefit which they hoped it would be able to yield. I don't think we're looking for more. A QE-3 if you will, I don't think that will have any more impact than QE-2 did. The central bank should focus just on keeping prices stable," Romney added.

During the GOP presidential debate on Sept 7, 2011, Former House Speaker Newt Gingrich was asked if he would reappoint Ben Bernanke to run the Fed. He answered, "I would fire him tomorrow. I think he's been the most inflationary, dangerous, and power-centered chairman of the Fed in the history of the Fed. I think the Fed should be audited. I think the amount of money that he has shifted around in secret, with no responsibility and no accountability, no transparency, is absolutely antithetical to a free society," Gingrich said.

Romney concurred. "I'd be looking for somebody new. I think Ben Bernanke has overinflated the amount of currency that he's created. QE-2 did not work. It did not get Americans back to work. It did not get the economy going again. We're growing now at 1-½%," Romney said. Thus, the Fed chief must consider that he would certainly lose his job, if he takes the risk of launching QE-3, - and Obama loses the election. Worse yet, if Romney wins, many Tea Party Republicans could push for a full fledged investigation into the Fed's secret dealings over the past few years, including trillions of dollars of loans to the Wall Street banking Oligarchs. There could be an audit of the Fed's secret intervention tactics. The Fed could be stripped of its dual mandate, and left with a single goal of fighting inflation. For these reasons, the Fed is likely to vote against the risk of launching QE-3.

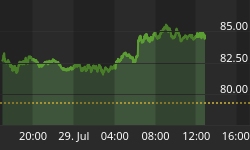

Still, many gunslingers in the Dow Jones industrials futures markets, are betting heavily on the unveiling of QE-3. The Dow finished +3.6% higher at 12,554 last week, - a remarkable feat. That puts the Dow +150-points above the level that prevailed just prior to the lousy June 1st jobs report. It seems as though economic data has a shelf life of only 24-hours, before it's etched-a-sketched away from the memory of psychotic traders. The Dow's gains were accompanied by signs of a stabilizing Euro, on ideas that Europe's political elite, would rescue the zombie banks in Spain. However, while the zombie banks can exist on artificial life, as zombies, they will hoard their cash, and would be very reluctant to lend to worthy borrowers, thus prolonging the Euro-zone's ongoing recession. Still, the recession in Europe is of little concern for hallucinogenic Bulls, anxiously awaiting their QE-3 fix.

However, US-retail investors were fleeing stock mutual funds for 14 straight weeks. They've yanked $46-billion out of the market since the start of the year. Just 53% of US-households owned any stocks in April, the lowest since 1998. As such, the average daily trading volume in US stocks on all exchanges has shrunk to 6.5-billion in April, compared with 12.1-billion at its peak in 2008. Whose left are high-speed trading firms, which now account for as much as two-thirds of all the volume on the stock markets . Yet high frequency traders are mostly scalpers, seeking to pocket a few pennies or $1 per share during the day. The rest of the players are money managers for high net worth individuals, hedge fund traders, mutual funds, and agents of the "Plunge Protection Team." In thinly trade markets, the actions of a few big players can have bigger impacts on the market's increasingly strange behavior.

There is growing suspicion that the "President's Working Group," otherwise known as the "Plunge Protection Team" is covertly intervening in stock index derivatives, on a daily basis, in order to place a safety net under the market, when risky bets go sour. For the past 15-years, traders have relied on the "Greenspan and Bernanke Put" to bail them out of tough situations. The Fed has a long history of springing into action to inject liquidity into the money markets, or "Jawboning" timely messages to the financial media, aiming to prevent the emergence of steep corrections on Wall Street that if left unchecked, could snowball into an outright Bear market, and plunge the US-economy into a nasty recession.

The "invisible hand of the Fed" causes short squeezes that lead to the sudden emergence of "miracle rallies," that defy logic. This conspiracy theory isn't based upon hard evidence, that's known to the public. Instead, it's supported by a "negative proof," or rather, the law of improbability. For instance, on June 6th, the Dow Jones Industrials surged +286- points to close at 12,414, its biggest gain of the year. The rally started early and gathered force in the final hour of trading, as short sellers scrambled for cover. The outsized gain had more than erased the biggest loss of the year: the -275-point plunge set off just a few days earlier. One floor trader was quoted by the media as saying, "In market language, it's called a technical bounce. There's no bad news today, so the market goes up. Frankly, it's that simple." Such an improbable explanation however, keeps conspiracy theories of Fed intervention alive.

Likewise, on June 12th, the Dow staged its second biggest rally of the year, shooting up +162-points, and erasing a big -142-point decline from the previous day. The big rally on Wall Street was highly improbable, because in the background, the yield on Spain's 10-year bond jumped to as high as 6.81%, and up more that 60-basis point since a €100-billion bailout of Spain's banks was announced. At 7%, big debtor nations are pushed to the brink of default. Yet the negative news was ignored and the US-stock market surged higher anyway. Chalk that outsized rally up to big bets on the launching of QE-3, or what Wall Street analysts like to call, "value investing" in the world's biggest casino.

The past year was very tumultuous for stock markets around the world. Yet the S&P-500 index has managed to defy the law of gravity, by posting a +3.5% gain from a year ago, while most of the world's markets tumbled, - succumbing to the turmoil that's roiling Europe. Compared with a year ago, Brazil's Bovespa has lost -32%, Germany's DAX-30 index is -24% lower, the Toronto Stock Exchange is -16.5% lower, Korea's Kospi index has lost -16%, Hong Kong's Hang Seng index fell -15.8%, and Japan's Nikkei-225 is -11%. Even the Footsie-100, the Siamese twin of the Dow Industrials is trading -5% lower from a year ago.

The S&P-500's superior performance is surprising, considering a quarter of its companies' revenues come from Europe! Moreover, a stronger US-dollar translates into weaker earnings for US-Multi-Nationals that earn 45% of revenues overseas. Yet the S&P-500 index is outperforming its foreign rivals. Is one company - Apple Inc is responsible for the S&P-500's supremacy in world markets? Most likely, the Fed is juicing-up the stock market, while central bankers in other countries are not playing that game.

On Aug 17th, 2011, two Fed chiefs said they're opposed to efforts of trying to prop-up the stock market. Philadelphia Fed chief Charles Plosser said "taking action after stocks have tumbled, signals that we are in the business of supporting the stock market." Likewise, Dallas Fed chief, Richard Fisher warned that the Fed "should never enact such asymmetric policies to protect stock market traders and investors. Some traders might view the easing of monetary policy as a "Bernanke Put," or the idea that the central bank will loosen credit after a stock-market decline," Fisher said. Fed intervention can buy some precious time for the White House, by placing safety nets under the market. Yet it would require a blast of nuclear QE-3 to lift the US-stock market to new heights and extend its 3-¼ year Bull Run.

Commodities hurt by Weaker Euro, Slowdown in China

The Continuous Commodity Index, (CCI) measuring an equally weighted basket of 17-commodities, has been caught in the grip of a year long slide. Its value is -21% lower than a year ago. The deepening recession in the Euro-zone, and a slowdown in the Chinese economy is blamed for undercutting the demand for industrial commodities, such as copper, iron ore, rubber, steel, and crude oil. There were big losses in the soft agricultural markets, for cocoa, coffee, and sugar.

In a strange twist of fate, the US-dollar has been getting stronger against the second most actively traded currency, - the Euro, by default, or by virtue of the fact that it looks less ugly than the Euro currency. In turn, a stronger US$ against the Euro is exerting selling pressure on a wide array of commodities. Some of the biggest casualties in the commodities markets have lost as much as half of their value from their peak levels of 2011. The price of cotton and natural gas are -53% lower than a year ago. Coffee is -41% lower, rubber is -34% lower, corn is -26% lower, sugar and silver are both -21% lower, and wheat is -18% lower. The wholesale price of unleaded gasoline is -12% cheaper than a year ago.

Virtually all of the top exchange traded commodities are lower in price than a year ago, with the exception of live cattle, up +16%, and Gold and soybeans that have scratched out gains of +5% from a year ago. In turn, there's been an unwinding of inflationary pressures worldwide. In Emerging nations, where commodities account for most of the consumer price basket, the drop in commodity prices could knock the official inflation rate to zero-percent by year's end. In order to reverse the deflationary trend in commodities, it would require another big blast of QE from the Fed, which in turn, would flood the world with cheaper US-dollars.

In the past, China's finance ministry has complained about the Fed's QE money printing operations. At a G-20 meeting in South Korea on Oct 26, 2010, Chinese Finance Minister Xie Xuren said that "issuers of major reserve currencies" -- code words for the United States - "must follow responsible economic policies." "Because the US's issuance of dollars is out of control and international commodity prices are continuing to rise, China is being attacked by imported inflation. The uncertainties of this are causing big problems. If other countries allow their currencies to appreciate freely against the US-dollar, then their exports will deteriorate. If they maintain rigid exchange rates against the dollar, their central banks will have to buy more dollars on the foreign exchange market, and this will increase liquidity in their own currencies, and further inflate commodity and stock prices," he warned.

Soon after Chinese Finance Minister Xie Xuren issued his warning to Washington, the People's Bank of China (PBoC) began to embark on a tightening campaign, which included five rate hikes, lifting its 1-year loan rate to 6.56%, in order to offset the inflationary effects of higher commodity prices, that were fueled by the Fed's $600-billion QE-2 scheme. China's inflation quickened to a 3-year high of +6.4% in June 2011, and factory prices were +7.5% higher in July 2011. China 's inflation was boosted by rising food costs, which soared +14.4% in the year through June . Pork, a staple meat for Chinese and the most closely watched commodity shot up +65% from a year earlier. Beijing is especially sensitive to rising food and energy prices that might stir social unrest and threaten its leadership.

As fate would have it, the PBoC's last rate hike to 6.56% in July 2011, coincided with the completion of the Fed's QE-2 money printing operation. Since then, the global commodity rally began to sputter out, as QE addicts were forced to go cold turkey. As Europe sank into recession, commodity markets fell into a year long slide. In China, the producer price index has gone into negative territory, and was -1.4% lower in May compared with a year earlier. With a negative inflation rate, there's less incentive for Chinese traders to buy Gold.

Last week, on June 7th, the PBoC lowered its one-year loan rate 25-bps to 6.31%, confident that inflation pressures would stay tame. The PBOC also lowered the required reserve ratio (RRR) for the biggest banks by 150-basis points to 20% in three moves since November. That has freed an estimated 1.2-trillion yuan ($190-billion) of fresh liquidity into the Shanghai money markets. So far, the liquidity injections haven't led to higher prices for commodities or the Shanghai red-chips market. Instead, turmoil in the Euro-zone, the slowdown in China's economy, and a weaker Euro have kept commodity markets under siege.

Euro Currency Crisis weakens Commodities

The initial knee-jerk reaction to the EU's €100-bailout of Spain's troubled banks was one of euphoria and relief. However, it only took a few hours before the alarm bells began to ring over the mushrooming size of Spain's public debt. In Madrid, Spain 's 10-year bond yield hit 6.83% on June 12th, edging closer to the 7% danger level that triggered bailouts for the governments of Greece, Ireland, and Portugal. There are also lingering worries that Greek voters might opt to throw off the yoke of EU austerity, and default on €423-billion of debts to foreign lenders .

The €100-billion bailout might prevent the collapse of the Spanish banks, unless depositors make another major run on the banks. Jittery depositors withdrew €66-billion from Spanish banks in April. However, the bailout would add to Spain's debt pile, taking it +10% higher to 90% of the country's GDP. And that's not good news, for anyone holding Spanish bonds.If the bailout comes from the ESM, rather than the EFSF, then the €100-billion debt incurred would be senior to Spanish government bonds. This means that existing government bonds already trading on the secondary market, would become junior bonds, to the ESM loans, and would lose value. Furthermore, owners of subordinated Spanish bank bonds could be forced into taking a big haircut. That could trigger another flight from the Euro.

The sovereign debt crisis in Italy and Spain is exerting downward pressure on the Euro versus the US$, which in turn, is weakening commodity prices. And matters for the Euro-zone are much worse that politicians are willing to admit. On May 29th, the Egan-Jones Ratings agency lowered its sovereign credit rating of Spain to single-B from BB-, citing the country's deteriorating economic outlook. "The nation's 9.6% budget deficit, 24% jobless rate and bank losses of as much as €260-billion weigh on the economy . Spain will inevitably be faced with payments to support a portion of its banking sector and for its weaker provinces. The assets of Spain's largest two banks exceed its GDP. We are slipping our rating to 'B'; watch for more requests for support from the banks and money creation," Egan Jones warned.

Indeed, foreign investors cut their holdings of Spanish debt to 37% of the total in circulation in April from 50% at the end of last year. However, Spanish banks were very active players in the ECB's 3-year loan program, having borrowed €300-billion. And much of that money was used to buy Spanish government bonds. As a result Spanish banks now own about 67%, of the government's debt. Now that those bonds are plummeting in value -- prices fall as yields rise -- Spain's banks and government are chasing each other in a financial tailspin. Among the largest holders of Spanish bonds are the country's international banking giants Santander and BBVA, which, through February, owned €60-billion and €49-billion, respectively.

Italian banks were also enthusiastic buyers of government's bonds - they own 57% of Italy's €2-trillion of bonds outstanding . As in the case of Spain, foreigners have been obliging sellers having dumped €242-billion worth of bonds to local Italian banks, and whittling their share of Italian bond outstanding to 35% as of March compared with 51% late last year. Bond traders figure that Italy would be next in line for a bailout, because of its 120% debt to GDP ratio and its shrinking economy, despite reforms initiated by Prime Minister Mario Monti. Yields on Italy's 10-year note jumped to 6.17% today, up from as low as 5.66% last week.

Gold Bugs betting Big on QE-3

So far this year, Gold has largely been held hostage to the gyrations of the broader commodity indexes. However, on June 1st, the price of Gold suddenly surged spectacularly higher, following the dismal US-jobs report. Hedge fund traders figured that the weak jobs report would be the smoking gun that pushes the Fed into launching QE-3 at the upcoming June 19th meeting. The price of Gold soared $80 /oz higher, above its intra-day low on June 1st, before settling at $1,625 /oz. However, on June 7th, Fed chief Bernanke stayed silent on the topic of QE-3. Gold quickly plunged $40 /oz within a few minutes, and skidded to as low as $1,561 /oz, before strong hand buyers stepped in.

Seeking shelter from the Italian and Spanish bond markets, many global investors shifted from Euros and into Gold, especially when the yellow metal found solid support at the $1,540 /oz level in the month of May. The slide to $1,540 equaled a -20% correction from Gold's all-time high set in August of 2011. Thus, Gold fell to the threshold of a bona-fide Bear market, but escaped the claws of the grizzly bear. The Gold market has since rebounded for a second time towards overhead resistance seen at the $1,630 /oz area, buoyed by big bets that the Fed would vote to launch QE-3 at its upcoming meeting. A $500-billion blast of nuclear QE-3 would weaken the value of the US-dollar and in turn, boost commodity prices. QE-3 could signal the end of the deflationary trend that been plaguing commodities, and signal the beginning of an intermediate rally in the Gold market, that could be sustainable.

However, in the opinion of the Global Money Trends newsletter, - the Fed is trapped in a political minefield, and won't offend the Republican Party. Therefore, the Fed is expected to stay politically neutral ahead of the Nov 6th elections, and leave QE-3 on the back burner (assuming Greece does not exit the Euro). If correct, it would be difficult for a Gold rally to gain traction. Barring a shift to QE-3, other possibilities that could lift Gold higher are "Black Swan" events, such as a Euro currency crisis, that's trigged by Greece's Far-Left, or a surprise military attack on Iran's nuclear facilities this summer. The good news for Gold Bugs is that a sustainable bottom for the yellow metal appears to be firmly in place.

This article is just the Tip of the Iceberg of what's available in the Global Money Trends newsletter. Subscribe to the Global Money Trends newsletter, for insightful analysis and future predictions about the (1) top stock markets around the world, (2) Commodities such as crude oil, Gold, copper and base metals, (3) Foreign currencies, such as the Australian and Canadian dollars, Brazil real, the Euro and Japanese yen, (4) Central bank interest rates and global bond markets, (5) Central bank Intervention techniques (6) and key Credit Default Swap markets.

GMT filters important news and information into (1) bullet-point, easy to understand reports, (2) featuring "Inter-Market Technical Analysis," with lots of charts displaying the dynamic inter-relationships between foreign currencies, commodities, interest rates, and the stock markets from a dozen key countries around the world, (3) charts of key economic statistics of foreign countries that move markets.

Subscribers can also listen to bi-weekly Audio Broadcasts, posted Monday and Wednesday evenings, with the latest news and analysis on global markets. To order a subscription to Global Money Trends, click on the hyperlink below,

http://www.sirchartsalot.com/newsletters.php

or call toll free to order, Sunday thru Thursday, 8-am to 9-pm EST, and on Friday 8-am to 5-pm, at 888-808-7978. Outside the US call 561-391-8008.