Gold Investments Weekly Newsletter is now featured on the Irish National State Broadcast company RTE in their new Commodities section of RTE Business - http://www.rte.ie/business/commodities.html .

Newstalk 106 featured Mark O'Byrne, one of our directors in their 'That's My Business' slot when they interview a representative from a prominent Dublin Business every Monday from 2pm. Mark spoke to Brendan Byrne, who was standing in for Damien Kiberd, about the merits of diversifying some of one's investments into precious metals.

The Irish Independent featured our Sales and Marketing Director, Stephen Flood in a feature they did about the busy lives of the modern day executive in modern day Ireland.

Weekly Markets

Precious Metals

Gold was up 2.8% for the week. On the New York Mercantile Exchange, gold for April delivery closed at $446.80 an ounce up from the close of $435.10 an ounce last Friday. It closed up $3.40 on Friday alone and reached an intraday high of $448 after the bad Trade Deficit numbers and Alan Greenspan's warning about the US' burgeoning budget deficits.

Silver was up 2.5% for the week, the March contract turning higher to close at $7.535.

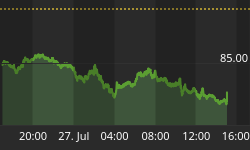

Platinum was largely flat for the week after last weeks 1.3% increase. April platinum went down $6.40 to $870 an ounce. Spot platinum reached $866.50/871.50.

Palladium closed the week at $203.80 to be largely unchanged for the week and consolidating after last weeks 15.6% gain.

Performance (% Change)

| Current Level | 5 Days | 1 Year | 5 Year | |

| Gold | 442.10 | +2.9% | +8.6% | +54.6% |

| Silver | 7.48 | +3.7% | +6.4% | +59.8% |

| S&P | 1200.08 | -1.8% | +5.2% | -11.5% |

| ISEQ | 6084.30 | -2.9% | +16.4% | +14.6% |

| FTSE | 4982.00 | -1.1% | +9.7% | -23.0% |

Gold's desirability as an macroeconomic and inflationary hedge was shown during the week. The Commerce Department reported that the U.S. trade deficit came in at a wider-than-expected $58.3 billion in January, the second-worst deficit on record. And late Thursday, Greenspan told a New York audience that budgetary red ink is the most worrisome of the deficits confronting Washington policymakers. Earlier in the week the 'Sage of Omaha' Warren buffet had been even more explicit in warning that the massive debt levels may lead to the US becoming a 'sharecropper's society' whose economic destiny is controlled by foreign creditors rather US citizens and elites. Sharecroppers are peasants who do not own their own house or land and must pay in tribute to their creditors or landlord a share of their crop. Buffet's is the world's second richest man and it's most successful investor and his opinions on the global economy and finance are rightly highly respected.

Friday's gains in gold came without the benefit of a weaker U.S. currency, which firmed in foreign-exchange dealings showing that gold's appreciation is not purely a dollar depreciation story and that there are a number of other important fundamental factors.

Nell Sloane of Nell Sloane Futures said that they believed that "the rotation away from US financial assets will continue and both flight to quality and inflationary elements will remain a positive driving force for gold prices. We also continue to see bullish gold forecasts from a number of Bank analysts but most of those forecasts are assuming a progressively lower US Dollar as the primary force behind gold strength. Just to reiterate the potential for energy price driven inflation, we point to the overnight forecast from the IEA, who predicted that Chinese demand for oil was set to rise by 22% in the coming year. While the IEA Chinese oil demand growth rate, falls short of the 33% Chinese demand growth rate predicted by the US EIA, it is clear that oil supplies are set to remain tight for at least the coming 9 months and that should keep the cost push inflation issue in position."

Market analyst and financial newsletter writer Peter Grandich said that "The 'Three D's' -- dollar, debt and deficits -- continue to provide strong support for gold. These three factors are "clearly heading in a direction that can only positively impact gold's short-to-intermediate direction," he said. Even more importantly this trend looks to be for the long term as these macroeconomic imbalances will take a number of years to readjust.

With gold bullion up $10.65, indexes tracking unhedged gold mining stocks, the HUI Gold index, were up 2%.

Gold is at a 3 month high. It is only $8.70 from breaking the 17 year high of $454.20 hit this last December 2nd (gold hit $499.75 on December 14, 1987). It is up 7.8% in the last 30 days and up 10.3% in the last year. Should it take out $454.20, most technical analysts believe it should rally up until it's 1987 highs and the important $500 might prove to be the next point of resistance. Incidentally, the Dow Jones Industrial Average was at some 2,000 in December 1987 and it's average for the last twenty years is 2,500.

Also of importance was the work of the Gold Anti-Trust Action Committee or GATA consultant Dan Norcini who showed how the price of gold is much lower than it should be when compared with other commodities. Using the closing prices of the Reuters CRB for the period when last it was above the key 300 level in late 1980, Norcini showed that gold is very undervalued especially when compared to all other commodities. This GATA say is further proof of manipulation by Central Banks and corporate banks of the gold price in order to disguise the extent of inflation in the US economy which would necessitate increases in interest rates.In the last 5 months of 1980 the CRB averaged 300 and the gold price averaged $600 per ounce in stark contrast to the current CRB level of 318 and gold at $444.

Oil

Light, sweet crude for April delivery rose 89 cents to $54.43 and was up a further 1.21% for the week. Intraday, oil came within 2 cents of its all-time high of $55.67 this past Wednesday after the International Energy Agency estimated global petroleum demand would grow far faster than previously expected in 2005. The IEA boosted its demand numbers by almost 300,000 barrels per day thanks, in large part, to the US' voracious appetite for oil and Asia's booming industrialising economies.

OPEC has reached its production limit, and trying to stretch output by one million barrels per day isn't likely to lower oil prices, Algeria's minister for energy and mines said. Chakib Khalil said prices were high because of world economic growth - particularly in the United States and China. "OPEC has reached its production limits. It doesn't have much production capacity," he said. "If it came to a crunch, it has capacity for one million barrels (more per day), and I don't think a production increase would influence the barrel price."

Also of significance to oil's long term price movement was the release of the US government's Department of Energy commissioned and sponsored report acknowledging the reality of 'peak oil' or the peak of global oil production and gradual depletion of existing finite supplies. "World oil peaking is going to happen," the report says. Only the "timing is uncertain"."The development of the US economy and lifestyle has been fundamentally shaped by the availability of abundant, low-cost oil. Oil scarcity and several-fold oil price increases due to world oil production peaking could have dramatic impacts ... the economic loss to the United States could be measured on a trillion-dollar scale," the report says.

The authors of the report also dismiss the power of the markets to solve any oil peak. They call for the intervention of governments. "Intervention by governments will be required, because the economic and social implications of oil peaking would otherwise be chaotic."

While oil is now at record levels in terms of today's dollars it must be remembered that it is still a long way of it's 1980 peak of some $90 adjusted for inflation and the loss of the dollar's buying power. Gold is still some 50% below it's 1980 highs but in real terms it is 75% below it's price in 1980. There is no other asset class that can be bought for around 25% of it's real price 25 years ago. Adam Hamilton's excellent Zeal Intelligence compiled the following important and informative chart.

Other Commodities

Commodities price gains were broad-based, with the Reuters CRB Index surging 4.1% to 318.61 up 3.46 on Friday alone. The CRB is up 12.2% already this year.

The Reuters CRB Index (basic components include hard tangible assets such as Metals, Textiles and Fibers, Livestock and Products, Fats and Oils, Raw Industrials, Foodstuffs). One of the CRB index's greatest strengths is the fact that there is an equal weighting of all of its 17 components. This weighting assures that no price increase in any single commodity, like oil, can significantly skew the entire index. Significant moves in the CRB are only possible when the majority of its component commodities are moving in unison with a particular primary trend. The most important commodities - gold, oil, and silver only account for 3/17th of the entire index.

The Goldman Sachs Commodities Index increased 2.3% after last weeks 3.4% gain, increasing year-to-date gains to 20.4%. The GSCI is a world production-weighted commodity index which next year will be composed of 24 liquid exchange traded futures contracts. The GSCI includes energy, industrial metals, precious metals, agricultural and livestock products.

Cocoa touched new contract highs and the soybeans, corn and wheat posted impressive gains. A combination of technical chart signals, soaring heating oil futures, and most importantly bullish world global demand forecast triggered the continuing rally. Chicago Board of Trade soybean, wheat and corn futures finished higher, extending the bullish trend. Speculative buying by commodity funds fuelled a rally across the entire grain complex. The May soybean futures contract traded 23.25 cents higher at $662.50 a bushel. The CBOT May corn contract settled 4.75 cents higher at $2.24.75 per bushel. May Cocoa futures at the New York Board of Trade rose to a fresh contract high of $1,842 a metric ton, but later eased a bit, as funds bought aggressively amid rising tensions in top-producer Ivory Coast. May settled $51 higher at $1,804 a metric ton. Raw sugar futures traded to highs on the Nybot, scaling several chart barriers as the trade and funds bought, while producers sold into the advance. May settled up 0.20 cent at 9.17 cents and July closed up 0.16 cent at 9.29 cents. Arabica coffee futures ended lower on the Nybot on Friday as funds pocketed profits after the market initially gapped up to a five-year high, the highest levels since December 1999. New highs were touched across the board before the drop. The Nybot May contract settled 1.45 cents lower at $1.3665 a pound. March copper ended off 1.4 cents at $1.481 a pound. According to the latest inventories data compiled by Nymex, copper stood at 45,575 short tons as of the close of business on Thursday, down 523 short tons from the previous day.

The Reuters CRB is now up an unprecedented 9 days and 5 weeks in a row and the breakout above 300 is decisive. Inflationary fears with a weakening U.S. dollar have enticed speculators to shift dollars away from stocks and bonds to hard assets, like commodities.

The rapid move up may be followed by weakness in the short term as the CRB has moved far above it's 50 and 200 day moving averages. However, with massive global demand and poor supply due to underinvestment in commodities due to the low prices of the last 20 years it looks like this is a long term bull market. Adam Hamilton of Zeal Intelligence has importantly pointed out that adjusted for the significant inflation of the last 25 years the commodity complex is still way below it's 1974 peak at 961 and it's 1981 peak at 753.

Currencies

The dollar had its biggest weekly decline versus the euro in almost three months after a government report showed the US trade deficit continued to widen. The U.S. dollar index was lower by 1.28% for the week despite the large jump in market bond yields. The euro index was higher by 1.62% rising to $1.3457, and the yen is higher by 0.7% to 104. The currency markets are sure to remain on edge with regard to the actions of Central Banks globally and especially in Asia and their desire to diversify out of the falling dollar. "The path of least resistance for the dollar is down," said Murray Gunn, director of currencies in Edinburgh at Standard Life Investments, which manages about $193 billion. "The current- account issues are not going away. The dollar is still in a long- term down trend, and there's no evidence of a change."

The Swiss franc, Norwegian krone, Canadian dollar were all up about 2%. The only currencies to underperform the dollar for the week were the Brazil real which declined by 1.3%, the Turkish lira by 1.2%, and the Mexican peso by 0.4%.

On Friday, India's central bank governor, Yaga Venugopal Reddy told reporters that diversification of foreign exchange reserves was being discussed at the central bank, similar to recent comments from Japan and South Korea, the world's first and fourth largest holders of reserves. India's reserves holdings are the sixth largest in the world. "Yes it is being discussed. We are always discussing. It's a continuous process," Reddy said. "It is an ongoing debate with all central banks and you cannot expect a central bank governor to say anything further on this."

His comments sparked speculation on whether the talk of diversification was part of a coordinated plan by Asian central banks. Asian economies hold almost $2.5 trillion of reserves, and the majority are thought to be invested in U.S. dollar assets. Talk of a shift away from dollars, either in existing holdings or in allocations of new reserves, creates a great deal of nervousness in global markets over the dollar's prospects.

Stocks

For the week, the Dow Jones industrial average was down 1.5% to 10,774. The Standard & Poor's 500 index was also down 1.8%, to 1,200.08 and the Nasdaq closed at 2041.6 down 1.4%.

Interest rates, twin deficits and oil seem to have affected the major indices with the Dow, Nasdaq, and S&P ending near their lows of the week. Although the Dow and S&P are still not far from their 3½ year highs. On Friday, the indices opened mixed and near unchanged, but headed lower in the afternoon and all three indices ended near their lows of the session with losses of 0.71%, 0.88%, and 0.76%, respectively.

Bonds

Ten-year Treasury Note yields rose 22 basis points this week to 4.54%. The yield sits at 7 month highs and had its biggest 1 week move in 10 months. The yield gained 5.22% this week. The Long-bond or the 30 year Treasury Bond yields jumped 16 basis points to 4.81%.

U.S. 10-year Treasury notes had their biggest weekly drop since May as rising commodity prices and increased consumer demand for imported goods bolstered speculation inflation will accelerate. Investors pushed down government debt prices on concern faster inflation will erode the value of fixed-income payments. The tumble drove up yields and led to higher borrowing costs for consumers and companies. Some investors expect the rise in yields to continue.

U.S. 10-year Treasury notes may fall this week as rising oil and commodity prices bolster speculation that inflation will accelerate. Ried, Thunberg & Co.'s index of investor sentiment for government securities fell to 38, the lowest in two months, from 39 a week earlier. Readings below 50 mean the investors surveyed expect 10-year note prices to fall by the end of June. The 45 international money managers polled by the Jersey City, New Jersey-based bond-research firm manage a combined $1.29 trillion.

A majority of the survey participants said oil prices will remain above $50 a barrel, suggesting higher inflation may erode the value of fixed-income securities. Investors said there is a risk the Federal Reserve will raise its benchmark interest rate in bigger increments, after six quarter- percentage point increases since June. "At $50 it becomes a concern that maybe you start to see inflation become more important," said Ken Anderson, a survey participant who manages $11 billion in fixed-income investments at Evergreen Institutional Management in Charlotte, North Carolina. "If inflation becomes more of a problem, the probability of the Fed increasing by more than a quarter-point becomes more likely."

"Profit margins have peaked, inflation is on the way up, and those aren't generally good things for stocks," said John Caldwell, chief investment strategist for McDonald Financial Group, part of Cleveland-based KeyCorp. "So weakness in the bond market on top of that tends to make people skittish .... It just makes people question their thinking that much more."

The Treasury Department tomorrow releases data on net purchases of U.S. financial assets by international investors in January. Last month's report showed holdings of Treasuries increased by a net $8.34 billion in December, compared with $32 billion in November. The U.S. relies on foreign purchases of its debt to fund a record budget deficit. International investors own about half the $4 trillion in marketable Treasury securities outstanding. "Even if they reduce their buying at the margin it will have impact on the market," said Toutoungi. Japan is the largest foreign owner of Treasuries, holding more than $700 billion. Japanese Prime Minister Junichiro Koizumi said last week his country should consider diversifying its currency holdings, the world's largest. Finance Minister Sadakazu Tanigaki later said the government has no plan to shift its reserves.

Weekly Commentary

America's Twin Deficits

The U.S. Budget Deficit widened to the biggest monthly gap ever on surges in military, homeland security and Medicare spending, adding fuel to the debate between President George W. Bush and Congress over taxes and spending. The $113.9 billion monthly shortfall compares with the previous record deficit of $96.7 billion in February 2004, the Treasury said in Washington. Treasury said it was the largest monthly shortfall on record. The U.S. government ultimately reported a record deficit of $412.3 billion in fiscal 2004, which ended Sept. 30.

President Bush submitted a $2.6 trillion budget request for next fiscal year that includes efforts to boost spending for defense and homeland security. Economists predicted a February deficit of $100 billion, the median of estimates in a Bloomberg News survey and it was far wider than most Wall Street forecasts. Wall Street analysts polled by Reuters had on average put the deficit at $95 billion in February, though forecasts ranged from $85 billion to $115 billion. Military spending so far this fiscal year totalled $194.2 billion, up 6.9 percent from the first five months of fiscal 2004, according to the Treasury.

"The resolution of our current account deficit and household debt burdens does not strike me as overly worrisome, but that is certainly not the case for our fiscal deficit. Our fiscal prospects are, in my judgment, a significant obstacle to long-term stability because the budget deficit is not readily subject to correction by market forces that stabilize other imbalances," Greenspan said in a speech to the Council on Foreign Relations in New York.

US Government Budget Surplus / Deficit 1972 - 2002

Source: Congressional Budget Office, Chart by Marianna Quenemoen

The U.S. Trade Deficit widened to $58.3-billion, the second-biggest on record. The trade data imply another big U.S. current account deficit for the fourth quarter, set for release Wednesday. Analysts estimate the deficit at $183-billion, up from $165-billion in the third quarter. The bloated current account imbalance requires a huge inflow of foreign capital to finance it, and many observers believe higher interest rates will be necessary to keep attracting all that foreign money. Should it rise the US markets would need to attract $2.9 billion dollars every single market day in order just to maintain the current levels of the dollar and interest rates. This is clearly unsustainable.

Eamonn Fingleton, former City editor of The Sun newspaper and editor for the Financial Times and Forbes, whose website www.unsustainable.org studies the yawning trade deficit and the problems they will inevitably bring, asks "How big is a trade deficit of $570 billion dollars?" He gets out his calculator, and answers, "If delivered in dollar bills, it would weigh 510,000 tons - or about eleven times the weight of the Titanic. The money would require a fleet of 4,500 Boeing 747 freighters to transport. Placed end to end in dollar bills, it would stretch about 56 million miles - or about half the way to the sun. If the dollar bills were stacked one on top of the other they would rise 39,000 miles into space."

On a more serious note he continues that the trade deficit is "the worst any major nation has ever suffered in peacetime. And the issues are not just the demise of American industries but the very future of American power .... Economic history tells us that chronic trade deficits first enfeeble a nation and eventually, if they remain unchecked, ruin it. The decline of the once-great Ottoman empire, for instance, stemmed in substantial measure from its failure in its last decades to control its spiralling trade deficits. Chronic trade troubles also precipitated the decline of Argentina, a nation that began the twentieth century at the top of the First World and ended it at the bottom of the Second."

It is also revealing to look at the history of the so-called Group of Seven nations (these nations comprise Japan, Germany, France, Italy, the United Kingdom, and Canada, as well as, of course, the United States). Although some of them have on occasion run deficits even larger than America's recent 5 percent figure, they have invariably done so only at times of extreme distress. Specifically in most cases such deficits were incurred either in the desperate circumstances of the two World Wars or in the immediate aftermath of those massively destructive wars. The one other occasion when a G7 nation exceeded America's 2002 figure was a deficit of 7.7 percent incurred by Italy in 1924. But that precedent is cold comfort for anyone trying to downplay America's current trade crisis: a glance at the history books reveals that Italy in the mid 1920s was a true basket case so much so that its problems paved the way for the rise of Fascism (Mussolini seized dictatorial powers in 1925)."

Clearly these imbalances are not a recipe for long term healthy economic growth.

Gold Bullion's Historic Relationship with Equities and the Reversion to the Mean

Reversion or regression to the mean or average is the proven mathematical or statistical phenomenon whereby values revert to their long term mean or average. It is one of the most powerful forces in all investing. There is a tendency over time of investment returns to move toward a norm, or mean. This "investment law of gravity"-applies not only to the relative returns of equity mutual funds, but also to returns of stock market sectors, to returns of common stocks as a whole and to returns on all other asset classes over long periods such as the 20, 30, or even 40 years during which people invest for retirement.

Today's or recent histories out performing asset classes are more than likely to be tomorrow's ordinary or underperforming asset classes and conversely yesterday's underperforming asset classes are likely to be today's and the near future's outperforming asset classes. Quite simply put there are long term economic cycles and asset price trends and what goes up by a significant amount will come down and what has gone down or remained static for a long period will eventually go up. The oft heard warning that 'past performance may not be a reliable guide to future performance' is very very true and indeed contrarian investors such as Warren Buffet would contend that the better past performance has been the more likely that that particular asset class will under perform subsequently.

Dow Jones Versus Gold Ratio and psychology of the 'herd'.

Interestingly the long term or 26 year average of the number of ounces of gold required to buy 1 unit of the Dow is around 10. Thus were the law of reversion to continue we could again expect a DJIA / Gold average of around 10 which might result in a Dow Jones price of some 8000 and a gold price of $800. Or were the DJIA retest it's recent lows in October 2002 at 7286 this would equate to a gold price of some $730 or some 65% above it's current price.

Many respected financial analysts such as the venerable and internationally respected Richard Russell who has been writing his financial newsletter, the Dow Theory Letters, since 1958 and is quoted in such publications as Bloomberg magazine, Barron's, Time, Newsweek, Money Magazine, the Wall Street Journal, the New York Times, Reuters, and others believes that Dow and gold will cross at 3000 - that is, the Dow will be 3,000 on the same day that gold is $3,000 an ounce. Russell states, "The odds are that in due time the Dow/gold ratio will return to the mean or perhaps much lower. That, in a nutshell, is an important long-term argument for holding real money - gold. The Dow/gold ratio is telling us that today stocks are still near their highest level in history in terms of gold. And gold is near is lowest level in history in terms of the Dow .... Russell forecast - I see an extended period, maybe multi-years, in which gold will outperform the Dow. It would not shock me to see the ratio return to 1 to 1 some day."

While we would be surprised were a 1 to 1 ratio to come about there can be little doubt that a reversion to at least the average ratio of around 10 is more than likely.

Quotes of the Week

"Asian banks have reduced the share of deposits held in U.S. dollars in favour of other currencies like the euro .... The shift was most evident among Indian banks, who cut their share of dollar deposits placed abroad to 43 percent from 68 percent during from 2001 to end-September 2004. The share of U.S.-dollar-denominated deposits placed with Asian banks fell to 67 percent from 81 percent in September 2004 compared to 2001 .... The BIS banking statistics provide some tentative evidence that the deposits placed abroad by banks in the region have been increasingly denominated in currencies other than the U.S. dollar .... The above figures are suggestive of such a shift away from US dollar exposure for the region's banking sector."

Bank for International Settlements, (BIS), Central Bank's Central Bank, Latest Quarterly Report.

"Japan should 'in general' consider the necessity of diversifying how it invests foreign reserves. I think it's necessary to diversify the investment destinations' of foreign reserves."

Junichiro Koizumi, Prime Minister of Japan

"Warren Buffett recently made headlines by saying America is more likely to turn into a "sharecroppers' society" than an "ownership society." But I think the right term is a "debt peonage" society - after the system, prevalent in the post-Civil War South, in which debtors were forced to work for their creditors."

Paul Krugman, New York Times

"The evidence grows that our trade policies will put unremitting pressure on the dollar for many years to come .... Without policy changes currency markets could even become disorderly and generate spillover effects, both political and financial. There are deep-rooted structural problems that will cause America to continue to run a huge current-account deficit unless trade policies either change materially or the dollar declines to a degree that could prove unsettling to financial markets .... Presently, most foreign investors are sanguine: They may view us as spending junkies, but they know we are rich junkies as well. Our spendthrift behaviour won't however, be tolerated indefinitely. If nothing is done, he said, the United States will continue to transfer ownership of assets to foreigners to finance American over consumption .... In the last 10 years foreign powers and their citizens had accrued about $3 trillion worth of US debt and assets such as equities and real estate. At current rates in another 10 years' time the net ownership of the US by outsiders would amount to $11 trillion .... A decade ago their net ownership was negligible .... There could be dangerous consequences if these trends continue. Within a decade, the US would be compelled to deliver 3 per cent of its annual output to the rest of the world simply as tribute for the overindulgences of the past. This annual royalty paid [to] the world would undoubtedly produce significant political unrest in the US. Americans will eventually chafe at the idea of perpetually paying tribute to their creditors and owners abroad .... Americans end up owning a reduced portion of our country while non-Americans own a greater part. This force-feeding of American wealth to the rest of the world is now proceeding at the rate of $1.8bn daily .... A country that is now aspiring to an 'Ownership Society' will not find happiness in - and I'll use hyperbole here for emphasis - a 'Sharecropper's Society.' But that's precisely where our trade policies, supported by Republicans and Democrats alike, are taking us."

Warren Buffet, Berkshire Hathaway

"The Trade Deficit last year came to $617 billion, up from $495 billion the year before. It is rising as fast as the money supply...and as fast as California houses. Alan Greenspan told Congress that this represented no "crisis," just a "serious problem." He is right. It is a serious problem on its way to becoming a crisis. Greenspan hopes it doesn't get there before next January, when he leaves office. Like so many of the other things that Greenspan tells the politicians - the Fed chairman's remarks on America's trade/current account deficits were carefully crafted to deceive. He told the pols, for example, that even though deficits must be funded from overseas, it makes little difference if foreigners or Americans themselves lend the nation money. It makes little difference to God, we suspect. But it makes a big difference to Americans. If we borrow $50 from our children, the family's net financial position is unchanged. But if we borrow it from an outsider, the family has a $50 obligation beyond the family itself. Each time we make an interest payment, the money passes to outsiders and we are that much poorer. Likewise, he says we needn't worry about the deficits because America's economy is so "flexible" and so able to "deal with shocks." He must know, but does not mention, that its flexibility is only in its credit joints - which stretch remarkably. Each time the country is threatened with an economic shock, since Greenspan has been at his post, the reaction has been to stretch credit. The shock has not really been dealt with; it has only been made worse, and postponed. The crisis will still come; it will be even more severe because people owe more money."

Bill Bonner, Editor of The Daily Reckoning and Author of 'Financial Reckoning Day'

"Over the past five years total debt has grown by roughly $6.1 trillion or about 33%. This is against a backdrop of GDP growth of $1.9 trillion or 19%. Meanwhile Personal Income grew $1.2 trillion less than 15% while consumer debt grew $3.2 trillion up 46%. Debt is growing at a faster rate than income. In 2000 debt to disposable income was 98% and in 2004 it had increased to 120%. Numbers in Canada, Britain are not a whole lot different and indeed in Britain they are worse. While household assets prices have been increasing they are only 70% of disposable income. Debt is growing even faster. The housing boom over the past decade is growing at a faster rate then even in the late 1980's that ended in a huge housing and property collapse. Yet we are told there is no bubble."

David Chapman, Union Securities Ltd, Safe Haven

"Commodities, the solid basics that make the world go around, deserve respect. A new bull market is underway, and it is in commodities - the 'raw materials,' 'natural resources,' 'hard assets' and 'real things' that are the essentials of not just your life but the lives of everyone in the world .... I'm talking corn, coffee and cattle, oil and gas, grains and metals .... China is using more commodities than any other nation in the world and at a faster rate, making it the world's No. 1 consumer of copper, steel, iron ore (to make steel) and soybeans. It's the No. 2 consumer of oil and energy products. You really cannot be a successful investor in stocks, bonds or currencies without understanding them .... U.S. investors were too distracted by their own booming economy and stock market in the 1990s to invest any money in increasing productive capacity of raw materials, agricultural products and other hard assets," writes Rogers. "And thus the seeds of the current commodities bull market were sown throughout the world: exploding demand for commodities at the very time that supplies were being depleted and investment in the natural resources infrastructure was virtually nonexistent. With that kind of supply-and-demand imbalance, prices can go in only one direction, and that's up."

Jim Rogers, Quantum Fund, Author of the 'Adventure Capitalist' and 'Hot Commodities'

"The current exceptional rates of economic growth cannot continue indefinitely. There is increasing concern over growing imbalances, especially ... the large twin deficits of the United States of America, with the potential associated risks to financial stability. We do believe that, if there is [economic] variance, it is more likely to be on the downside, rather than the upside. This would then have a serious impact on the revenue expectations of our member countries."

Shihab-Eldin, OPEC Chief

"Statements from several Opec representatives suggesting that the global economy has become immune to any negative impact from higher crude prices look disingenuous"

International Energy Agency

"The American spirit of "buy now and pay later" - or never - has been a driving force behind this unprecedented housing market. Gone are the days of saving a hefty down payment and striving to pay off your house in 30 years. Today, the typical first-time home buyer or vacation-home buyer might finance the entire cost of the house and pay only the interest owed on the loan for the first several years. The latest option? A monthly "minimum payment" that doesn't even cover the interest .... Such innovations have, no doubt, been a boon to buyers who might have otherwise spent years socking away a down payment or paid a premium for a 30-year fixed-rate loan on a house they planned to own less than five years. And judging by historically low default rates, homeowners have been able to handle their growing debt burdens. Then again, buyers have been experimenting with more aggressive financing in the best of all times, when interest rates remain low and home prices continue to appreciate. "Mortgage markets have been so flush with cash that home buyers are able to layer one risk on top of the other," said Keith Gumbinger, vice president of HSH Associates. "It's possible to borrow more than the value of the home, put in no money of your own and pay a minimum monthly payment.""Not only do you not own any of your home, but you may be piling up additional debts that could quickly exceed the value of the home," said Gumbinger, adding that the interest rates on these loans adjust every one to three months. "There are no guarantees that rates will remain at comfortable levels and no guarantee that home prices will continue to go up.""You could find yourself in a rather uncomfortable circumstance," he said."

Sarah Max, 'Risky Real Estate Moves', CNN Money

The Housing mania will end in tears. Today's tales of rampant real-estate speculation sound just like what we heard at the peak of the tech bubble. And we all know what happened when that bubble burst. What is different -- and far more dangerous -- about the real-estate mania than the stock-market mania is that anyone with a pulse can get 100%-plus financing for housing -- a fact made quite clear by the story (and one that many folks have learned firsthand). Many people can control multiple properties via lax lending standards. It has been cheap and easy financing that has enabled the mania, in turn promoting even looser lending standards as the whole process has fed on itself. And, when the housing bubble does pop, folks will find out about the downside of leverage. The fact that our financial system is so larded up with bank assets (in the form of loans collateralized by real estate) means that the implosion will impact the economy. Then, as soon as lenders start taking hits on real estate, they will tighten up lending standards, exacerbating the problem .... I think it's safe to say that this mania in real estate cannot get too much crazier. Yet, it's not possible to say how much longer it will last. What is 100% knowable: Given all the speculation financed by borrowed money, this will end in tears, and the ramifications will be far-reaching. In case you're wondering what it might look like, there is a group of islands where there isn't enough real estate for everyone -- and where real-estate prices have declined for 10 years now. It's also home to the world's second-largest economy. It's called Japan.

Bill Fleckenstein, President of Fleckenstein Capital, MSN Money Columnist

"It is possible home prices in some areas of the country were too lofty but a sharp nationwide drop or destabilising contraction does not seem the most probable outcome. House prices ... like those of many other assets, are difficult to predict, and movements in those prices can be of macroeconomic significance."

Alan Greenspan, Federal Reserve Governor

Key Events in the Week Ahead

Most importantly on Wednesday is the release of the U.S. current account deficit figures for the fourth quarter of '04.

Also on Wednesday, OPEC oil ministers meet in Iran. It is a gathering that will be closely watched as market players debate where the price of oil is headed. It is the first meeting of OPEC in Iran in more than three decades.

Also on Wednesday figures for February housing starts and building permits will be released.

On Thursday the Philadelphia Fed index of manufacturing activity comes out.

Friday sees the release of the University of Michigan consumer sentiment survey.