Lets start with an anecdotal data point. In the year 2007, the US paid $200 billion in interest costs on its outstanding government debt. In 2012 the US will pay approximately $200 billion on its outstanding government debt. Of course the reason this set of circumstances can occur is courtesy of US Federal Reserve interest rate suppression as today the US has $7 trillion more in debt outstanding than was the case in 2007. Just what happens when US interest rates ultimately start to rise? Clearly a question of incredible importance on so many levels, but we're not there yet.

We all know the US Federal Reserve has practiced both interest rate suppression and monetary expansion (printing money) as their modus operandi of supposed economic stimulus. Unfortunately, interest rate suppression has given the political community a lay up in terms of continued and unabated fiscal profligacy, in which they have so eagerly partaken. There will be a "price" for this at some point, but the piper has not yet arrived to the party. There is clearly further method to the madness, if you will. In a period of macro deleveraging, the Fed necessarily needs to attempt to keep GDP above the general level of interest rates. Theoretically this allows the backdrop conditions to come into being for debt to be paid down while not further exacerbating already in place deflationary pressures. Since the Fed itself can only impact GDP indirectly, they attack the second part of the equation that is interest rates and simply keep their fingers crossed on GDP.

Quite important to investment decision making within a rate suppression environment, and from a very academic standpoint, interest rate suppression by the Fed is their attempt at raising the net present value of alternative asset income, or cash flow streams. By systematically and purposefully eliminating acceptable returns from safe investment choices offering income streams (think Treasuries, CD's, etc.), the Fed essentially forces those desirous of income to seek out higher risk alternatives such as equities, income oriented real estate investments, etc.

Certainly these collective actions by the Fed directly distort the character of the broad financial markets and necessarily influence the behavior of investors. As Jim Grant has so correctly opined, in a free capital market interest rates act as "traffic lights" in terms of imparting incredibly valuable messages regarding risk to investment as well as business decision makers. In the current environment, the "traffic lights" are out, yet the roads remain jammed with economic travelers. These investment and business decision making "travelers" are not only desirous of achieving acceptable levels of rate of return on capital, but even more desirous of avoiding economic collisions resulting in capital losses.

A few years ago we focused a good portion of portfolios on total rate of return investing as one of what we believed to be a key number of attractive investment themes. This served a bit of a dual purpose as many traditional income oriented sectors such as the telecoms and utilities were low beta in character. This allowed portions of portfolios to achieve acceptable income flows, enhanced the potential for overall portfolio total rate of return, and allowed a lowering of overall portfolio risk via the meaningful inclusion of low beta assets. To make a long story short, the longstanding policy of Fed interest rate suppression forced many a conservative investor to do exactly the same.

The reason we've dragged you through this preliminary commentary is to strongly suggest we all need to heighten our focus upon investment risk, and most importantly investment discipline, in what is an increasingly undisciplined world. As a result of Fed interest rate suppression specifically forcing investors into income oriented equities, valuation risks have grown, and in some cases significantly. Let's look at a few specific examples.

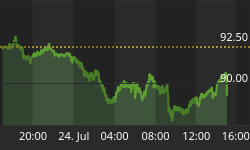

We recently eliminated Verizon from portfolios. WeI may be early for all I know, but we believe the easy money has been made. The stock is up approximately 50% over the last few years, and if purchased a few years back, the yield was 7%. Today the yield on VZ is in the mid 4% range. Relative to near zero yields on short term Treasuries or CD's, 4.5% still looks pretty darn good, but here's a simple question. What is more important now, protecting the 50% price increase, or the 4.5% yield? Sarcasm aside, you know the answer. Eleven years of current dividends are "in the bank" if you've held VZ over the last few years.

You already know that perhaps the most simplistic valuation metric known is the P/E ratio (price to earnings). Here's a quick look at VZ's average annual P/E multiple. Do we really need to comment? Of course not.

Look, this is not a condemnation of Verizon, but more a conceptual example of the increasing need to stay disciplined in an increasingly undisciplined world of central bank and sovereign entity behavior. VZ is a fine company with hopefully a bright long term future. Certainly the assumed Softbank investment in VZ and ATT competitor Sprint means more capital is coming to this industry, and we believe increased competitive pricing pressures. We'll see how it all works out.

What we're really suggesting is that as investors, we now need to focus a bit more intently on what we are paying for forward cash flow streams as the interest rate suppression actions of the Fed have been distorting financial markets for a good while now. We need to remember to focus on valuation metric absolutes and investment risk first, return second, in the environment of the moment. We simply need to drive more defensively when the Fed has turned out the traffic lights.

Like VZ, SO has been a multi-year portfolio holding. We've eliminated a third and look to further reduce (with a downside line in the sand already in place). Again, a fine company, but one where investors will now pay the highest multiple in decades to own forward streams of cash flow after a like 50% price increase over two years. Yes, the electric utilities are wonderful in that profits are almost guaranteed via the granting of allowable rate of return by State PUC's. An industry also benefiting nicely from the collapse in natural gas prices. But an industry that grows revenues, cash flow and profits very slowly.

Once again, we almost hate to single out individual companies as both mentioned above are managed well and are solid financially. What is important regardless of our specific examples is the concept. And that very simple concept is the current need to remain increasingly disciplined as investors despite the increasingly undisciplined actions of global central bankers and the global political community.

Most of you are too young to remember this, but maybe three decades back, Ray DeVoe once commented that "more money has been lost in this country reaching for yield than at the end of a gun." We've never forgotten that truism and have always tried to incorporate it into decision making. It's at times like this that we need guys like Ray the most. Examples litter financial market history. Charles Keating and Lincoln Savings and Loan. The LBO craze of the late 1980's and early 1990's. Auction rate securities in the early part of the last decade. And of course subprime mortgage backed securities five short years ago. Now is the time to remember investment discipline is the key to longer term investment survival, especially when the most important traffic lights in the economy and financial market are out.