For the week ending January 25, 2013, the SPX was up 1.1%, the Russell small caps were up 1.4% and the COMP was up 0.5%.

This is the second week that tech has underperformed large caps and the Russell. Tech has also failed to surpass the September 2011 highs. And with AAPL likely going to test the 370 level in the foreseeable future, it is highly unlikely that tech will move much higher. Nasdaq 100 futures (NQ) has already started to test and fail daily model support earlier this week.

The model remains flat equity indices waiting for a test of support to confirm the rally. Much of this rally has been fueled by JPY pairs which continue to profile as exhaustive. The EUR/JPY and USD/JPY have now closed up eleven consecutive weeks on the weekly chart. That is a truly extreme level. COT and model profiles on all time frames (daily, weekly and monthly) indicate a significant reversal in these pairs is highly probable and imminent.

Other asset classes as indicated below are confirming a growing risk aversion.

Asset Class Correlations

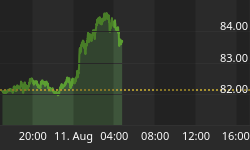

For the week ending January 25, 2013, the EUR was up 1.1%, copper was down 0.5%, 30 year yield was up 10bp and the Aussie Dollar was down 0.8%.

Copper was in a multi-week countertrend rally that was stopped out last week. A test of 3.62-3.63 is probable in the coming sessions. Failure to hold that level will likely trigger short.

The dollar is close to triggering long with a sustained close above 80.05 and confirmed upside momentum over the coming sessions.

The multi-month divergence with equity and the EUR, AUD, copper and 30 year yield remains. As a result equity may show greater relative weakness as part of any future asset class convergence. Using any of these asset classes as a directional indicator may likely produce false signals. Our preference is to use JPY pairs.

There is also a noticeable divergence with the 5 year Treasury break even as shown below which was up 1bp on the week.

Sentiment

Market sentiment remains extremely complacent as viewed through the options market with the VIX at a 6 year low. Implied volatility skew though has been rising averaging 125.87 for the week and closing at 124.71.

Skew is a measure of how implied volatility is distributed. The lower the reading the less skewed the curve, indicating a normalized distribution.

Funds Flow

For the period ending January 17, 2013, $5.1 billion flowed in to domestic equity funds while $10.6 billion flowed in to both municipal and taxable bonds. Though there still remains a large divergence as charted below, this is the second consecutive inflow into domestic equity funds.

For the month of December, domestic equity funds had a net outflow of $22.0 billion while bond funds had a net inflow of $9.8 billion. For 2012, domestic equity funds had a net outflow of $149.3 billion while bonds funds had a net inflow of $295.4 billion.

Bottom Line

We remain waiting for a test of support in determining future equity direction. You never chase a market nor do you chase this move. At a minimum support will be tested. If that holds a new uptrend will form. If that fails, we will likely see resumption of the downtrend. There is no sense getting emotional or speculating where the market will go. Let the market show it's hand. It always does.

JPY cross pairs need to be monitored closely for any signs of an unwind. They remain highly stretched at current levels with COT data confirming an imminent reversal. This will pressure other risk assets ahead of the general equity markets.

About The Big Picture: All technical levels and trends are based upon Rethink Market Advisor models, which are price and momentum based. They do not use trend lines nor other traditional momentum studies. To learn more about how the models work, please click here or visit http://rethink-markets.com/model-profile