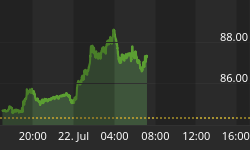

With gold dropping nearly 3% on February 20, we at Casey Research had to look closely at the FOMC minutes, which were partially responsible for that movement. Since there are quite a few highlights, I have split this analysis into three sections: the confusion over the minutes in the market; the ambiguous language hinting at deep problems; and a few quotes to make your blood boil.

The Confusion

A Bloomberg headline from Wednesday, February 20's news reads Fed Signals Possible Slowing of QE Amid Debate over Risks. This headline is characteristic of most of the reporting on the FOMC minutes. Supposedly the Fed signaled a desire to end the quantitative easing earlier. There was actually no such signal.

The committee did, however, discuss possible reasons why they might want to end QE4 earlier. Here are some excerpts from the meeting:

"However, a few participants expressed concerns that the current highly accommodative stance of monetary policy posed upside risks to inflation in the medium or longer term."

"In this regard, several participants stressed the economic and social costs of high unemployment, as well as the potential for negative effects on the economy's longer-term path of a prolonged period of underutilization of resources. However, many participants also expressed some concerns about potential costs and risks arising from further asset purchases. Several participants discussed the possible complications that additional purchases could cause for the eventual withdrawal of policy accommodation, a few mentioned the prospect of inflationary risks, and some noted that further asset purchases could foster market behavior that could undermine financial stability."

Wow, that sounds pretty serious. It's like the Fed has turned a new leaf. Isn't this a clear signal to the market that the easing will end earlier? In a word, no. Here's the most important excerpt, which came toward the end and which many people may have breezed over or missed:

"One member dissented from the Committee's policy decision, expressing concern that the continued high level of monetary accommodation increased the risks of future economic and financial imbalances and, over time, could cause an increase in long-term inflation expectations."

This quote puts the rest of the comments into perspective. There was a discussion of possible risks, but at the end of day, that's all it was, a simple discussion. Although several members expressed concerns in the discussion, when it came down to voting on the actual policy, only a single member dissented.

This reminds me of our internal meetings at Casey Research. Every two weeks, the whole team - including some guest participants - gets on a conference call to discuss the economy and especially gold prices. During the meeting, some participants will voice concerns about the possibility of weaker gold prices. However, at the end of the meeting, all of us are still long gold. A discussion about a change of direction is not the same thing as an actual planned change of direction. It's healthy to have a devil's advocate in any discussion, regardless of the final decision.

Now, the fact that the Fed is discussing these problems is certainly significant; after all, they could just ignore the issues. The sheer fact that there was a discussion means there's a possibility that at some point the concerns could become more serious and then turn into action. But that action hasn't taken place yet, nor is the FOMC planning it. So while what happened in the meeting may warrant a temporary weakening in gold prices, it certainly shouldn't have resulted in Wednesday's major drop.

The Mystery

A few parts of the meeting were quite intriguing, but the purposely murky wording makes it difficult to completely nail down their meaning. It seems that the FOMC has deeper concerns than those discussed above. Here's the first of these mysterious paragraphs from the minutes:

"In general, after having been depressed for some time, investor appetite for risk had increased. A few participants commented that the Committee's accommodative policies were intended in part to promote a more balanced approach to risk-taking, but several others expressed concern about the potential for excessive risk-taking and adverse consequences for financial stability. Some participants mentioned the potential for a sharp increase in longer-term interest rates to adversely affect financial stability and indicated their interest in further work on this topic."

So what does "excessive risk-taking and adverse consequences for financial stability" mean? The next sentence on long-term interest rates offers a clue. Participants warn of a "potential for a sharp increase in longer-term rates." Sure, a sharp upward turn in rates would hurt just about everything, including the stock market, but the sectors that will get hurt the most are real estate and bonds.

Let's see if we can find out which one they're talking about. I wouldn't exactly describe the current real estate market as an area of excessive risk-taking. Most people still won't touch real estate with a ten-foot pole, and though real estate has heated up a bit, I wouldn't call the recent moves in the market excessive. Bonds, however, are in a bubble - and the yields of risky junk bonds have been pushed down a great deal by investors piling into them in search for higher yield, regardless of the underlying risk. Now this is just my interpretation, but it seems to me the Fed is saying that the bond bubble is a serious problem.

Here's our next mystery paragraph:

"A few also raised concerns about the potential effects of further asset purchases on the functioning of particular financial markets, although a couple of other participants noted that there had been little evidence to date of such effects. In light of this discussion, the staff was asked for additional analysis ahead of future meetings to support the Committee's ongoing assessment of the asset purchase program."

You see what I mean by murky wording. "Particular financial markets" and "little evidence to date of such effects" don't say much. What evidence and what effects, and in which financial market? Apparently, the Fed members find this issue worrisome enough to warrant further analysis; unfortunately, they're not being very forthcoming about it. What it does show, though, is that there are two conversations taking place about risk: one for the public and another one behind closed doors.

The Anger

As promised, here are a few quotes that might make your blood boil. If you read through the minutes quickly, they seem benign, but if you stop to think about them, they're infuriating. Here's the first:

"In 2014 and 2015, real GDP was projected to accelerate gradually, supported by an eventual lessening of fiscal policy restraint, increases in consumer and business sentiment, further improvements in credit availability and financial conditions, and accommodative monetary policy."

Umm. wait; what "eventual lessening of fiscal policy restraint"? Essentially, the Fed is saying that as economic conditions improve, the American voter will stop complaining, and the government can finally get back to spending wheelbarrows of money. It's scary to think that these additional government spending plans are already reflected in the Fed's GDP projections, but apparently this isn't the only forward-looking policy prediction from the Fed:

"For example, a couple of participants noted evidence suggesting that a shift in the relationship between the unemployment rate and the level of job vacancies in recent years was unlikely to persist as the economy recovered and unemployment benefits returned to customary levels."

It seems that the Democrats have been very touchy about reducing those unemployment benefits, and the Fed seems to have a lot of faith in the government doing the right thing. But it's going to be tough for any party to curb those benefits when unemployment rates are even as low as 6%. Let's see what else the Fed's crystal ball forecasts for us:

"The staff continued to project that inflation would be subdued through 2015. That forecast is based on the expectation that crude oil prices will trend down slowly from their current levels, the boost to retail food prices from last summer's drought will be temporary and relatively small, longer-run inflation expectations will remain stable, and significant resource slack will persist over the forecast period."

OK, I buy the argument about the temporary effect from the summer drought, but the assumption of downward-trending oil prices seems a bit unrealistic. And if we're seeing growth in the economy as the Fed expects, then shouldn't the Fed forecast rising oil prices to match growing demand? Why even tinker with the numbers in this way? The Federal Reserve doesn't have a comparative advantage at projecting oil prices.

Here's the last bit worth noting:

"In addition, the Committee's highly accommodative policy was seen as helping keep inflation over the medium term closer to its longer-run goal of 2 percent than would otherwise have been the case."

If you read that quickly, you might think to yourself, "Well, that sounds good. I guess they managed to keep inflation closer to the 2% target." But think about what they're actually saying. Their accommodative policy is also known as "printing money." That's a process of pushing inflation up, not down. So, what they're saying is, "Man, we did a good job of pushing inflation up to 2%! Otherwise, it would have been lower." Ain't that just great?

It's imperative to protect yourself from the Fed's rampant money-printing, as sooner or later it can't help but cause serious inflation. One of the best ways to do that is internationalize.