The selloff in gold that captured the world's attention in mid-April has revealed some truths about how the market trades and the sentiments of many of the investors who have piled into the trade over the past few years. While the correction does highlight a higher degree of uncertainty than many of the most ardent gold advocates had anticipated, it does not represent the historic "end of an era" reversal that the many in the media have so gleefully suggested. In many ways, the market has shown a resiliency that its detractors do not understand.

Traditionally, investors buy gold for three primary reasons: as a hedge against inflation, as insurance against economic catastrophe and as a medium for speculation. Lately the mainstream investment establishment, and the media outlets that slavishly follow their pronouncements, have attempted to make each group question their resolve. During the attack many blows were landed, but fortunately no knock outs were scored.

In most developed countries inflation has been reported to be far below the predictions made by the monetary hawks. Keynesian worries about deflation have even shouted down the risk of inflation as the most imminent monetary threat. Simultaneously, surges in stock markets in the United States and Japan, and improvements in the U.S. housing market, have boosted consumer confidence and have convinced many that the global economy is in the midst of a strong and stable recovery. Lastly, after more than a decade of largely steady gains, a cessation of gold's upward momentum created a variety of technical patterns that convinced short term speculators that a gold sell off was imminent. These predictions became self-fulfilling when the largest Wall Street firms lowered their mid-term price targets. Media outlets descended upon these developments like a pack of hungry wolves, resulting in the most serious sell off in gold in nearly five years.

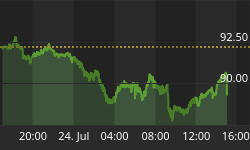

Between April 1 and April 15, gold declined more than 18%. Many observers had pointed to the generational collapse that occurred to gold in 1980 and ignored similar gold sell offs in 2006 and 2008 that led to fairly rapid recoveries. However, the metal stubbornly refused to follow the script that was being written. The fall stopped abruptly and gold has recovered almost 10% since mid-April. So are we seeing a "dead cat bounce" of a dying asset class, or will gold resume its ascent?

Today, we are witnessing an epic, international struggle between the natural forces of a deflationary recession pitted against the inflationary forces unleashed by the monetary expansionism by three of the world's most important central banks: the Fed, the Bank of Japan, and the ECB. This struggle is reflected in market volatility and uncertainty, which I believe will persist for some time.

Global Quantitative Easing (QE) initiatives have now injected a staggering $10 trillion of new fiat currency into the global economy. By definition, these moves are inflationary but the economies of the debtor nations are so unpromising that the bulk of QE cash has been hoarded as bank deposits, thereby blunting the inflationary impact. The camouflage that low official inflation statistics currently provide has blinded investors to the likelihood of future inflation.

In March, the gold market received another unforeseen shock. The sovereign crisis in Cyprus raised the prospect that the country would be forced to sell its gold reserves to meet its debt obligations. Although Cyprus has only 14 tons of gold, investors fear that such liquidation sales could herald larger sales by troubled Eurozone nations like Portugal (382 tons), Italy (2,452), Greece (112), Spain (282) and even France (2,435 tons). Taken together, these countries account for some 18 percent of all central bank held gold. This potential overhang encouraged further sales by speculators. However, as Peter Schiff pointed out in an article earlier this month, fears of a central bank sell off fail to consider the potential actions of emerging market central banks.

As rumors of national gold sales subsided, the price of gold recovered somewhat, ending this past week at about $1,460. However, retail buyers demanding physical gold coins kept the price for a one-ounce coin well above $1,500 at week's end. This gave rise to an ominous difference between the 'official' gold price ($1,460) and the 'actual' price of physical gold ($1.501.30-$1,613.75), depending on the dealer.

Central bank QE targets continue to twist and change creating added investor uncertainty. Furthermore, the U.S. Bureau of Economic Analysis (BEA) announced future changes in its method of calculating GDP (see commentary). By including corporate expenditures on R&D, TV, movies and Government 'promises' of future pensions as 'investments', GDP will be boosted synthetically. This will help serve to maintain the illusion of health, thereby keeping the gold market off balance.

Meanwhile, the Fed has 'persuaded' the Central Bank of Japan to enact limitless QE. In July, Mark Carney, reputed to be a Bernanke style monetary expander, takes the helm at the Bank of England. This adds to the political pressure being brought on Germany to drop or at least dilute its austerity medicine in favor of possibly even more massive QE by the ECB. Finally, rumor indicates that Janet Yellen, a super Keynesian, will succeed Ben Bernanke as Chairman of the Fed.

It appears that the major central banks will follow the Fed in creating limitless synthetic fiat currency. Like inflating a balloon, at some stage, the skin is stretched to the point where a rupture is inevitable. The trust placed by the world's savers is analogous to the skin of this particular balloon. Should it burst, both the price increases and economic uncertainty long heralded by gold investors may arrive with stunning force. Should that happen, the momentum traders will pile back into the market and gold may reach new heights.

If confidence in the current monetary system persists intact, and is combined with continued evidence of economic weakness (and seemingly antithetical stock market momentum), it is possible that the price of gold will suffer another leg down. Under the right circumstances it could fall below $1,300. While the tug of war between inflation and confidence in fiat money may persist for some time, the weight of history will eventually come down against paper. It always has, and it always will.

Subscribe to Euro Pacific's Weekly Digest: Receive all commentaries by Peter Schiff, John Browne, and other Euro Pacific commentators delivered to your inbox every Monday!

Order a copy of Peter Schiff's new book, The Real Crash: America's Coming Bankruptcy - How to Save Yourself and Your Country, and save yourself 35%!

John Browne is a Senior Economic Consultant to Euro Pacific Capital. Opinions expressed are those of the writer, and may or may not reflect those held by Euro Pacific Capital, or its CEO, Peter Schiff.