The next formal policy statement from the Federal Reserve could prove to be unfriendly to the current stock rally. Based on history, it is reasonable to state Jon Hilsenrath of the Wall Street Journal (WSJ) is plugged into the Fed. From a Hilsenrath WSJ story dated June 7:

Federal Reserve officials are likely to signal at their June policy meeting that they're on track to begin pulling back their $85-billion-a-month bond-buying program later this year, as long as the economy doesn't disappoint.

Stocks Held At Logical Level

Last week's sell-off in stocks was held in check near the intersection of the April closing highs and the trendline from the November 2012 lows (see chart below).

Intermediate-Term Outlook Remains Bullish

This week's technical analysis and stock market forecast video (below) covers bullish trends from a daily, weekly, and monthly perspective.

Fed May Acknowledge Economic Improvement

While it is highly unlikely the Fed will announce a reduction in bond purchases next week, any new language that speaks to an improving economic outlook could be interpreted as a "tapering is coming" signal. From the June 7 Wall Street Journal story:

A good-but-not-great jobs report last Friday ensured officials wouldn't want to act right away and would instead want to see more data before taking a delicate step toward winding down the program. But they could point at their next meeting to improvement they're seeing in the economy, a prerequisite to reducing the so-called quantitative-easing program.

No Higher High Yet

With a Fed statement due June 19, the S&P 500 still has some work to do. As of Monday's close, the index was still noticeably below the May high.

Retracement Levels Not Yet Cleared

The bounce in stocks that began last Thursday has yet to clear a Fibonacci hurdle commonly watched by traders. If the S&P 500 can close above 1,646 and change, it would increase the odds of a push toward a higher high above 1,669.

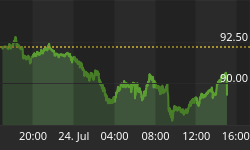

Bond Market Already Moving

Any reduction in the Fed's bond purchase program will have a similar impact to a more traditional interest rate increase, which tends to put a drag on bond prices. After a very difficult month in May, bonds appear to be pricing in a change in Fed policy. Long-term Treasuries (TLT) have not made a new high since July 2012 (see below).

Stocks Beating Bonds

As we noted on May 28, all investment decisions involve opportunity costs. Even with the stock market's recent volatility, equities have continued to outperform bonds. The chart below, as of Monday's close, shows stocks making a new weekly closing high relative to bonds.

Materials Signaling Economic Improvement

All things being equal, materials stocks tend to be in greater demand during periods of economic expansion. The weekly chart of the materials ETF(XLB) shows a recent bullish breakout from previous areas of resistance dating back to June 2011, which supports the case for economic improvement.

Hanging On To Bullish Bias

In the chart below, the red text describes a "bearish look" from a weekly perspective. The green text describes the look of a bullish trend from a weekly perspective. As of Monday's close, the look can be classified as tentatively bullish. Our concerns would increase if the chart below morphs into a downtrend (see October 2012), especially in the aftermath of any Fed-tapering hints next week.

Leadership Sides With Cyclical Trade

Healthy stock market advances tend to be led by more economically-sensitive sectors such as financials, small caps, and technology. From a weekly perspective, financials (XLF) have held up relatively well.

Strength In Small Caps

When investors feel better about future economic outcomes, they are more willing to invest in smaller (read riskier) companies. Small caps (IWM) kicked off the trading week with a gain of 0.61%. For comparison purposes, the S&P 500 posted a slight loss in Monday's session. It is difficult to become overly concerned when small caps are outperforming.

Investment Implications

We will continue to favor stocks (SPY) over bonds (AGG) as long as the leadership and trends covered above remain in place. It is prudent to pay close attention with a Fed-tapering signal possibly coming next week. Higher highs in the major indexes would elevate some of our concerns related to being long stocks. A higher high would be in place if the S&P 500 can close above 1,670. We are open to shifting to a bearish or defensive bias if the charts begin to point in that direction, especially in the wake of any bear-friendly statements from the Federal Reserve on June 19.